If you’re receiving Social Security benefits or Medicare and have recently moved, your Social Security change of address needs to be high on your priority list.

“Even if you receive your benefits by direct deposit, Social Security must have your correct address so we can send letters and other important information to you. We’ll stop your benefits if we can’t contact you.”

Ouch! You don’t want that to happen.

Thankfully, it’s pretty easy and painless to get your address changed. You just have to choose which of these three approaches will work best for you.

It’s important for you to have a clear understanding of the process used to calculate your Social Security benefits. If you understand this calculation, you may be able to spot mistakes and fix them before it’s too late.

Like anything with Social Security, the rules can seem complex at first. But once you get under the surface, they are actually pretty easy to understand. To help you, I distilled the several pages of calculation rules down into four easy-to-understand steps.

Why Do I Need To Know How To Calculate My Social Security Benefits?

So you may be thinking, “Why do I need to know how to calculate my own Social Security benefits? After all, the SSA will give me an estimate at any time.”

That’s true! You can go to your My SSA account online and see an up-to-date copy of your benefits estimate. So why would you need to know how to do this calculation on your own?

It’s important for a few reasons.

First, it never hurts to understand the mechanics behind an income stream that’ll probably be a large part of your overall retirement income.

This means that these estimates are less accurate for younger workers but more reliable for workers who are close to retirement.

So, understanding how to do this calculation is especially important if you plan to retire early or later than “normal” or if you have a significant earnings change in the last few years of working.

To do this calculation, there are only four steps.

Adjust all earnings for inflation

Calculate your Average Indexed Monthly Earnings (AIME)

Apply your AIME to the benefit formula to determine primary insurance amount (PIA)

Adjust PIA for filing age

Social Security Calculation Step 1: Adjust all earnings for inflation

So let’s jump in with calculating your AIME. To do this, you’ll need to get use a notepad or a tool like Excel/Google Sheets.

You’re going to need six individual columns with plenty of room underneath for your information. Set up your columns with the following headings: Year, Age, Actual Earnings, Indexing Factor, Indexed Earnings, Highest 35 Years.

The first two headings are the year and your age. Go all the way back to the first year you had earnings that were taxed for Social Security. You can find a complete record of this by going to your online SSA account and click the link that says “view earnings record.” If you don’t have an online account, it’s very easy to set one up.

This may seem a little redundant to put the year and your age, but it’ll make another step a little easier.

Now you just need to copy down the information from the SS earnings history. You’ll want to use the part that says “your taxed Social Security earnings.” Don’t skip a year, even if there were no earnings. Just put a zero in.

Once you have all of your historical earnings recorded, it’s time to adjust them for inflation. The SSA uses an indexing factor to make sure your future benefit has kept up with inflation, but still based on your earnings.

Important note here…only your earnings through age 59 are indexed. All earnings at age 60 and beyond are used in the calculation at face value with no inflation adjustment applied.

Also…When you’re getting your indexing factors, you have to be careful to use the factors specific to your age.

The easy way to get these is to visit the SSA web page on indexing factors. At the bottom of that webpage it says, “Enter the year of eligibility for which you want indexing factors.” This should be the calendar year you turn 62. It’s really important to use this year to make sure you get the correct indexing factors.

Now that you have your indexing factors, just copy them on to the sheet. Be sure to keep your years matched up.

Once your indexing factors are written down, you simply need to multiply your actual earnings by your indexing factor. This will give you your indexed earnings.

Social Security Calculation Step 2: AIME Calculation

Now, all you have to do is extract the highest 35 years of indexed earnings.

If you’re still working and don’t have 35 years, you’ll need to estimate what your future earnings will be and apply the indexing factors just as you would for actual historical earnings. This is where you can start to play around with the numbers to see the various impacts of retiring early, or working later or maybe having variable earnings close to retirement.

Once you have your highest 35 years in the last column, you just need to sum them up and divide by 420. You divide by 420 because that’s the number of months in 35 years and we need to get your average earnings expressed as a monthly number.

Once you do this, congratulations…you have your AIME and have finished the first (and hardest) step of the calculation. It’s downhill from here.

