If you’re receiving Social Security benefits or Medicare and have recently moved, your Social Security change of address needs to be high on your priority list.

“Even if you receive your benefits by direct deposit, Social Security must have your correct address so we can send letters and other important information to you. We’ll stop your benefits if we can’t contact you.”

Ouch! You don’t want that to happen.

Thankfully, it’s pretty easy and painless to get your address changed. You just have to choose which of these three approaches will work best for you.

What do you know about Social Security delayed retirement credits — and how confident are you in that knowledge?

If you don’t fully understand how delayed retirement credits work and how they get added to your benefit amount, you might be disappointed when you receive your first Social Security check after you file.

You should know that when you delay filing for your Social Security benefits after your full retirement age, your delayed retirement credits aren’t added right away.

Here’s why, what else you need to understand, and when you should file instead to minimize the delay.

Why You May Be Missing Credits

Does the Social Security Administration have a little trick up their sleeves when it comes to delaying your benefits?

It can look that way! They do not add your credits immediately if you file after full retirement age.

To be honest with you, this is a little puzzling to me and I’m not sure why they do this. It’s not as if they don’t have the systems in place to do the calculations. After all, if you file early, the reductions are applied immediately!

So why don’t you get the same treatment when you delay filing?

I’m going to show you how this works — but let me give you a little context around this first.

Know How to Calculate Monthly Changes to Your Benefits

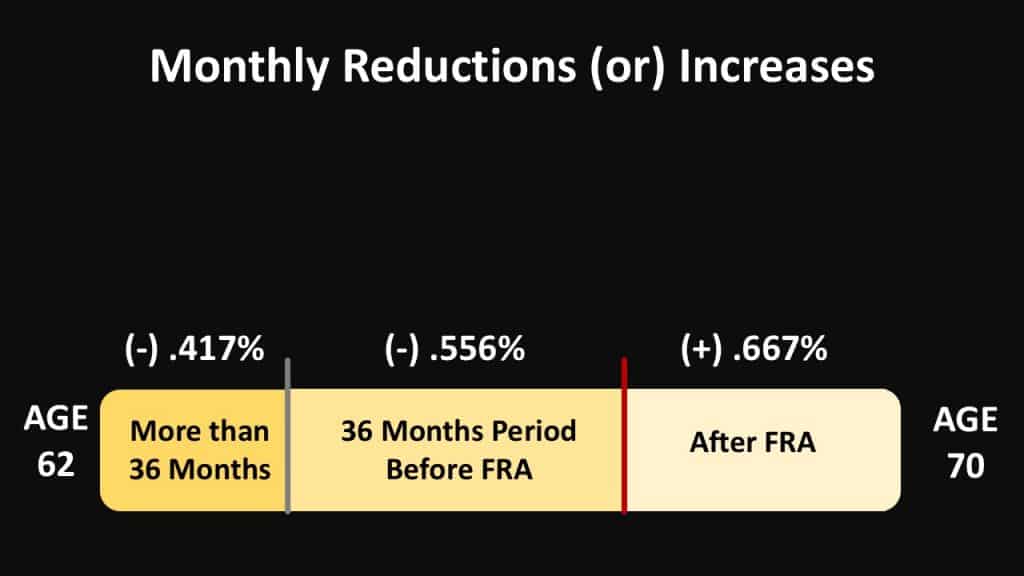

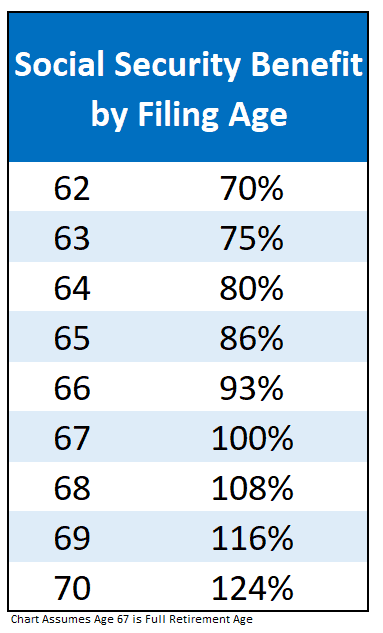

I often discuss the monthly reductions for filing early or increases for filing early, and understanding that is a fundamental part of today’s discussion. Let’s take a look at this chart to start:

You can file for your retirement benefits between the ages of 62 and 70. The red line in the chart above represents your full retirement age.

Knowing this, you can calculate how much your Social Security income benefits should increase if you delay filing — as well as how much those benefits might decrease if you file before full retirement age.

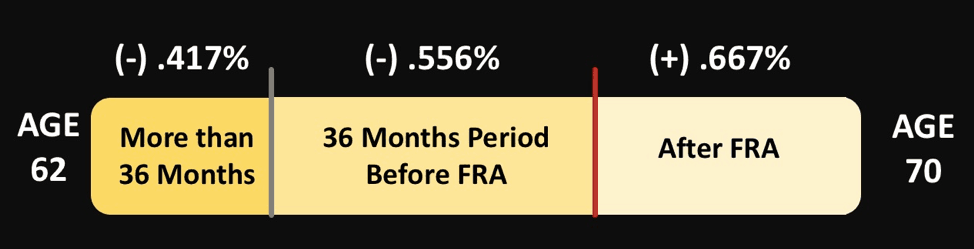

If you file early, decreases are broken up into two separate bands. First, you have the 36 month period immediately prior to full retirement age where benefits are reduced by .555% per month, and then anything more than 36 months, benefits are reduced by .417%.

But if you file after your full retirement age, your benefit will be increased by .667% for every month. These increases are referred to as delayed retirement credits.

What Happens If I File After My Full Retirement Age?

It’s important to understand that there is a difference in how the increases and reductions are applied.

If you file at any time before your full retirement age, your benefit will be calculated by these reduction amounts and immediately reduced beginning with your first check.

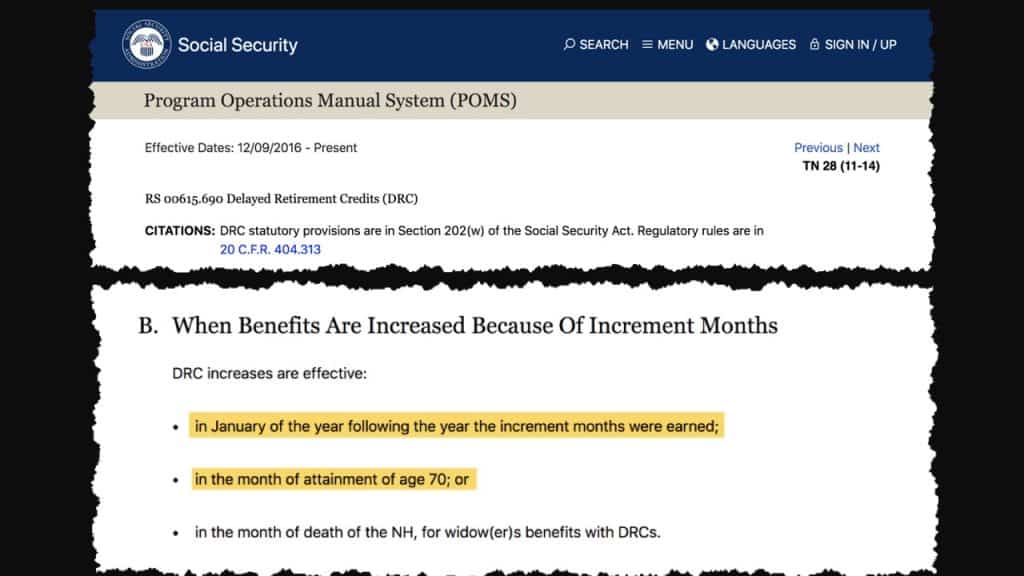

In January of the year following the year you earned the delayed retirement credits.

Let’s look a specific example to better understand this.

Make Sure You Understand the Full Impact of When You Choose to File

Let’s assume your birthday is in February, and this is the year you hit your full retirement age.

Six months later, you decide to file for benefits and you receive your first check in September of that same year.

You’ve probably already calculated in your head that you should receive 6 months of delayed retirement credits; that works out to 4% increase to your full retirement age benefit.

When you get your first check deposited in September, therefore, you might be surprised to find that check is for the same amount as it would have been had you filed for Social Security benefits back in February.

The delayed retirement credits would be added — eventually. The fact that they don’t kick in immediately throws many people off!

You’d probably see the delayed retirement credits come through starting in January of the following year, which means you wouldn’t see it on your actual checks until that February.

And no, you don’t receive any sort of payment to make up for those months that you missed.

Can You Get Your Delayed Retirement Credits Faster?

One way to lessen the lag is to file later in the year.

If you want to avoid this lag altogether, you could wait until your 70th birthday. Then, no matter what month it falls on, the delayed retirement credits are added immediately.

Maybe in the future the Social Security Administration can figure out how to do this for any filing age after full retirement like they do before. It can’t be that hard, right?

One would think!

But for now, this is how the system is set up. It’s important to know this so you can get proactive and plan accordingly — and not get hit with a nasty surprise after you’ve already delayed filing so you can get a bigger benefit.

Take Control, Because It’s Your Retirement and Your Benefits

You’re making a smart move by learning all you can and reading sites like these, but don’t use this as specific advice for your own situation. I encourage you to do your research and talk to your own advisors. Most importantly, continue to educate yourself and stay curious!

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the 400,000+ subscribers on my YouTube channel! For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

We’re taking a look at the math behind a social security strategy that’s been around for a while. Here it is: File early, invest the monthly benefit, and you’ll be able to generate more income than someone who waited until later to file.

Effectively…you can do better on your own. But does it make sense to file early and invest the money?

A Decade of Positive Returns Creates Optimism in Investing

There’s nothing like a decade of positive returns in the market to create optimism for investing. We’re starting to see this optimism affect how individuals file for social security.

A few years ago, there weren’t many people saying they were big believers in the market. We were still recovering from the worst market since the Great Depression, and news was still (mostly) negative.

A few years later, individuals started seeing a few years of positive returns. Some of those have been double digit returns, and optimism began rising.

And so I’ve started to hear more people say things like “Devin, I think I could file early for Social Security, invest it, and create more income down the road than what I would’ve had with Social Security.”

