With inflation at multi-decade highs, the annual increase to Social Security’s has been a hot topic lately. With all the coverage this is receiving in the news, I’ve constantly been asked the same questions.

The most common questions I receive are:

- How is the annual increase in Social Security calculated?

- What happens if they switch to an alternate method (CPI-E)

- How is the annual increase applied to a Social Security benefit?

- What age does the annual increase in Social Security start applying?

- Do you have to be receiving benefits to get the annual increase?

Let’s answer each of these questions individually…

1) How is the annual increase in Social Security calculated?

On an annual basis, the Social Security Administration uses a certain measurement of inflation to determine if benefits should be increased or not. The measurement they currently use is the CPI-W, which stands for the Consumer Price Index for Urban Wage Earners and Clerical Workers. This inflation gauge is compiled and published by the Bureau of Labor Statistics.

Although they release the data on a monthly basis, the Social Security Administration (SSA) only makes adjustments to Social Security benefits based on the third quarter data (July, August, and September). The prior year third quarter data is compared to the third quarter index for the current year. If the difference between the two numbers is positive, Social Security benefits increase. If there is no increase in the CPI-W, then there is no cost of living adjustment for the year.

2) What happens if they switch to an alternate calculation method (CPI-E)?

Some say the CPI-W measurement method may not be the best because retirees spend their money very differently than individuals who are not retired. Retirees tend to spend more on healthcare and housing, and less on gasoline, education, and consumer electronics.

As a fix for this, it has been widely suggested that the Social Security Administration should discontinue basing the annual increase to Social Security on the CPI-W and instead start using a measurement known as the CPI-E.

This version of the CPI is meant to track the expenses specifically for Americans who are 62 years of age or older. While both of these indexes measure the same categories of goods and services, they have different weightings to the categories.

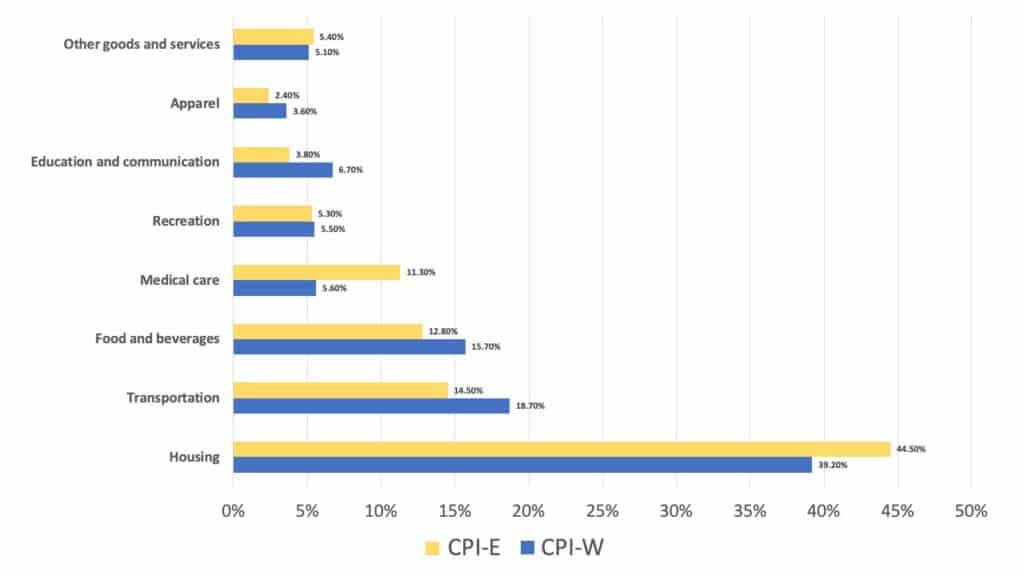

So for example, the CPI-E factors in around 11% of its index to healthcare cost. The CPI-W, however, only counts 5.6% of the overall index as healthcare expenses. Since statistically, seniors spend more of their money on healthcare, an index that assigns a higher weighting should be more accurate to the way they spend money and experience inflation.

There are some other differences in weightings between the CPI-W and the CPI-E that may be significant for determining the annual increase to Social Security benefits. In total, each index measures 8 main categories:

- Housing

- Transportation

- Food and beverages

- Medical care

- Recreation

- Education and communication

- Apparel

- Other goods and services (for the stuff that doesn’t fit anywhere else)

The chart below shows that the two biggest differences are the weightings assigned to housing and medical expenses: The big question here is: What does this mean for the actual increase to Social Security? Would it result in a larger benefit increase for seniors?

