Jo’s husband died when he was 44. Jo was only 43, and up until that point, they ran a successful plumbing supply business together. Jo and her husband earned a high income, and his passing left her with the burden of running a demanding business alone.

She didn’t spend a lot of time thinking about her future Social Security benefits at that point of her life. But things are different now.

Jo is about to turn 60. She’s been told that she can qualify for Social Security survivors benefits, and has also heard that the Social Security Administration has a history of miscalculating these benefits — so Jo wants to make sure she understands the math herself.

You Can’t Use the Normal Calculations to Understand Social Security Survivors Benefits

Jo watched my video on how to calculate Social Security benefits, but she walked away feeling thoroughly confused. That’s not how I want any of my viewers to leave my videos, but on this one… I can understand why.

(This is also why I recorded a new video called “What If You Die Early?” to make sure other viewers have more resources!)

What was the problem? The video itself wasn’t confusing. The issue lies in the fact that most people don’t know that Social Security survivor benefits are not always calculated the same way that retirement benefits are calculated.

There are alternate calculations that are used if you die early.

The Alternate Calculations to Understand If a Spouse Dies Early

Whether you’re trying to figure out what your benefit will be because you’ve lost a spouse or maybe you’re building a retirement plan and running some “what-if” scenarios for your own partner, understanding these alternate calculations is really important.

Unfortunately, a lot of people, including financial planners, get this wrong because they are relying on the software they use to tell them how to plan for risks that occur before retirement.

But you can’t do that with Social Security.

These software programs don’t always know who is eligible for a benefit, under what conditions are they eligible and most importantly, how that specific benefit is calculated.

I want to break this article down into three sections. Here’s what we’ll cover:

- How to determine if the person who died worked for enough years for survivors benefits to be paid from their work record

- Who is eligible to receive survivors benefits

- How Social Security survivors benefits are calculated

Let’s dive into these details below.

Part I: Is the Work Record Long Enough to Pay Out Social Security Survivors Benefits?

Before any of your beneficiaries to receive survivor benefits, you must work for enough years to be considered “insured” for Social Security.

There are two different ways you can be “insured,” but the big, broad rule is that if you worked for at least 10 years, your beneficiaries can receive survivor benefits. That being said, there are exceptions to this, where beneficiaries could still receive a survivor benefit if the work record is shorter than 10 years.

This is an important rule to understand for individuals who die young. To determine whether a person worked long enough to qualify for benefits, the Social Security administration counts work history by credits.

You have to have a certain number of these credits to be considered “insured” by Social Security. In 2019, you get one credit for every $1,360 dollars in earnings and you can earn up to 4 credits per year. (The earnings amount required for a credit generally increases on an annual basis.)

Depending on the age of death and number of credits obtained at that time, a person will either be:

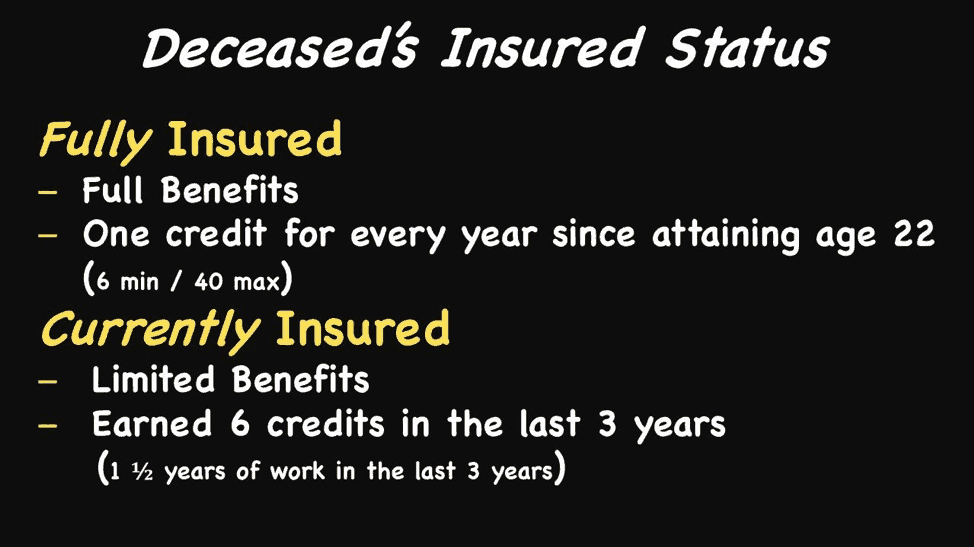

- Fully Insured, which means your beneficiaries can receive full benefits payment

- Currently insured, which means Social Security will only pay a limited amount of benefits.

I’ll get into the weeds on the differences in payments in just a moment. For now, know that to be considered fully insured, you need to have earned one credit for every year since you turned 22. You need a minimum of 6 credits, but you never need more than 40.

For example, let’s say you were to die at 40 (sorry). In that case, you’d need at least 18 credits to be considered fully insured by the Social Security Administration:

Part II: Who Can Receive Survivors Benefits?