So, You Think You Can Do Better?

Now, I’ve heard things like that for a while, but I’ve never gotten into the numbers to see what was really possible. So…I decided it was time for a closer look.

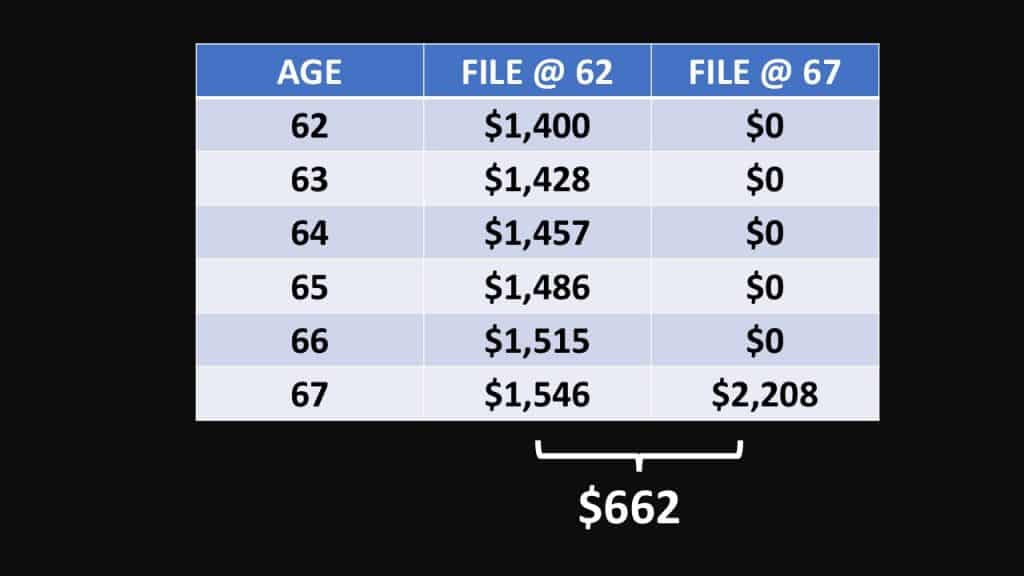

Let’s consider someone with a $2,000 benefit at their full retirement age. For this example, we’ll assume full retirement age is 67.

You can file as early as 62 and get $1,400 or as late as 70 and get $2,480.

Let’s look at two scenarios: First one is where you need to start your income at 67; and the other is where you need to start your income at 70.

In both cases, I’ll assume that you file for benefits at 62. That benefit has a 2% cost of living adjustment (COLA) applied and that you invest the monthly benefits check.

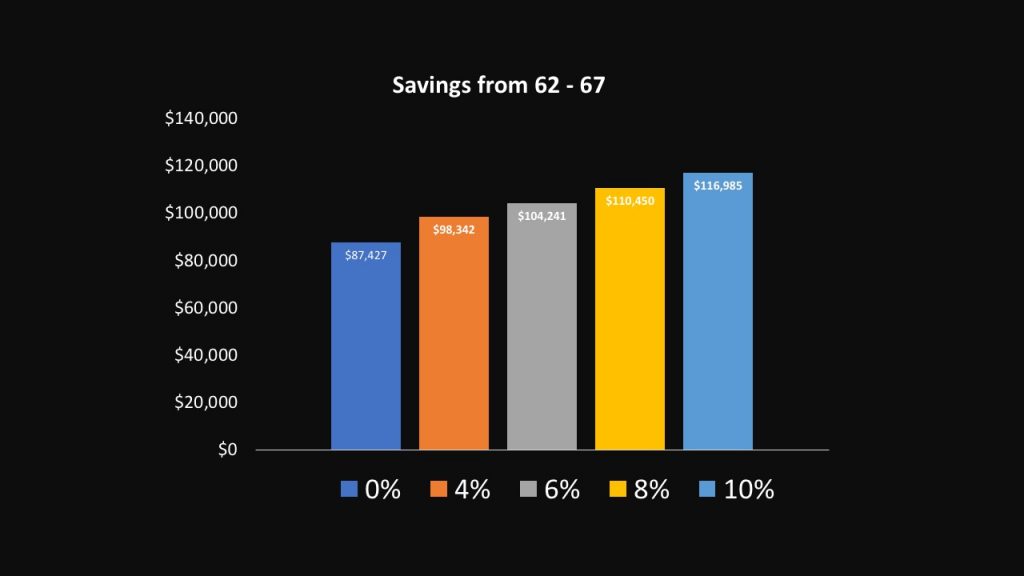

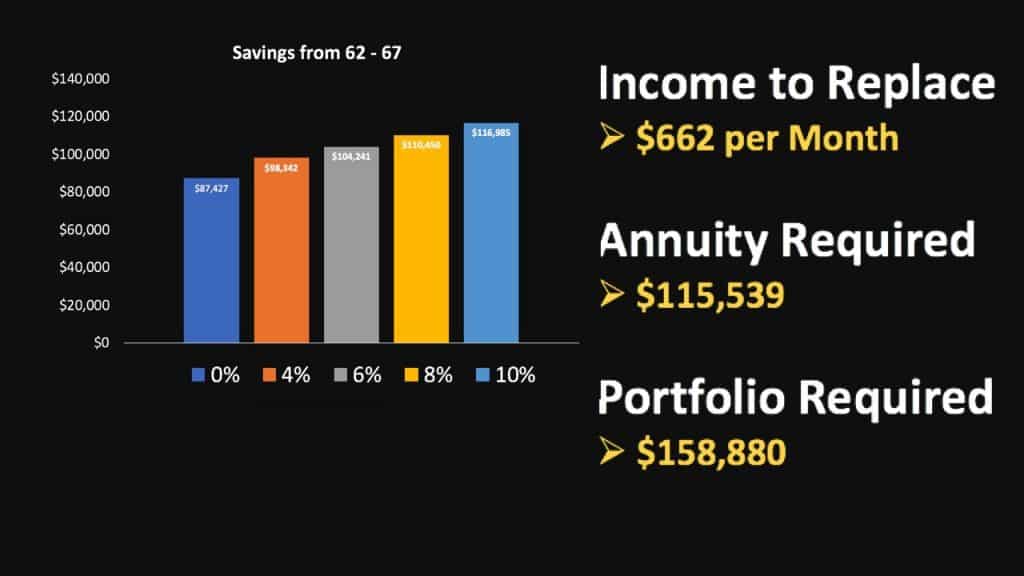

Here’s how that investment would accumulate at various rates of return from the beginning if age 62 to the beginning at age 67:

First, let’s assume you didn’t make anything. That $1,400 would be worth $87,427. At 4, 6 and 8 percent it would gradually increase and the highest rate of return I assumed was 10 percent where your balance would be $116,985. These amounts would be the available balance to use in supplementing your income.

So now let’s look and see what the income gap would be after we adjust for the annual cost of living adjustments. Your benefit would start at $1,400, but by age 67, it would be approximately $1,546 if there was a 2% annual COLA.

The age 67 benefit was $2,000, but when you add the COLA to it, that amount would now be $2,208. So there would be an income gap of $662 that you would need to create from the invested Social Security benefits.

I’m assuming there are two ways to generate this income. First, is an immediate lifetime annuity. This is the closest thing to your Social Security benefit in that it offers a fixed payment that’s guaranteed for your lifetime. The way these work is that you give a lump sum of money to an insurance company and they send you the payments. The other option I assumed was leaving your money invested and taking a 5% annual withdrawal to supplement the income.

And The Results Are In

Here were the results: If you need to generate an income stream of $662 per month, it would require an annuity of $115,539 and an investment portfolio of nearly $160,000.

For the annuity, this would mean that you’d have to achieve an annual return of 10% and for the portfolio option you’d need to get a return of 21%.

Keep in mind…these are the returns needed to break even. You’d have to exceed that to do better that what you’d get with almost no risk from the Social Security administration. I’m not sure how you feel about your capabilities to get consistent investment returns like these, but if you can…maybe you should start a hedge fund. I can tell you that there’s no way I would take that chance with a client’s money.

What If You Invest It For A Longer Period of Time… Does That Work Out?

But what if you have a longer time period?

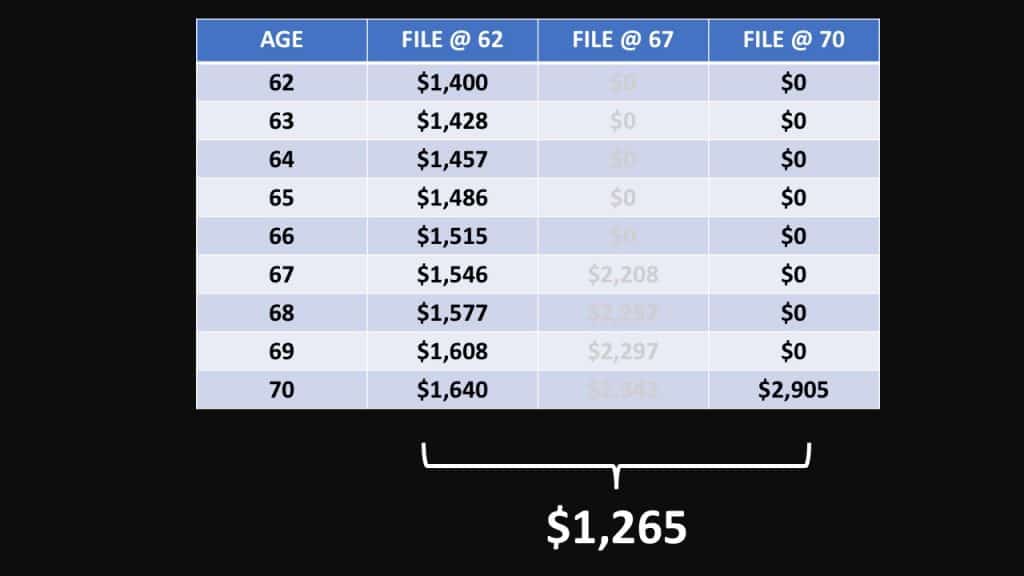

Let’s say that you don’t need the income to start until you’re 70. In this scenario, you’d have from the beginning of age 62 to the beginning of age 70 to receive benefits and invest them. How would the time/value of money change the outcome?