The big question here is: What does this mean for the actual increase to Social Security? Would it result in a larger benefit increase for seniors?

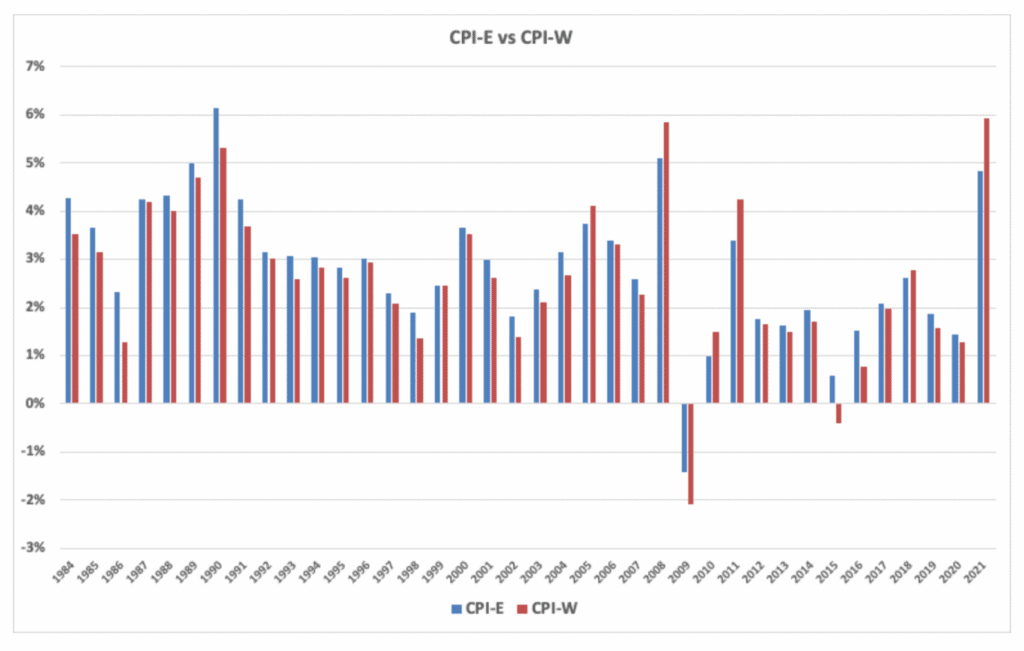

If you average the difference between the two measurements since 1984, the CPI-E has been about 0.2% higher per year. So yes, in most years the CPI-E would yield a higher cost of living adjustment than the CPI-W, but there are some years (like the increase announced in October of 2021) where the CPI-W was higher than the CPI-E.

This illustrates the reluctance of legislators to implement the change. On paper, it sounds good. An index that more accurately represents the expense of retirees should work better. But no politician wants the responsibility of making this switch in a year where the new method yields worse results than the old one.

Ultimately, there is no magic formula that works well enough to keep everyone happy.

3) What age does the annual increase to Social Security start applying?

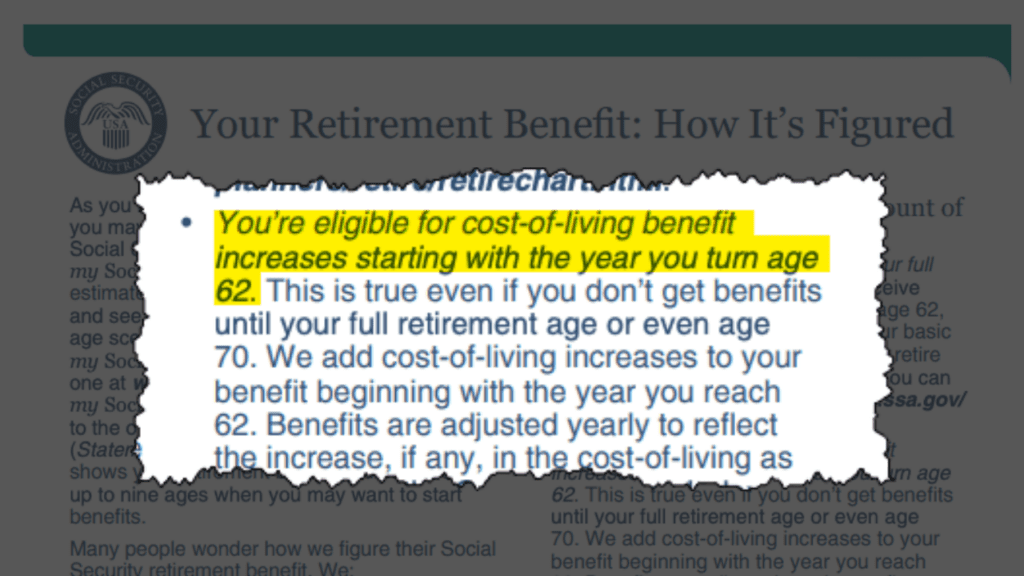

The Social Security publication titled “Your Retirement Benefit: How It’s Figured” succinctly addresses when the annual increases start applying to benefits.