Social Security Calculation Step 3: Primary Insurance Amount (PIA) Calculation

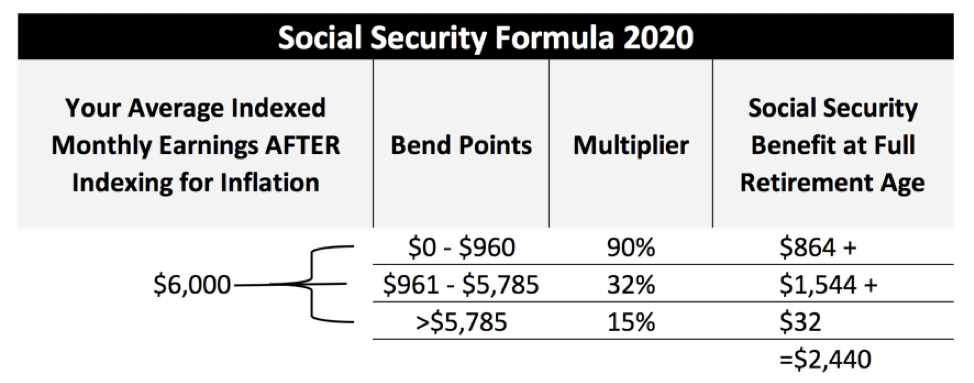

Now you’re ready to determine the heart of your benefit; your primary insurance amount (PIA). The PIA is simply the result of your benefit calculation and is generally your full retirement age benefit amount.

This is calculation is accomplished by using the “bend point” formula that’s in effect for the year you attain age 62. If you aren’t 62 yet, you’ll need to forecast what the bend point formula amounts will be in the year you turn 62. These change annually based on the change in annual wages and generally increase at 3-4%.

There are two numbers that make up this formula which are separated into three separate bands: The amount up to the first number, the amount between the first and second number, and the amount above the second number.

For earnings that fall within the first band, you multiply by 90%. That is the first part of your benefit.

For earnings that fall within the second band, you multiply by 32%. That is the second part of your benefit.

For earnings that are greater than the maximum of the second band, you multiply by 15%. This is the third part of your benefit.

The sum of these three bands is your benefit amount at full retirement age: your PIA, or Full Retirement Age benefit amount.

In the example image below we illustrate an individual with an AIME of $6,000 being applied to the bend point formula.

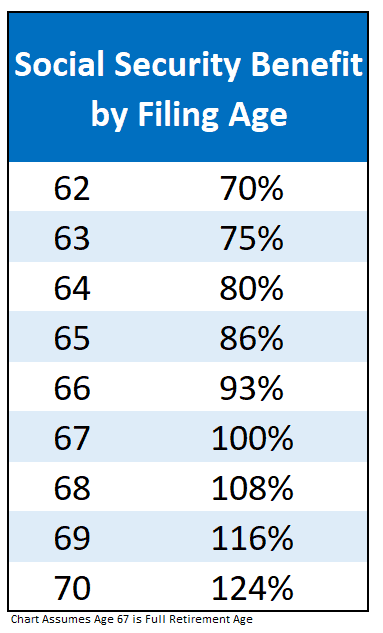

Now that you’ve calculated your average index monthly earnings and applied them to the PIA formula, you simply need to figure out how your filing age will impact your benefit amount.

Social Security Calculation Step 4: Adjust for Filing Age

The easy way to look at it is to think about it in annual numbers.

Your benefit will be lower if you file at 62 and higher if you file at 70.

If you file after your full retirement age, your benefit will increase by 8% per year. If you file in the 3 year window immediately prior to your full retirement age your benefit will decrease by 6.66% per year of early filing. For anything more than 3 years before your full retirement age, your benefit will decrease by an additional 5%.

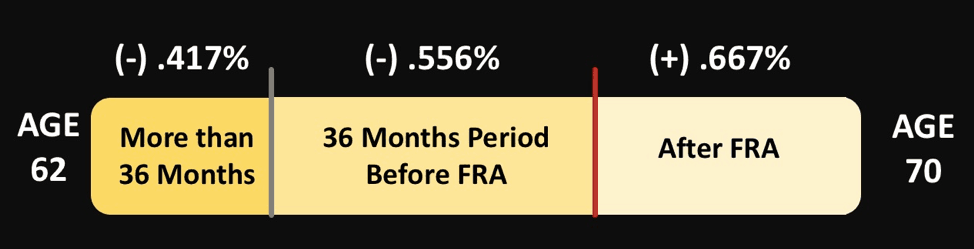

A lot of people don’t want to retire on their birthday so it’s important to break this down by a monthly amount.