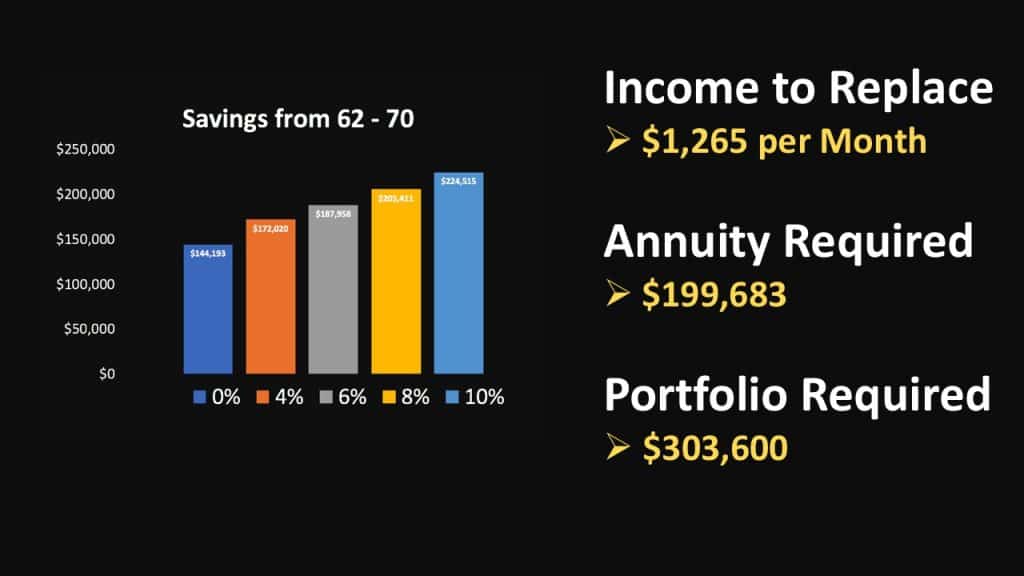

By the time you take your age 70 benefit, it would have grown to $2,905 with an annual 2% cost of living adjustment. That’s an income gap of $1,265 you’d need to cover. Since you’d have a few additional years to invest, the balance of the investment portfolio would be higher than in the prior scenario ranging from 144,000 to 224,000 at 10% annual return.

Now we know you may have saved, but how much would it take to replace $1,265?

You need an annuity of $200,000, and an investment portfolio of around $300,000. This means that for the annuity to work you’d need to get about a 7% return and for the portfolio to work you’d need about a 17% return.

Again…those numbers are just to give you the dollar amount of income that you’d get from Social Security without taking hardly any risk. And, the risk is not the only difference here.

For example, the annuity options do not have survivor benefits, the taxation of an annuity vs. investment portfolio vs. social security is all different so the net amount would not be the same. The annuity options were calculated with today’s interest rates and there’s just no way to know what the interest rates would be in the future and how these annuities would be affected. The investment returns I illustrate are compounded annually and would be slightly different if compounded on a monthly basis. The amount of your social security benefit would also affect the required rate of return on the other options.

This article is based on what we know today with a set benefit amount, but your mileage may vary with your own circumstances.

It’s Your Retirement!

Ultimately, remember…I’m not your financial, legal or tax advisor. This article is meant to help educate you, but not as specific advice for your specific situation. I’d highly recommend that you keep learning and stay curious!

Questions?

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too. Also…if you haven’t already, you should join the 100,000+ subscribers on my YouTube channel!

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

The other day, a piece of economic data came out that is good news for the longevity of the Social Security trust fund. It could mean that the fund DOES NOT RUN DRY in 2034 as was previously forecast. I’ll tell you what it is and why its so important to watch this moving forward.

Are The Headlines Right About Trump Fixing Social Security?

Not long ago I saw a headline that said something like “Trump Administration policies are fixing Social Security.” I couldn’t find the exact one I was looking for but it’s no secret that President Trump has long advocated that the fix is neither benefit cuts nor tax increases, and instead it’s a simple matter of growing the economy and everything will fall into place. And there’s truth to that but we are getting so close to the point where even record setting economic numbers will be too little too late. But what we are seeing is promising!

The specific number I’m referencing is the unemployment rate. Economists believe this to be one of the most important economic indicators because of its far-reaching effect.

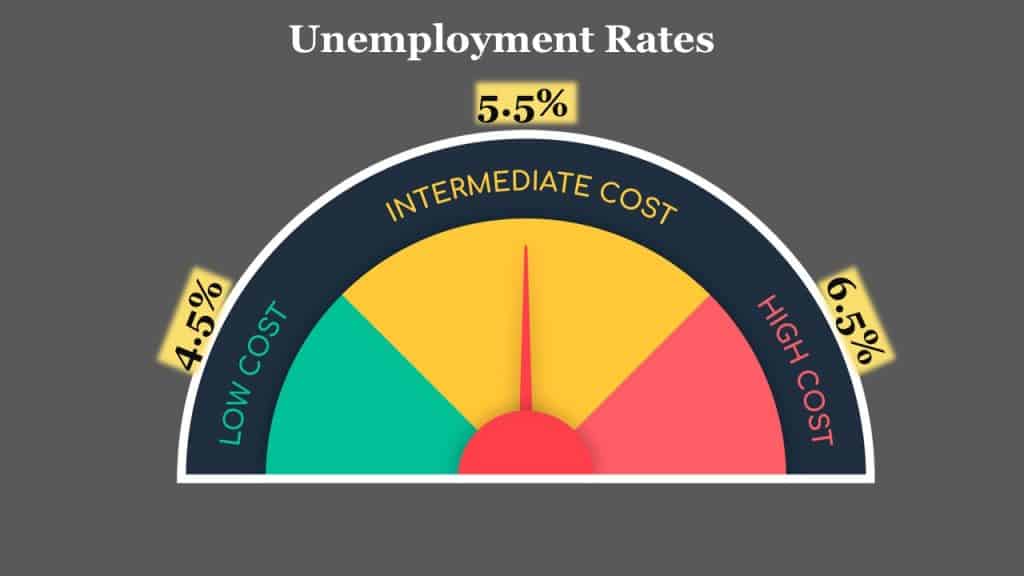

Unemployment Rate as a Factor

In the Social Security trustees’ report, they list the unemployment rate as one of the factors that will determine how long the funds last. In a very simplified explanation, this impacts the trust fund because with more people working, there are more taxes being paid into the social security trust fund. Thus, the retiree to worker ratio is improved.

Now, in this report they forecast an intermediate cost, high cost, and low cost scenario for all of the various factors.

The intermediate cost is where they get the assumption that the SS trust fund will be dry by 2034. If the cost goes down, the trust fund will last longer. If the costs go up, it won’t last as long.

The intermediate cost assumption they are using for the unemployment rate is 5.5%. The lowest cost scenario they show is 4.5%. But, for the first time in a very long time, the unemployment rate has dipped below 4%.

As of the last report it was at 3.8%. If it stays down here for long, the Social Security trustees will have to revise their estimates.

What Does This Have To Do With President Trump?

So what does this have to do with President Trump?

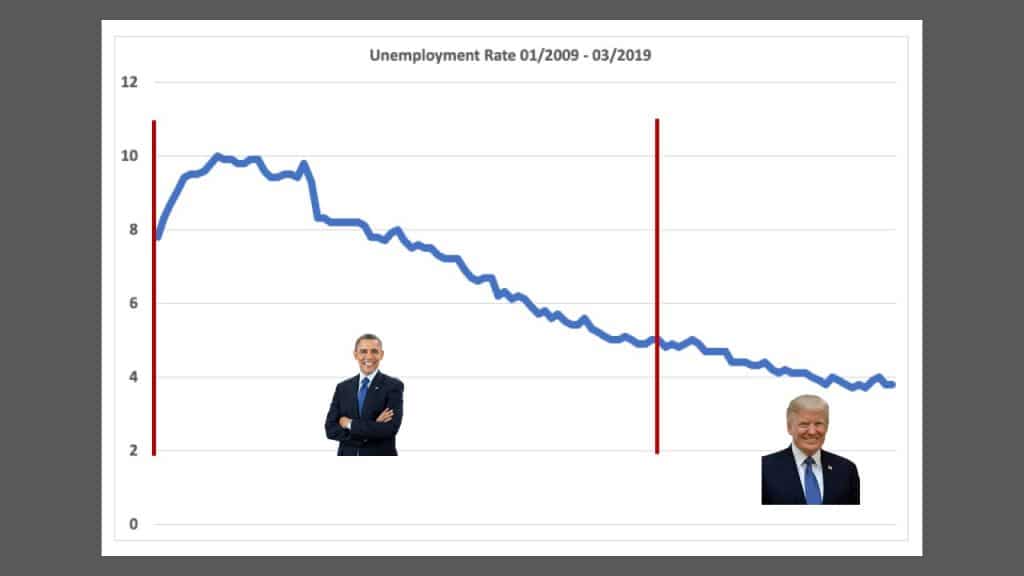

Well, he’s the president while unemployment rates have been pretty impressive.

Since 1969, unemployment rates for the year end have only gone under 4% twice. 2002 and 2018. The question is, is this a result of the policies of Donald Trump?

Yeah…I’m not about to answer that.

If you look at unemployment rates for the last decade, you can see that except for an increase at first, they’ve been coming down for the last nine years.

Is this because of the policies of President Obama? Could it be because of President Bush’s policies before President Obama was in office are finally being felt? We could take this back for decades.

The truth is, I think the President has less to do with the economy than we think. I mean, they don’t control monetary policy, so at best they have short term impacts on the stock market and an indirect effect on the economy.

The point is not to play politics or any of that nonsense. Its to remind you that these trustees’ reports are using assumptions THAT CAN and do CHANGE. And as things change, you can count on me to let you know.

It’s Your Retirement!

Before we go, I want to thank you for taking the time to get informed. So many people rely on hope that everything will work out. Sometimes it does, but sometimes a lack of planning can ruin what should be your best years. This is your retirement! Please continue to stay informed!