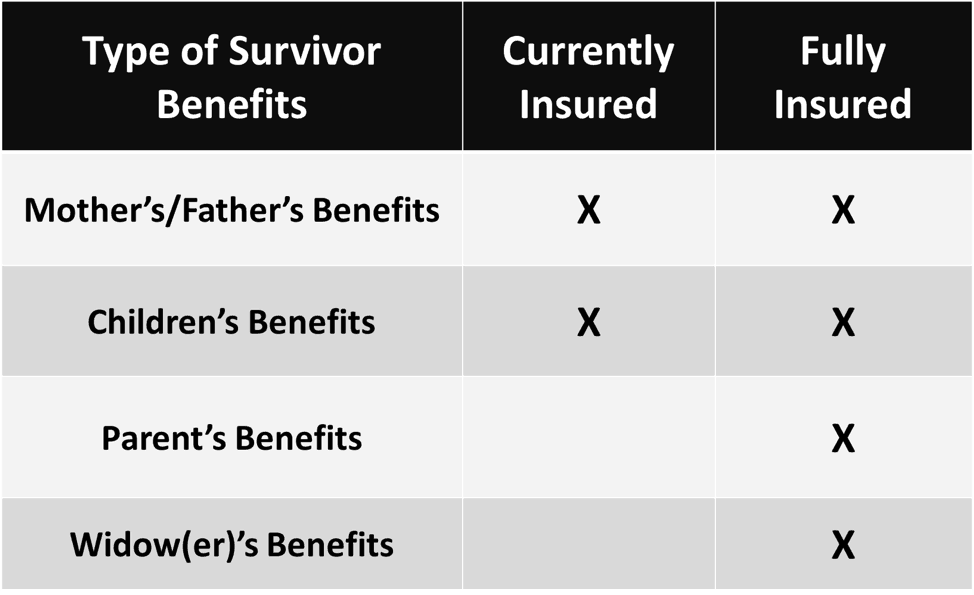

There are four different types of survivor benefits:

- Widow(er) benefits: This is what we traditionally think of when we think about survivors benefits; you die and your spouse can get a survivors benefit.

- Mothers’ and fathers’ benefits: These are also known as child-in-care benefits, and they will pay a survivors benefit to a spouse who is taking care of your children under the age of 16[1]

- Benefits payable to children: Children can receive a portion of your full retirement age benefit up until they reach adulthood.

- Benefits payable to your dependent parents: Not many people know about this one, but in short, they pay benefit to your parents if they were receiving at least one half of their support from you when you died.

These different benefit types each work differently with your insured status. If you are fully insured, your beneficiaries can receive any of these benefit types.

But if you are “currently insured” (or you only have one and a half years of work on your work record for the last three years), then Social Security would only pay out the mothers’ and fathers’ benefits or children’s benefits. Your spouse would not receive parents benefits or the traditional survivor benefits once they retired.

Part III: The Alternate Calculation for Early Death

To really understand how the Social Security Administration calculates survivors benefits, let’s do a quick review of the usual calculation for an individual who has a long work history. There are three basic steps:

- Adjust historical earnings for inflation.

- Get monthly average from the highest 35 years

- Apply monthly average to benefits formula

The result of this three-step calculation is your Primary Insurance Amount, or PIA. This is also your full retirement age benefit. Your own retirement benefit is based on this calculation — and other benefits, like spousal and survivor benefits, rely on your work record as well.

But what happens if you die before you’ve worked 35 years? What if you only worked for 20 years?

With retirement benefits, 35 years are used in the calculation to determine the benefit whether you’ve worked 35 years or not. So if you’ve only worked for 20 years, your earnings history will show 20 years and earnings and 15 years of zeros.

Needless to say, zeros in a calculation will drive down the average. And if someone dies early, then there could be quite a few zeros in their last 35 years of work history, right?

That would be unfortunate, but thankfully, survivors benefits aren’t calculated in the exact same way as retirement benefits.

If someone dies, there is an alternate calculation that differs from the normal calculation in two key areas:

Instead of using the highest-earning 35 years from a work history, the Social Security Administration will take the number of years between the attainment of age 22 through the year of death and drop off the lowest five years.

What’s left is divided by the number of months in those years and that is ran through the formula that’s effective in the year of death.

For a deeper dive in the years used in calculations, see my article Your Social Security Benefit Isn’t Always Based On 35 Years of Work History

For example, say someone named John dies at age 40. The Administration would index his earnings for inflation look at the number of working years on his record beginning at age 22 and ending at death. In this case, that’s 19 years.

Next, they’d drop off 5 of the lowest years. What would be left would be the highest 14 years of John’s earnings. Since there are 168 months in 14 years, his average indexed monthly earnings would be the sum of the highest 14 years divided by 168. The result would then be applied against the benefits formula that was in effect that year.

The Other Key Factor in Calculating Survivors Benefits: Windexing

There’s one other key difference in the calculation here: as long as the deceased person was under age 62 when they died (along with a few other restrictions), the Social Security Administration will perform another calculation to see if it produces a higher result for survivors benefits.

This is called “windexing,” and it’s one of the Administration’s famous word combinations that stands for Widows Indexing. This alternate calculation compares the benefits payable from doing the calculation with the formula in place during the year of death and then with the benefit payable from the year the surviving spouse attains age 60 or the deceased would have attained 62.

This is important because the benefits formula generally increases every year and a higher benefits formula would produce a higher benefit.

Social Security survivors benefit can make life a lot easier for the surviving spouse if a higher-earning spouse dies early. Understanding what to expect in payments, and the basics of the calculations so you can spot inaccuracies, should be a central part of your retirement planning.

If want to learn more, join me and nearly 290,000 others on my YouTube channel and Facebook group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security.

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

Further Resources to Use:

SSA research paper with clarification on the drop out years.

POMS: Base Years, Computation Years, and Divisor Months

Excellent SSA research notes on the WINDEX

[…] Social Security Survivor Benefits: The Complete GuideIf You Die Young: How to Calculate Social Security Survivor Benefits (what everyone between the ages… […]

My spouse died in August 2010 when she was 46 years of age.. I was 44 at the time… I got married to her in 1995 We wee married for 15 years.. While she was alive and for approximately 10 years she collected social security disability for renal failure.. Her two kids was able to collect social security under her work record When the mom died one of her sons was still able to collect social security on her record as the other son was 19 so his SSA payments stopped. I’m currently 53 years of age and I have… Read more »