Monthly Increase/Decrease Percentages

After your FRA, your benefit will be increased by .667% per month you delay.

For the 36 month period before full retirement age your benefit is reduced by .556% and for more than 36 months it is reduced by .417% per month.

And that is it! Once you’ve gotten through this step you’ve successfully calculated your Social Security benefit.

It’s your retirement!

Before you leave I’d recommend staying connected with my content so you won’t miss anything. In many cases, I’ll publish my newest stuff on YouTube (with more than 400,000 subscribers!) and then have a discussion in my Facebook group.

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

How confident are you that your Social Security earnings record is accurate?

Unless you’ve checked it recently, you shouldn’t be too sure.

Mistakes in an individual’s Social Security earnings record are actually much more common than most people think. In tax year 2012 alone, the Social Security Administration reported $71 billion in wages that could not be matched to an individuals earnings record! The good news is that the Social Security Administration has a system for sorting out some of these mistakes and assigning the earnings to the correct record. But nearly half of the mismatches are never corrected. That means that in 2012 there were approximately $35 billion in wages that was never credited to an individual’s Social Security history.

Why A Social Security Earnings Record Mistake Matters

A mistake in your earnings history can make a big difference in how your Social Security benefits are calculated. How? It all goes back to the benefit’s formula. The Social Security Administration uses your highest 35 years of earnings as a cornerstone of the benefit calculation. If any of these 35 years are incorrect or missing altogether, the average is skewed. One year of missing earnings can make a difference of $100 per month (or more!) in your benefit amount. Over your lifetime, that could be nearly $30,000 in missed benefits from one year of missing earnings.

You need to check your Social Security earnings record today. Thankfully, it’s pretty easy to do.

Here’s how to accomplish this in five easy steps.

Step 1

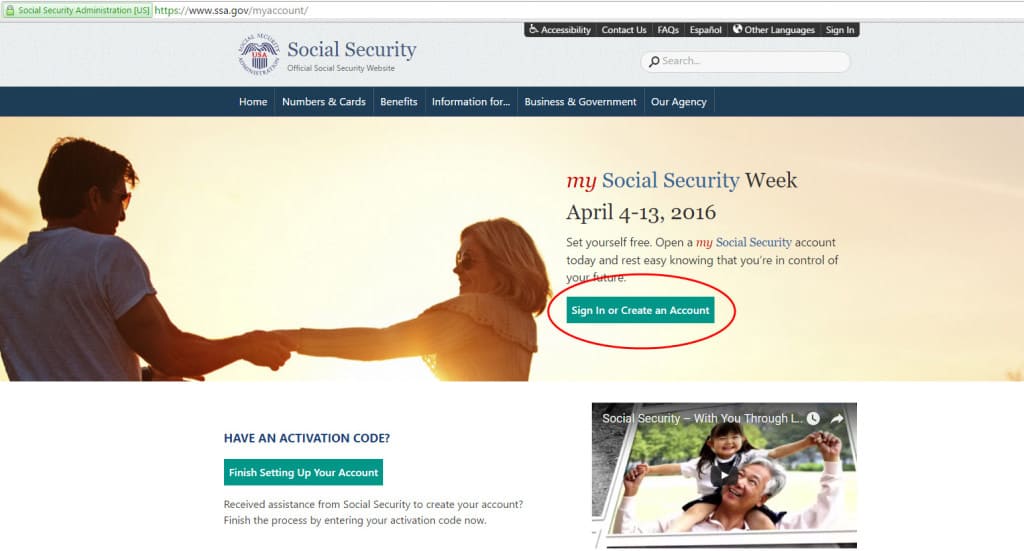

Visit www.ssa.gov/myaccount to get started. If you click the link, it will open Social Security’s website in a separate page so you can keep using this guide.

Once the page loads, simple click on the button labeled “Sign In or Create an Account.”