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

It’s important for you to have a clear understanding of the process used to calculate your Social Security benefits. If you understand this calculation, you may be able to spot mistakes and fix them before it’s too late.

Like anything with Social Security, the rules can seem complex at first. But once you get under the surface, they are actually pretty easy to understand. To help you, I distilled the several pages of calculation rules down into four easy-to-understand steps.

Why Do I Need To Know How To Calculate My Social Security Benefits?

So you may be thinking, “Why do I need to know how to calculate my own Social Security benefits? After all, the SSA will give me an estimate at any time.”

That’s true! You can go to your My SSA account online and see an up-to-date copy of your benefits estimate. So why would you need to know how to do this calculation on your own?

It’s important for a few reasons.

First, it never hurts to understand the mechanics behind an income stream that’ll probably be a large part of your overall retirement income.

This means that these estimates are less accurate for younger workers but more reliable for workers who are close to retirement.

So, understanding how to do this calculation is especially important if you plan to retire early or later than “normal” or if you have a significant earnings change in the last few years of working.

To do this calculation, there are only four steps.

Adjust all earnings for inflation

Calculate your Average Indexed Monthly Earnings (AIME)

Apply your AIME to the benefit formula to determine primary insurance amount (PIA)

Adjust PIA for filing age

Social Security Calculation Step 1: Adjust all earnings for inflation

So let’s jump in with calculating your AIME. To do this, you’ll need to get use a notepad or a tool like Excel/Google Sheets.

You’re going to need six individual columns with plenty of room underneath for your information. Set up your columns with the following headings: Year, Age, Actual Earnings, Indexing Factor, Indexed Earnings, Highest 35 Years.

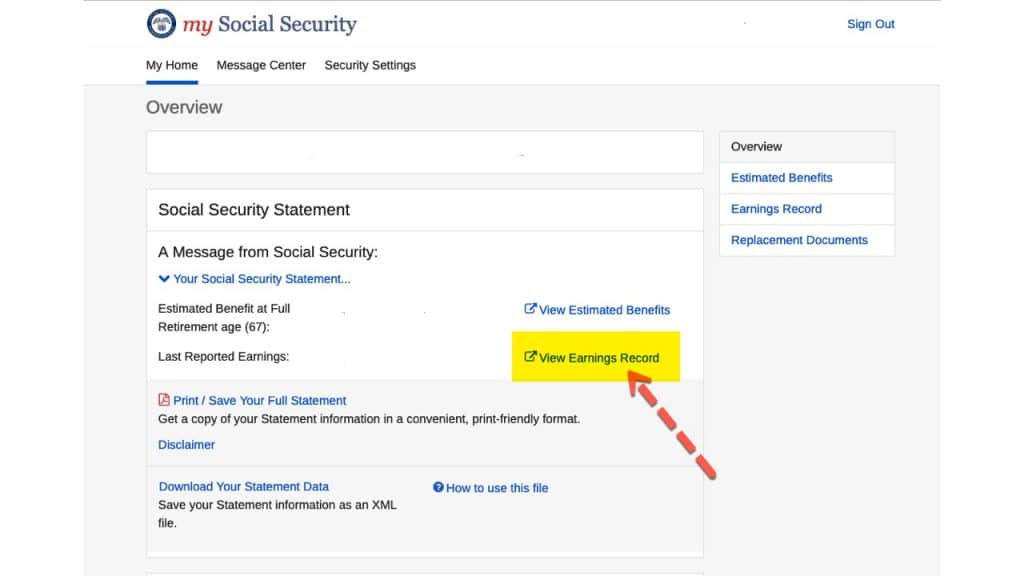

The first two headings are the year and your age. Go all the way back to the first year you had earnings that were taxed for Social Security. You can find a complete record of this by going to your online SSA account and click the link that says “view earnings record.” If you don’t have an online account, it’s very easy to set one up.

This may seem a little redundant to put the year and your age, but it’ll make another step a little easier.

Now you just need to copy down the information from the SS earnings history. You’ll want to use the part that says “your taxed Social Security earnings.” Don’t skip a year, even if there were no earnings. Just put a zero in.

Once you have all of your historical earnings recorded, it’s time to adjust them for inflation. The SSA uses an indexing factor to make sure your future benefit has kept up with inflation, but still based on your earnings.

Important note here…only your earnings through age 59 are indexed. All earnings at age 60 and beyond are used in the calculation at face value with no inflation adjustment applied.

Also…When you’re getting your indexing factors, you have to be careful to use the factors specific to your age.

The easy way to get these is to visit the SSA web page on indexing factors. At the bottom of that webpage it says, “Enter the year of eligibility for which you want indexing factors.” This should be the calendar year you turn 62. It’s really important to use this year to make sure you get the correct indexing factors.

Now that you have your indexing factors, just copy them on to the sheet. Be sure to keep your years matched up.

Once your indexing factors are written down, you simply need to multiply your actual earnings by your indexing factor. This will give you your indexed earnings.

Social Security Calculation Step 2: AIME Calculation

Now, all you have to do is extract the highest 35 years of indexed earnings.

If you’re still working and don’t have 35 years, you’ll need to estimate what your future earnings will be and apply the indexing factors just as you would for actual historical earnings. This is where you can start to play around with the numbers to see the various impacts of retiring early, or working later or maybe having variable earnings close to retirement.

Once you have your highest 35 years in the last column, you just need to sum them up and divide by 420. You divide by 420 because that’s the number of months in 35 years and we need to get your average earnings expressed as a monthly number.

Once you do this, congratulations…you have your AIME and have finished the first (and hardest) step of the calculation. It’s downhill from here.

Social Security Calculation Step 3: Primary Insurance Amount (PIA) Calculation

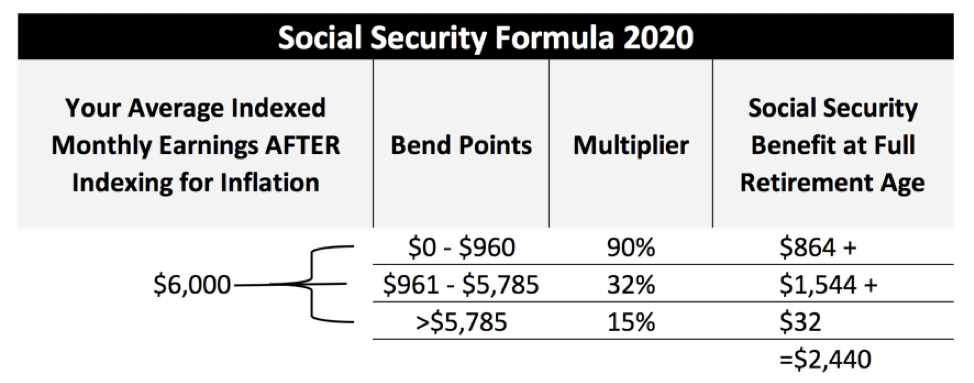

Now you’re ready to determine the heart of your benefit; your primary insurance amount (PIA). The PIA is simply the result of your benefit calculation and is generally your full retirement age benefit amount.

This is calculation is accomplished by using the “bend point” formula that’s in effect for the year you attain age 62. If you aren’t 62 yet, you’ll need to forecast what the bend point formula amounts will be in the year you turn 62. These change annually based on the change in annual wages and generally increase at 3-4%.

There are two numbers that make up this formula which are separated into three separate bands: The amount up to the first number, the amount between the first and second number, and the amount above the second number.

For earnings that fall within the first band, you multiply by 90%. That is the first part of your benefit.

For earnings that fall within the second band, you multiply by 32%. That is the second part of your benefit.

For earnings that are greater than the maximum of the second band, you multiply by 15%. This is the third part of your benefit.

The sum of these three bands is your benefit amount at full retirement age: your PIA, or Full Retirement Age benefit amount.

In the example image below we illustrate an individual with an AIME of $6,000 being applied to the bend point formula.

Now that you’ve calculated your average index monthly earnings and applied them to the PIA formula, you simply need to figure out how your filing age will impact your benefit amount.

Social Security Calculation Step 4: Adjust for Filing Age

The easy way to look at it is to think about it in annual numbers.

Your benefit will be lower if you file at 62 and higher if you file at 70.

If you file after your full retirement age, your benefit will increase by 8% per year. If you file in the 3 year window immediately prior to your full retirement age your benefit will decrease by 6.66% per year of early filing. For anything more than 3 years before your full retirement age, your benefit will decrease by an additional 5%.

A lot of people don’t want to retire on their birthday so it’s important to break this down by a monthly amount.

Monthly Increase/Decrease Percentages

After your FRA, your benefit will be increased by .667% per month you delay.

For the 36 month period before full retirement age your benefit is reduced by .556% and for more than 36 months it is reduced by .417% per month.

And that is it! Once you’ve gotten through this step you’ve successfully calculated your Social Security benefit.

It’s your retirement!

Before you leave I’d recommend staying connected with my content so you won’t miss anything. In many cases, I’ll publish my newest stuff on YouTube (with more than 400,000 subscribers!) and then have a discussion in my Facebook group.

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

Social Security benefits are changing forever at the end of 2020.

Here’s what’s going on.

Let’s Start with a Critical Factor: Your Full Retirement Age

Under the original Social Security Act of 1935, workers had to reach age 65 to receive a full retirement benefit.

This “full retirement age” was actually simply based on the fact that many state pension systems and the Railroad Retirement Benefit system used age 65, so, the Committee on Economic Security – the group that designed the US SS system – decided to go with an age that was already commonly used.

They also considered using age 70, but ultimately decided that age 65 was more reasonable. Bottom line? Their choice was pretty subjective!

This full retirement age didn’t change from the beginnings of Social Security all the way until 1983.

This was the other time in history where, like today, the Social Security trust fund faced a crisis and nearly ran out of money! To keep this from happening, The NATIONAL COMMISSION ON SOCIAL SECURITY REFORM (which is more commonly referred to as the Greenspan Commission) made a series of recommendations to Congress about how to keep the program solvent for the next 50 years.