They say: “You’re eligible for cost-of-living benefit increases starting with the year you turn age 62.”

That seems clear, but the annual increases to Social Security are commonly reported in such a way that makes it difficult to understand.

For example, in October of 2021 the SSA announced a 5.9% increase. In most publications and new reports, this was referred to as the “2022” increase. This led many to think that if they turned 62 in 2022, the cost of living would apply to their benefit. That’s not accurate. Technically, the increase announced in October of 2021 was the 2021 increase. It was announced in 2021, and applied to benefits in December of 2021 (payable in January of the following year).

If you look closely, there are multiple places where the SSA referred to this as the 2021 increase while the rest of the world called it the 2022 increase.

Here’s the easiest way to remember this: The first annual increase in Social Security which will become effective for your benefit is the one announced in the same year you turn age 62.

4) Do you have to be receiving benefits to get the annual increase?

Regardless of whether you have filed for benefits or not, the annual increase to Social Security applies to benefits starting at age 62.

The Social Security Administration has a piece that is very clear on this. It says, “You’re eligible for cost-of-living benefit increases starting with the year you become age 62. This is true even if you don’t get benefits until your full retirement age or even age 70. We add cost-of-living increases to your benefit beginning with the year you reach 62.”

Now that’s very clear as to when the annual increase in Social Security applies to retirement benefits, but it doesn’t mention survivor or disability. For that, we have to dig a little deeper into the Social Security website.

Because these rules are often a bit convoluted, we actually have to reference two different rules. First, we find the rule on when the annual increase is applied and according to their program operations manual systems, or POMS, (that’s the handbook for processing claims), they say “Beneficiaries entitled to an AIME PIA or a Transitional Guarantee PIA are entitled to any COLA which occurs in or after the benchmark year.”

Here’s the simplified interpretation of that.

If you become entitled to benefits after 1978, you are entitled to any annual increase to Social Security which occurs in or after your benchmark year.

This raises the obvious question…what is a benchmark year? For that, we turn to another section of this manual which defines the benchmark year for retirement, disability, and survivor benefits.

- For retirement benefits, the benchmark year is the year you turn 62.

- For survivor benefits it’s the earliest of the year you turn 62 or the year of death.

- For disability benefits it’s the earliest of the year you turn 62 or the year you become disabled.

Note: There are some changes that could happen to the benchmark year for disability benefits if you are on receiving disability and then stop for at least a 12 month period before filing for retirement benefits. For the full rules on this, read section B of the POMS manual page on this.

5) How is the annual increase in Social Security applied to a benefit?

Although the mathematical application of the annual increase in Social Security seems fairly simple, the method used could cause slight variations from what you may expect.

You can’t just look at your benefits estimate and assume all of the estimated amounts for the various ages will increase by the announced increase percentage. Instead, the annual increase is applied to your primary insurance amount (PIA) and then adjusted based on increases for filing later or reductions for filing early. (The PIA is generally the same as what you’d receive if you filed for retirement benefits at your full retirement age.)

The exact steps to calculate and apply the changes to your benefit are as follows:

- Adjust PIA for the annual increase percentage,

- Apply the adjustments for filing before or after full retirement age

- Round results to the next lower dime.

- Subtract any offsets (such as Medicare Part B premiums)

- Round the remainder down to the next lower dollar (the result of this step is your final benefit)

By following these steps it’ll help you understand the math behind figuring out why your annual increase in Social Security was slightly different than you expected if you just take a percentage and apply it to the benefit.

Don’t miss my article How the Social Security COLA Affects Spousal Benefits

Your Next Steps

As a next step in your learning about the annual increase in Social Security, you should consider joining the nearly 400,000 subscribers on my YouTube channel! This is where I break down the complex rules and help you figure out how to use them to your advantage.

And don’t leave without getting your FREE copy of my Social Security Cheat Sheet. The most important stuff from the 100,000 page website is all condensed down to just ONE PAGE! Get your FREE copy here.

[…] If you want to learn more about the annual increase to benefits, be sure to check out my article “5 Most Common Questions About The Annual Increase in Social Security (COLA).” […]