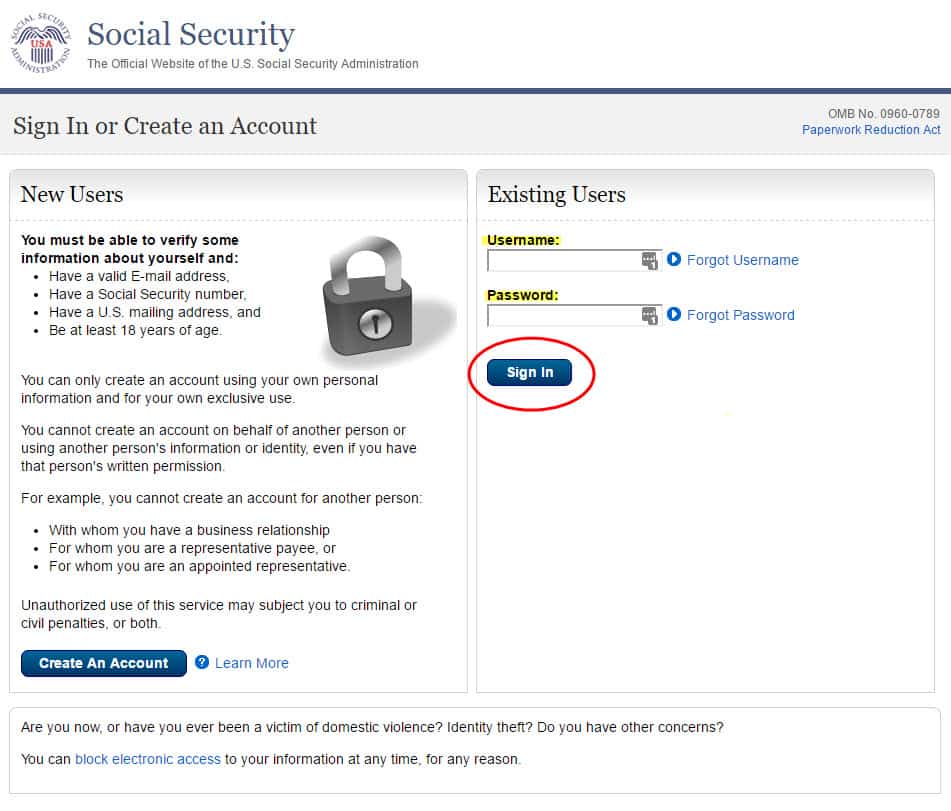

Step #2

Type your username and password and click the button labeled “Sign In.”