How Changes to FRA Impact Your Ability to Get Full Social Security Benefits

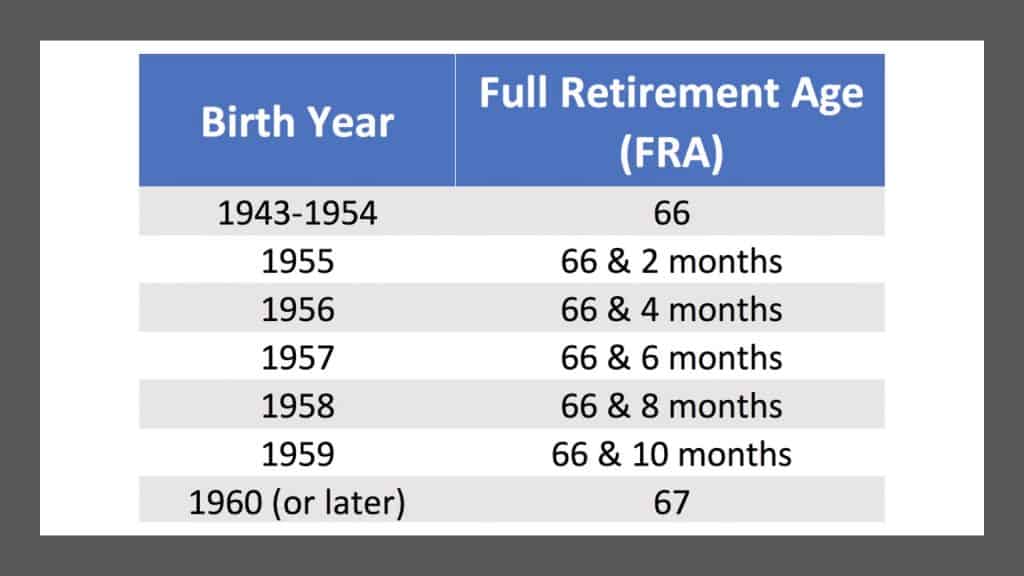

One of the Greenspan Commission’s big recommendations was to increase the full retirement age to age 67. To make this change a little easier to digest, they recommended that the change only impact those who were more than 20 years away from full retirement age and that the change would gradually phase in over a period of 22 years.

The first changes began by changing the age from 65 to 66. It stayed at 66 for 11 years. But now… it’s going up again.

For those born between 1955 and 1959, the full retirement age will be somewhere between age 66 and 67. For everyone born in 1960 or later, the FRA will be 67 (for now).

This takes us back to the beginning where I said that you’ll never be able to get as much in benefits in 2021 or later. Here’s why.

Why You’ll Never Get As Much in Benefits After 2021

For years we’ve used nice round numbers when calculating the impact of filing for social security benefits early, or later. We’ve said if you file at 62 you’ll get 75% of your FRA benefit amount and if you wait until 70 you’ll get 132% of your benefit amount.

Well, guess what? Not anymore!

Because the increases and reductions are calculated on a monthly basis, once FRA increases, there will not be as many months for benefits to increase by.

The inverse will also be true, the reductions for filing at the earliest age will be steeper because there will be more months between age 62 and full retirement age.

This is why I stress understanding how to calculate the reductions and increases on a monthly basis. (by the way…the full retirement ages, age-based reductions, and a lot more are all covered in my easy to understand Social Security Cheat Sheet. This is where I took the most important stuff from the 100,000 page website and condensed it down to just ONE PAGE! Get your FREE copy here)

How The 2021 Changes Will Affect Social Security Benefits

Here’s how this changes the benefits and reductions if we look at filing at the earliest age and at the latest age.

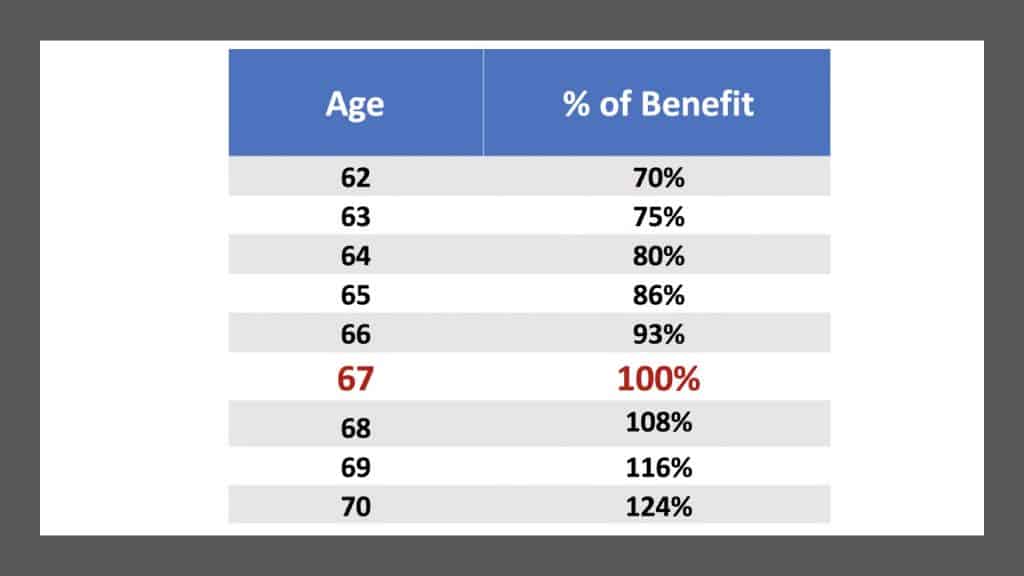

Currently, the SS filing window is between 62 and 70. You can’t file before 62 and it doesn’t make sense to file after 70.

So, for those born between 1943 and 1954, the FRA is 66, you are entitled to 100% of your benefit.

You can file as early as 62, but you’ll only receive 75% of your benefit. If you file at 70 you’ll receive 132% of your benefit. Once the FRA starts moving up, it all changes.

You’ll still be able to file at 62, but you’ll only receive 70% of your FRA and if you delay…your benefit will increase to 124% instead of 132%.

Don’t Just Hope Everything Will Still Work Out — Get Proactive and Plan Now!

Many people just hope everything will work out in retirement. Sometimes it does, but sometimes a lack of planning can ruin what should be your best years. This is your retirement! Please continue to stay informed. You should start by getting your FREE copy of my Social Security Cheat Sheet. This is where I took the most important stuff from the 100,000 page website and condensed it down to just ONE PAGE! Get your FREE copy here.

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the 274,000+ subscribers on my YouTube channel! For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing: There is a tremendous amount of misinformation out there about the changes in 2021. Help me clear up the confusion by sharing this article on Facebook. Thanks!

If you had to replace your Social Security benefits with another form of income, how much would you need to save up in order to live off of in the future?

It’s probably more than you think.

The fact is, the income you receive from Social Security may deserve more respect than it currently receives. It’s easy to dismiss your benefits as “too little” or “not enough.”

And it might sound crazy to call Social Security a good investment.

Can We Call Social Security a Good Investment?

But to be honest with you, in all the years that I’ve helped folks with retirement planning, Social Security income is the only income stream that I’ve seen with the following attributes:

It’s adjusted almost every year for inflation

It’s not 100% taxable

It’s backed by the US Government

It will pay you for as long as you live

That’s a long string of benefits for one income source. So how much would you need to replace your benefit? Another way of asking that question is, what kind of value you actually get from your Social Security taxes?

Or, even better: is Social Security a good investment?

If you could stop paying into the Social Security system and just invested that money on your own instead, could you create as much income for your future self?

We can do a side-by-side comparison of the Social Security benefits you can expect to receive and the result of investing the money you have to pay in on your own instead to determine if it’s true Social Security a good investment.

What’s Better: Investing the Tax You Have to Pay on Your Own, or Paying In and Receiving Social Security Benefits?

This isn’t just a random question to ask. I receive a lot of comments about opting out of Social Security, and investing the money you’d normally have to pay in to the system on your own instead.

Since my research tends to be driven by curiosity, I decided to take a deeper look at the numbers and see which would work out better…

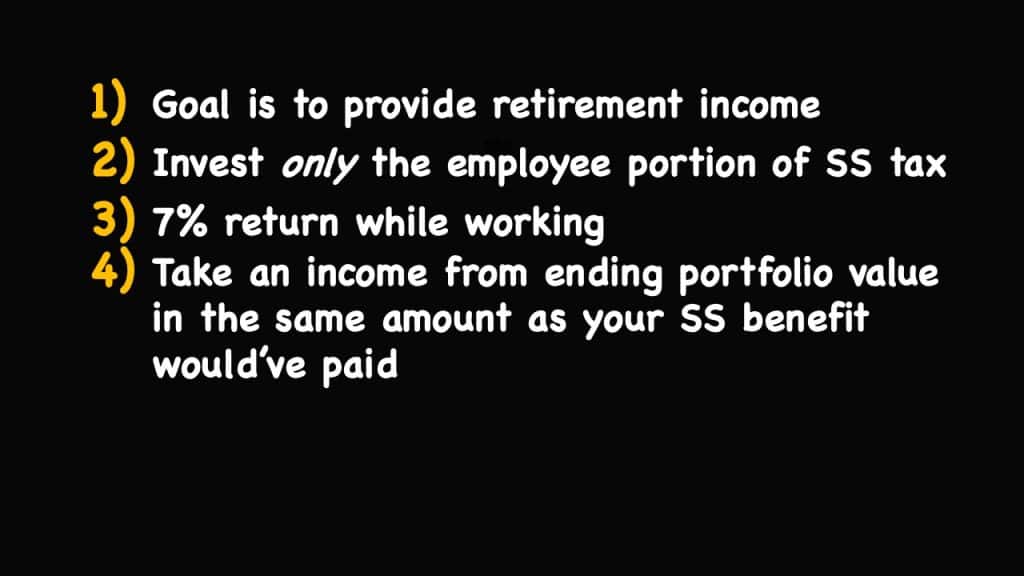

To get the results I made a few assumptions.

First, I assumed that your goal would be to create income in retirement as opposed to buying a vacation house or something else that would require a lump sum.

Second, I assumed that you took only your part of the Social Security tax you currently pay and invested it.

Why? Because the total FICA tax is 15.3%. If you are an employee you only pay half of that, or 7.65%.

Of that amount, 1.45% goes to Medicare and 6.2% goes to Social Security. It’s that 6.2% that I assume you invest for the purposes of these calculations.

We could chase the rabbit trails of investing the full Social Security tax, but if opting out were allowed, I hardly think an employer could be compelled to give you the other 6.2% to invest on your own.

And ultimately, I wanted to look at “what if you could invest the dollars that you currently have to put into the system?”

Next, we assume a 7% return. Obviously you may do better (or worse) than this.

This in itself raises another assumption to consider: Would you continue to get a 7% return on your investment in retirement, or would you move your money to an investment that may have less market risk when you actually needed to rely on being able to withdraw from your nest egg for income?

If you did, you’d most likely get a lower return at some point in the future. So, in the calculation, I modeled out two rates of return after retirement: 7% and 3%.)

Then, at your full retirement age, the invested balance would be used to fund an income stream that would be equal to the amount of Social Security income for which you would have been eligible.

There are multiple ways to illustrate the withdrawal, but this is the only way to keep it apples to apples.

Finally, I looked at multiple income levels while working in a job from age 19 to 66. To get a baseline, I used the national average wage index which is published by the Social Security Administration:

The first income level was for an individual at 50% of the national average wage index.

Then I looked at 100%, and then at 150%.

For a maximum SS benefit, I also looked at an individual who would’ve earned the maximum taxable wages for every year he or she was working.

With these earnings figures, I used the calculator on the Social Security website to calculate what the benefit for each of these income levels would be at full retirement age.

I then increased that amount by 2% per year to keep up with the cost of living adjustment provided by the Social Security Administration, and that’s the number that I illustrated withdrawing from the portfolio accumulated from the invested Social Security taxes.

Now that you know all of the parameters and assumptions, are you ready for the results?

Here they are…

Do the Numbers Say Social Security Is a Good Investment? The Results

For an individual at 50% of the average wage index, the portfolio value of the money invested would last beyond the expected 85 year life expectancy if invested at 7%.

But if that portfolio received a 3% return instead, this person would run out of money at age 80.

This is because a lower income individual would have a larger Social Security benefit relative to the amount of taxes they’ve paid in, and the withdrawal percentage would be higher for them.

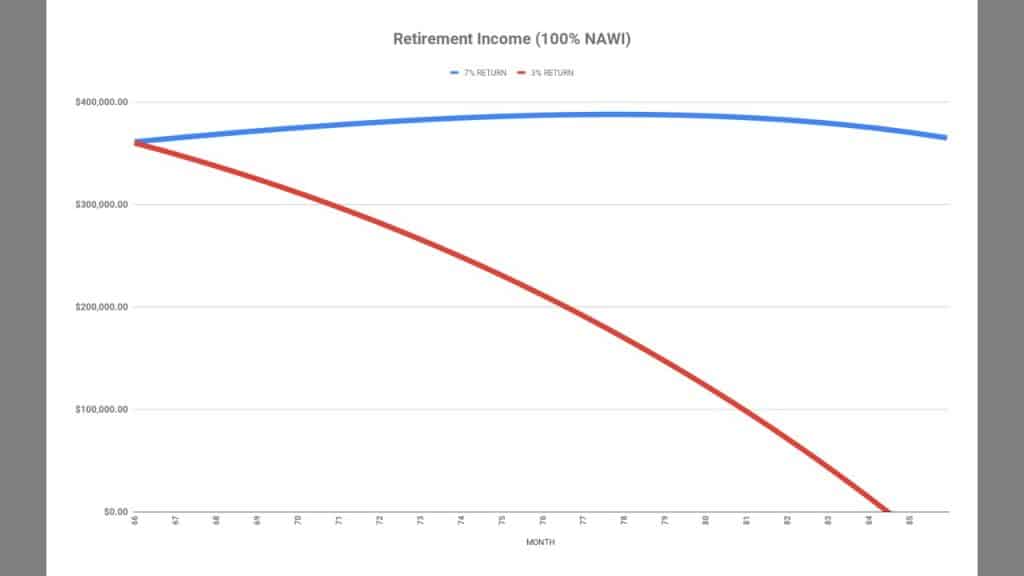

Next I looked at an individual at 100% of the national average wage index. At a 7% return, their invested money would last well beyond age 100.

But they too would run out of money if they only received a 3% return, although they’d at least get a few more years out of it. The money would run out at age 84.

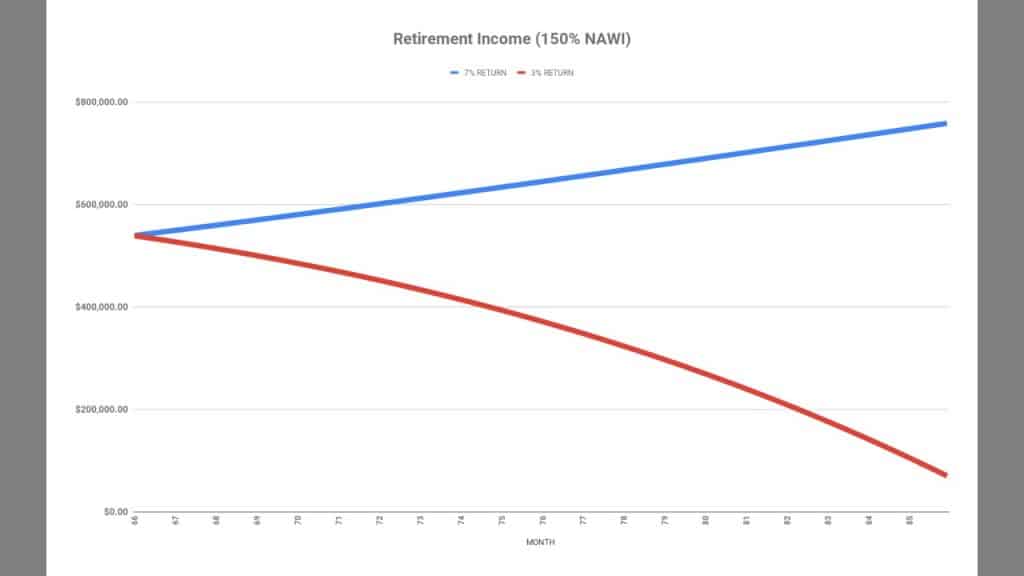

This is where things change… If an individual had earned 150% of the NAWI they would see their benefit increase and would have more in their account when they died than when they started. At 3% it would still last until around age 90.

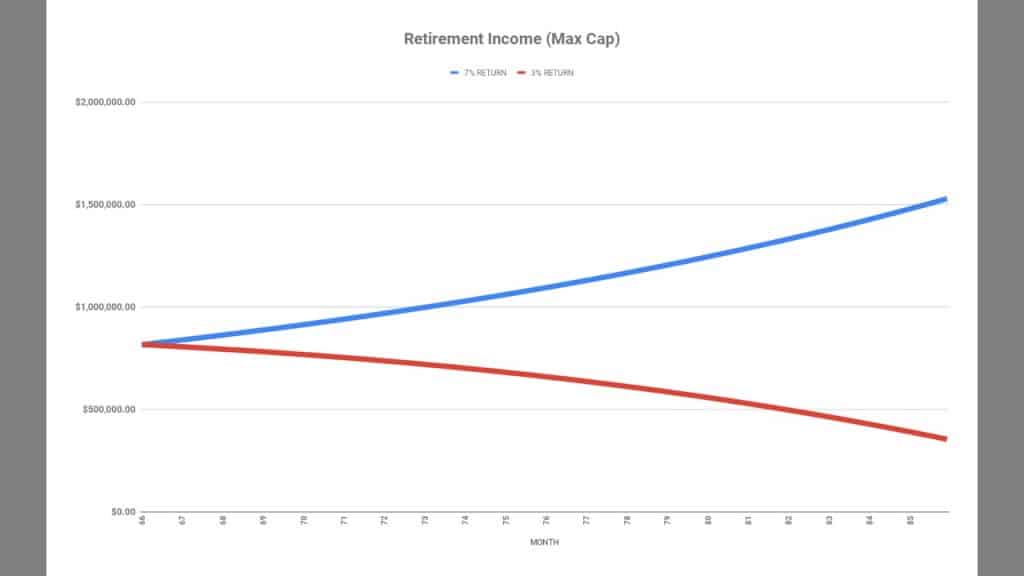

And finally, an individual who had earned the maximum wage base on an annual basis would see similar results except this time they would never run out of money in either scenario during a normal life expectancy.

To make sure my numbers were right, I spoke with Dr. Brandon Renfro. Dr. Renfro is a finance professor and a numbers guru. Things checked out!

If You’re Wondering Is Social Security a Good Investment… It Depends on Your Income

Considering we don’t actually have the option to withdraw ourselves from the system regardless of what these results tell us, it’s fair to ask: what’s the point of all of this?

Hopefully you can see that, depending on your income level, Social Security provides a better chance of having income throughout your life than investing on your own and hoping for a big enough return.

If you’re a lower income earner, then investing on your own may leave you in a worse spot than paying into the Social Security system and receiving benefits. And if you earn more income? Then you have a better shot of your own investments providing more money — but again, that depends on your investment choices and your returns. It’s certainly not guaranteed the way a Social Security benefit can be.

Take Action!

Remember: this is your retirement. Stay curious and STAY INFORMED.

You’re making the right moves by reading articles like these, but don’t use this as specific advice for your own situation. Do your research and talk to your own advisors. Most importantly, continue to educate yourself.

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group.

It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the 100,000+ subscribers on my YouTube channel! For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing that you don’t want to miss: Be sure to get your FREE copy of mySocial Security Cheat Sheet. This handy guide takes all of the most important rules from the massive Social Security website and condenses it all down to just one page.

It’s no secret that the Social Security Administration is staring down a big problem: funding for the program is set to run out, and fast.

That’s a scary thought if you’re approaching retirement or plan to rely on Social Security benefits to handle your living expenses in the future.

And it’s tempting to think that what sound like common sense solutions could actually fix the problem.

One such “common sense” answer is also one of the most popular suggested fixes for Social Security that I hear. What is it?

Simply increase or eliminate the maximum taxable wage base, and make high-income individuals “pay the same as everyone else.”