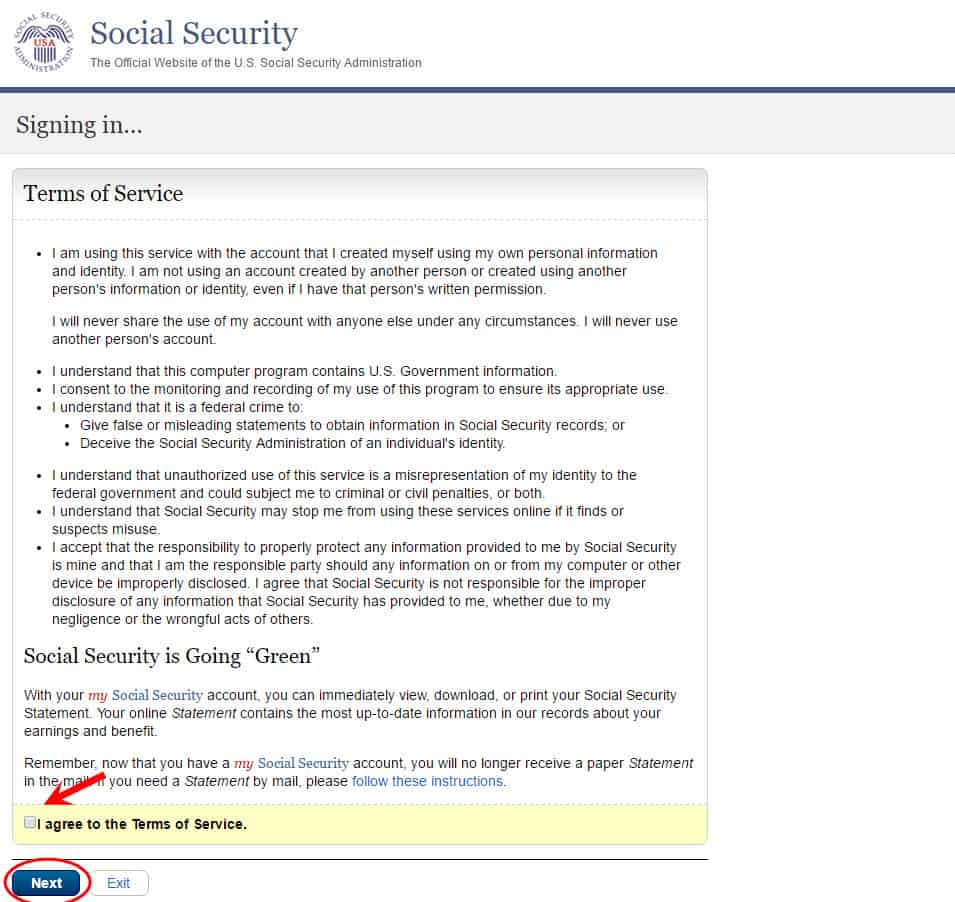

Step #3

In the third step, you need to read and agree to the my Social Security Terms of Service. Be sure to carefully read this page before clicking in the “I agree” box and then clicking “Next.”

Although you need to understand this information for yourself, here’s a summary of what you are agreeing to.

-You will never share your information with anyone or use anyone’s account

-Once you open an account, you will no longer receive a paper statement in the mail. Instead, you’ll receive an annual email reminding you to log in and check your information.