The truth is that while “scrap the cap” makes a great political rally chant, it is not the conclusive fix for Social Security’s funding problems.

Can’t We Just Make The Rich Pay More in Order to Fix Social Security?

Many, many people believe that the Social Security system is broken thanks to income inequality. Others think that the Social Security program, something that was designed to help the poor, is actually stacked in the favor of the wealthy.

Do these claims have any merit?

While it’s true that income inequality does exist, I wanted to find out if the insolvency of the Social Security trust fund could really be fixed by raising taxes on the wealthy.

Thankfully, I didn’t have to launch my own research project or hire a room full of Ph.Ds. The Congressional Research Service has already done the heavy lifting for me in a report that was last updated in late 2019.

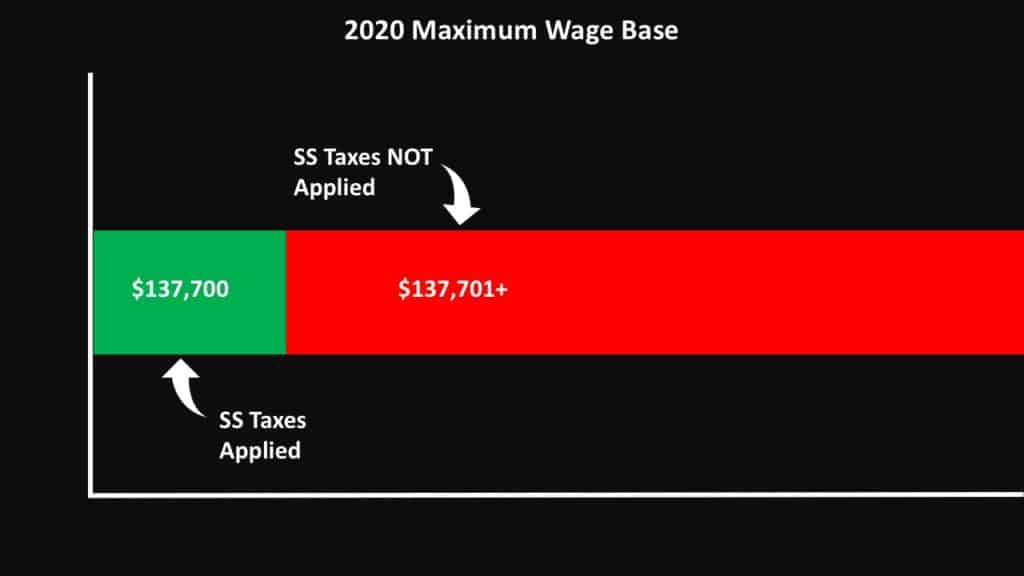

Before we get into their findings, let’s take a look at what the issue actually is. In 2020, the first $137,700 dollars in wages are subject to a 12.4% social security tax. Wages over that amount are not subject to that tax.

The maximum wage base for 2020.

The fact that wages over a certain amount aren’t taxed led (and still leads) lots of politicians and talking heads to suggest that the easy fix to all of the Social Security funding issues can be found within two options, both of which involve raising the amount of maximum taxable earnings:

Option 1: Completely Eliminate the Minimum Wage Base: In other words, this solution essentially says, “if you make a million dollars you should pay Social Security taxes on that full million in income.”

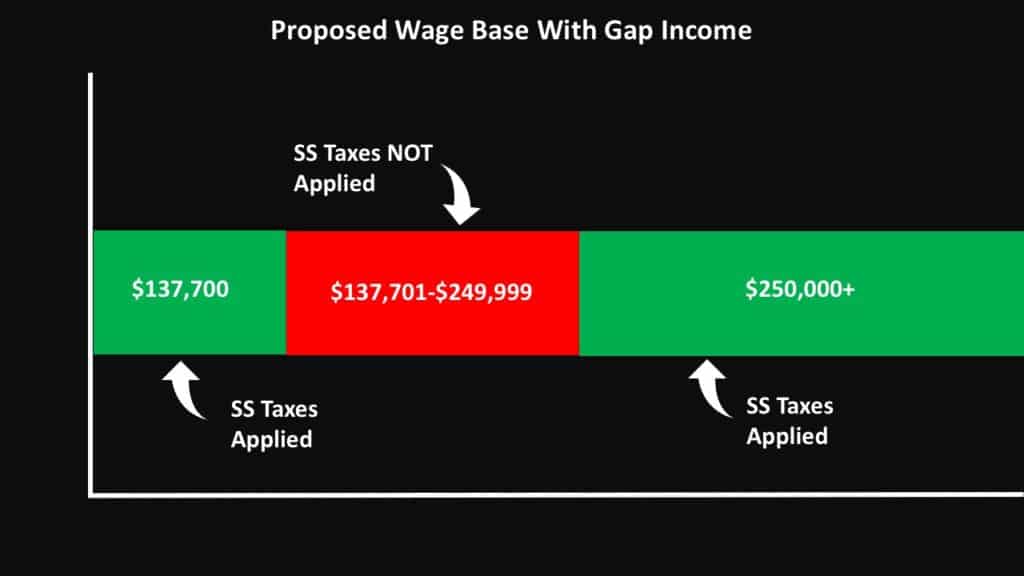

Option 2: Have A Gap On Taxable Income: In this scenario, the current maximum would stay in place but there would be an earnings gap where the tax would not apply. Once earnings exceeded a certain level the tax would become applicable again. This method is really the same as completely eliminating the wage, it just takes more time to get there. Because the first number is generally increased every year to keep up with the annual increase to average wages, and the second number would not change, it would only be a matter of time before the first number caught up to the first number thus eliminating the gap.

Social Security Wage Base with a gap in the amount of earnings that are subject to the Social Security portion of FICA/SECA taxes.

Why Taxing the Rich Will Not Fix Social Security

One of the big unanswered questions of increasing the wage level at which Social Security taxes are applied is that, if the cap is modified, do increased taxes add to Social Security benefits?

For example, if I begin having to pay additional taxes for social security… do I get credit for that? Will the additional taxes increase my future social security benefit?

Currently, there are at least three suggested methods for calculating how these additional tax will, or will not, contribute to a future social security benefit.

Option one is where there is no credit given for the additional taxes paid in beyond what the maximum taxable cap would have been under the old calculation method. If there is no credit given to benefits, and those tax dollars paid in have no benefit returned, it would fix 83% of the 75-year shortfall.

Option two is to continue crediting the higher earnings to a future benefit the same way it is now. Currently, an individuals earnings history is broken into three bands. The lower earnings are credited to a future benefit at the rate of 90%, the mid earnings are credited at a rate of 32% and the higher earnings are credited to a social security benefit at a 15% rate. In this scenario the 15% crediting rate would be applied to all of the additional earnings.

Using the current formula, this would fix 68% of the shortfall.

The third option is to use a new formula, which would credit the increased taxes above what the maximum taxable cap wou;d have been to your benefit at a 2-3% rate. This option would fix 76% of the shortfall.

Does it seem like something is missing? The closest that any of these get to fixing the shortfall is the super-harsh method where the taxable wage base is completely eliminated and there would be NO credit to the contributor’s future benefit amount.

Is it likely that a Social Security payroll tax increase will be part of the overall solution? Yes, but by itself it will not fix the problem. Next time you hear someone shouting that, tell them you know better.

It’s Your Retirement. Shouldn’t You Take Control?

Before we go, I want to thank you for taking the time to get informed. Don’t be one of the people who just float into retirement and hope everything will work out.

Sometimes it does, but sometimes a lack of planning can ruin what should be your best years. This is your retirement! Please continue to stay informed!

Be sure to subscribe to my site so you won’t miss any of the new content coming out, plus you will receive the blueprint version of my book for free.

Alternatively, you can just head over to Amazon and buy the full version. I can’t guarantee this, but I’m pretty sure you’ll get more value than the $12 it costs.

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the 100,000+ subscribers on my YouTube channel! For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing that you don’t want to miss: Be sure to get your FREE copy of my Social Security Cheat Sheet. This handy guide takes all of the most important rules from the massive Social Security website and condenses it all down to just one page.

The push to privatize Social Security hasn’t been discussed much lately. That’s too bad. It’s probably the best (and least intrusive) option to save Social Security that NO ONE is talking about.

This option was almost used in the late 90s and if it would have been implemented, we probably wouldn’t have the issues with the solvency of Social Security that we have today. But it may not be too late!

Over the past 10 years its been often repeated that the solvency issue of the Social Security trust fund can only be fixed by either increasing taxes or cutting benefits. Without one of these, there will be a 20% shortfall by the year 2034.

Wrong!

There is a third option that’s rarely discussed. In fact, its become a bit of a third rail. If you touch it your political career may be over. That third option is to privatize Social Security by investing part of the assets in the trust fund.

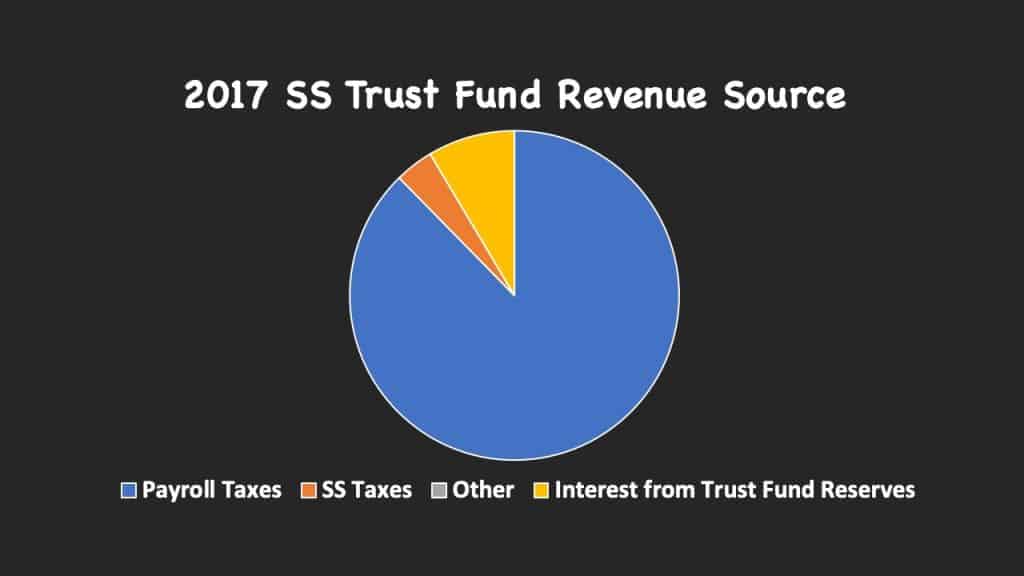

So how would it help to privatize Social Security? The quick answer is that there is a 2.9 trillion dollar balance in the trust fund that’s earning a measly 2.7%. If the rate of return could be increased, the funds would last longer.