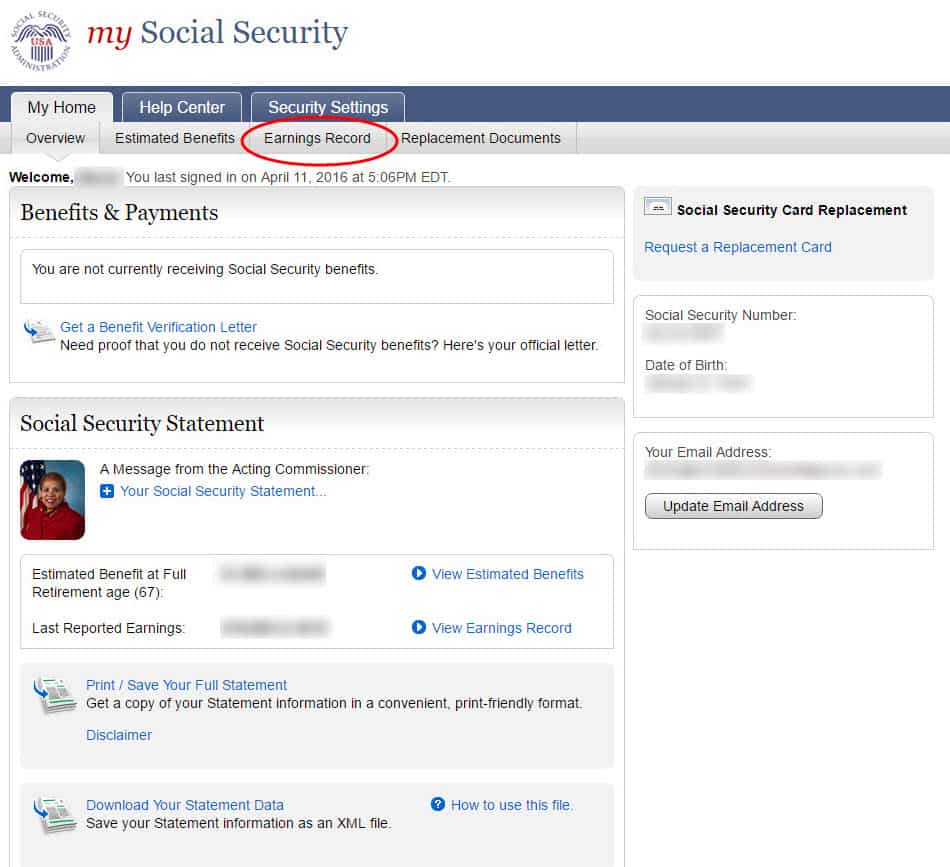

Step #4

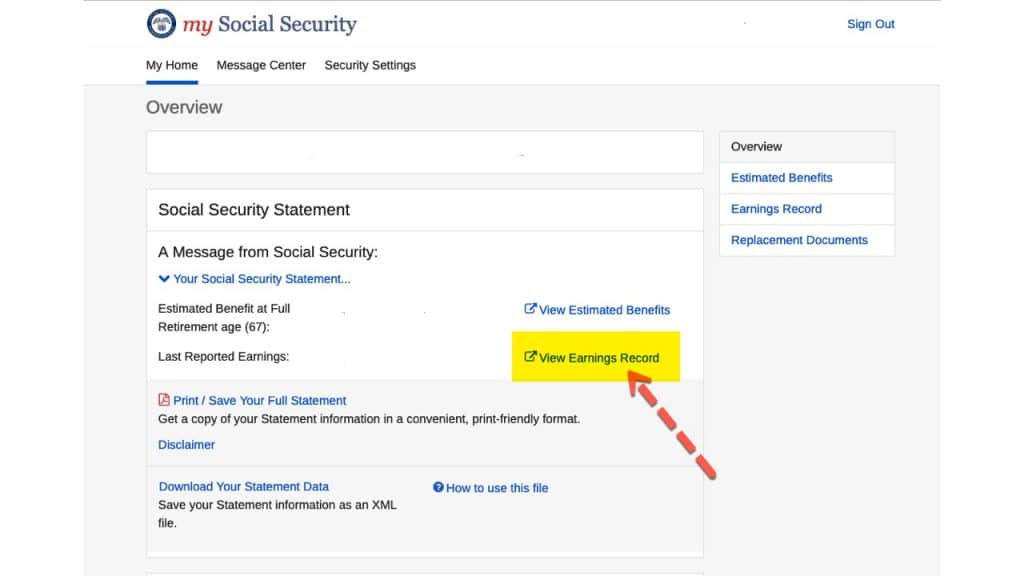

Now that you are on the home page, you just need to click on “Earnings Record” tab at the top.

Step #5

On your screen you should see your earnings record. Check it carefully. If there is a mistake, the burden is yours to prove it. You’ll need to locate documents that prove the error such as tax forms, W-2 forms or pay stubs. If you can’t find these, Social Security says to write down the name and address of your employer, the dates you worked there, how much you earned and the name and Social Security number you were using while you were employed, and the agency will use this information to investigate the problem.

For more information from the Social Security Administration on the procedure, you can visit the section of their POMS manual that discusses this.

Step #5 1/2

Dont forget to sign out! This system has too much valuable information to leave it open.

If you have questions about any of this, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

Your Social Security benefits statement has some really important information in it. But where do you find it?

Several years ago the Social Security Administration stopped mailing the annual benefits statement to save cost. Then they started back…but not for everyone. Now, you’ll only receive a statement 3 months before you turn age 25, 30, 35, 40, 45, 50, 55, and 60. After age 60, you should receive a statement every year.

I’m glad they started mailing them again, but for those under age 60 receiving a new Social Security statement every five years in not nearly often enough. Your estimated benefits are most likely changing on an annual basis when your yearly earnings are recorded. If you keep your retirement plan updated annually (and you should), you’ll need these numbers to change your calculations.

So forget waiting on the postal service to deliver this important document. Just use this step-by-step guide and you’ll be looking at your benefits statement in less than two minutes!

Whatever your age, setting up a my Social Security account is a great idea. Especially if you hate the long lines at the Social Security office! It’s really easy too. From the comfort of your sofa you can go the Social Security sign in page and conduct business that would otherwise require a trip to the SSA office.

Also, the information available in your online Social Security account is critical for sound retirement planning. So if you haven’t already claimed your account, you should today!

Here are a few things you’ll be able to do once you sign up.

If you have already filed for Social Security

You can:

-Change your direct deposit

-Get a replacement SSA-1099 or SSA 1042S for tax purposes

-Instantly print a letter wtih proof of your Social Security benefits

-Change your address

-Request a replacement Medicare card (if over 65)

-Check your benefit and payment history

If you have not already filed for Social Security

You can:

-Verify your earnings history and then keep track of your yearly earnings

-Get an estimate of your future benefits

-Apply for Social Security benefits

If all of those reasons aren’t enough to convince you to set up your online account today, consider this: For every day that goes by without YOU setting up your online account, your chances increase that someone else will! If for no other reason, do it to keep yourself protected!

How to Set Up Your Online Social Security Account

Setting up your my SSA account is really simple. In fact, I can show you how in 8 super-easy steps.