This huge balance was built up by having more workers than retirees. Thus, since Social Security collects from current workers to pay current retirees, there was an imbalance in the amount of money that came in vs. what needed to be paid out. This money built up over the years until it grew to its current massive size.

Now, the tables are turning and there are projected to be more retirees than workers. This means that to make the promised Social Security payments the Administration will have to start taking withdrawals from the trust fund. By the year 2034, this trust fund will be been depleted unless something changes. At that point, benefit payments will be funded solely by payroll taxes from current workers and a few other small sources. In short, there won’t be enough money to make 100% of benefit payments.

But what if we could make the trust fund last longer by increasing the rate of return?

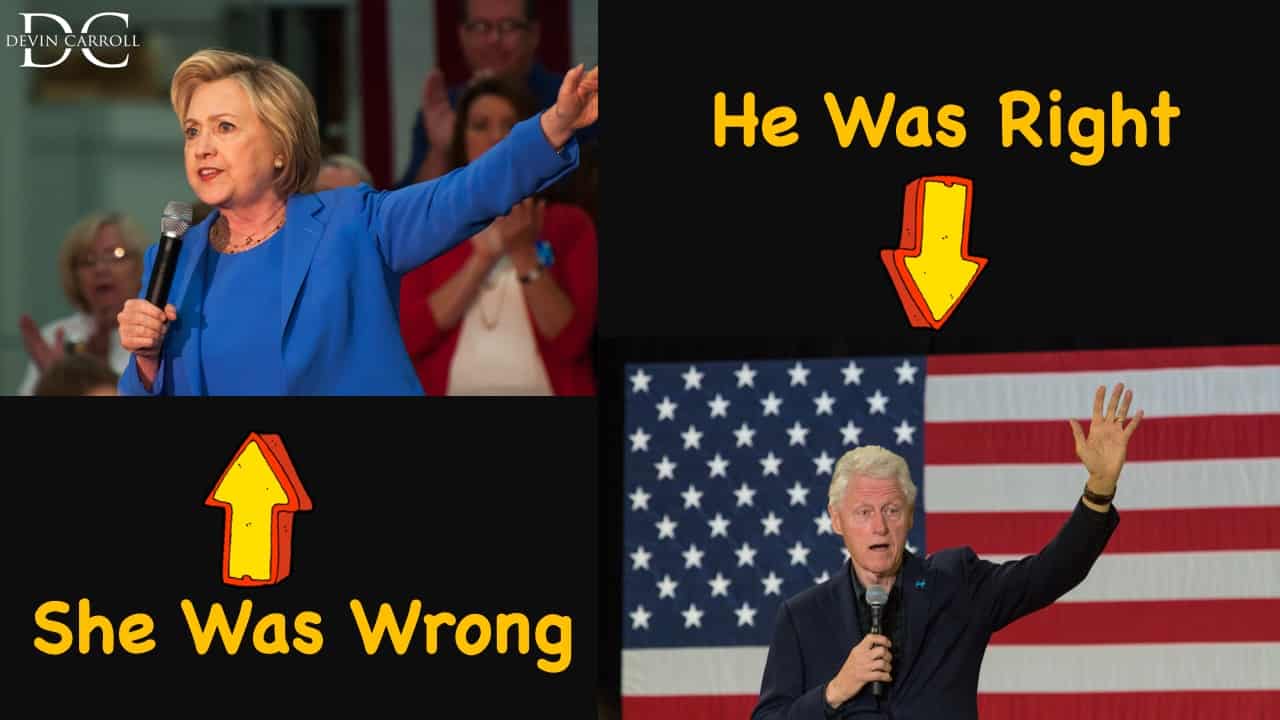

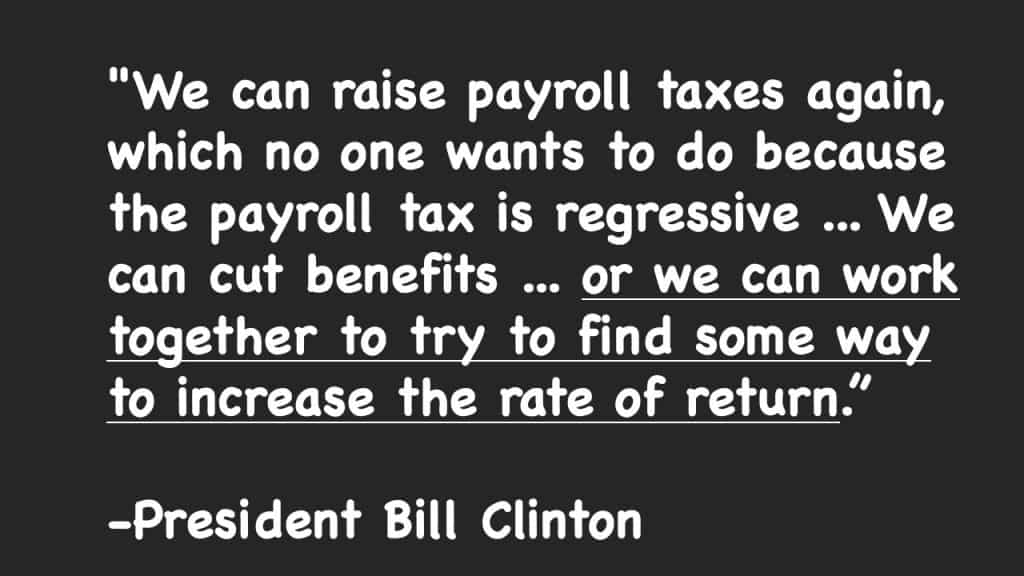

The Clinton’s Disagreement on Privatized Social Security

Let me give you some reasons this hasn’t happened yet. Back in 2016, when Senator Hillary Clinton was running for President, she loved to bash the “Republican” idea of investing Social Security. But ironically, it was her husband, President Bill Clinton, who actually proposed the privatized version of Social Security.

During the late 90’s he had a study group that suggested multiple fixes for Social Security. The one he really liked? Invest part of the Social Security trust fund. This made perfect sense! In multiple academic papers that followed it was found that the deficit would be closed completely by doing this.

How The Blue Dress Stopped The Plan To Privatize Social Security

But then something happened that stopped everything. Monica Lewinsky and her blue dress. At this point, President Clinton’s political survival forced him to align with his party and abandon several of his big objectives. Putting safeguards in place that would protect Social Security and Medicare for the long term was one that had to be pushed aside. The push to privatize Social Security died alongside his pride.

It’s too bad it went that way. In retrospective data, a paper from the Boston College’s Center for Retirement Research illustrated that this plan would have been effective, and we would not be in the place where we are today. In this same report, they say that investing the trust fund would still fix the issue. At the same time, reports from the SSA say that it wouldn’t have much of an impact this late in the game. So there’s some disagreement there about whether or not this will work at this point. After all, the time value of money needs TIME to work and we’re waiting until the 11th hour to get something done.

My Perspective

So let me tell you where I stand. I’m a conservative and find most of my views to align with our conservative legislators. However, no one gets a blank check for my approval.

Even though I have comments on my YouTube videos saying I’m a flaming liberal, and other comments on the same video saying I’m a crazy right winger I think that I have a responsibility to support the legislation that makes sense… even if it is from the ‘other’ party. But everything is framed as good or bad, liberal or conservative, black and white. We’ve gotten to a point where we feel bad for agreeing with a proposal from a party we don’t like and feel like we have to agree with everything our chosen party likes. There is an in-between here. And unless we find it, were going to have a disaster on our hands with Social Security.

If we keep waiting the only way to fix it will be drastic benefit cuts or tax increases. Increased taxes on the rich do not create ANYTHING! Instead, the often-unintended consequence is of targeting rich people with more taxes will be a BIGGER gap between the rich and the poor. This is because companies, who are more often than not owned by rich people, are not likely to take a reduction to their net profit or pay. Instead, the increased costs of higher taxes get passed on to employees through pay and benefit cuts.

It’s your retirement!

Before we go I want to thank you for taking the time to get informed. So many people just float into retirement hoping everything will work out. Sometimes it does, but sometimes a lack of planning can ruin what should be your best years. This is your retirement! Please continue to stay informed!

I’d recommend staying connected with my content so you won’t miss anything. In many cases I’ll publish my newest stuff on YouTube and then share it on my Facebook page. Then my content team does their magic and cleans it up into an article for those who enjoy reading. (Again…the article is shared on my Facebook page.)

Be sure to subscribe to my site so you won’t miss any of the new content coming out, plus you will receive the blueprint version of my book for free. Alternatively, you can just head over to Amazon and buy the full version. I can’t guarantee this, but I’m pretty sure you’ll get more value than the $12 it costs.

Not many of us want to spend too much time thinking or reading about taxes, but if you want to understand how Social Security is funded then we need to discuss the FICA tax. This payroll tax makes a big bite out of your paycheck and take-home pay but is responsible for funding the monthly Social Security benefits of millions of current retirees.

FICA stands for Federal Insurance Contributions Act, and the taxes this act imposed are used to fund federal benefit systems. Workers pay in through the tax now in order to receive their own benefits in the future.

In other words, FICA taxes are like your admission ticket to your eventual Social Security and Medicare benefits.

How the Taxes Withheld from Your Pay Break Down

Have you ever looked at the federal income tax brackets and wondered why the taxes taken out of your paycheck seem so much higher than the rates published by the IRS?

Seems awfully unfair, right? But the mismatch is due to the fact that the federal income tax rate — which is what we usually hear about when discussing taxes on a broad scale — is a relatively small part of the overall taxes most people pay.

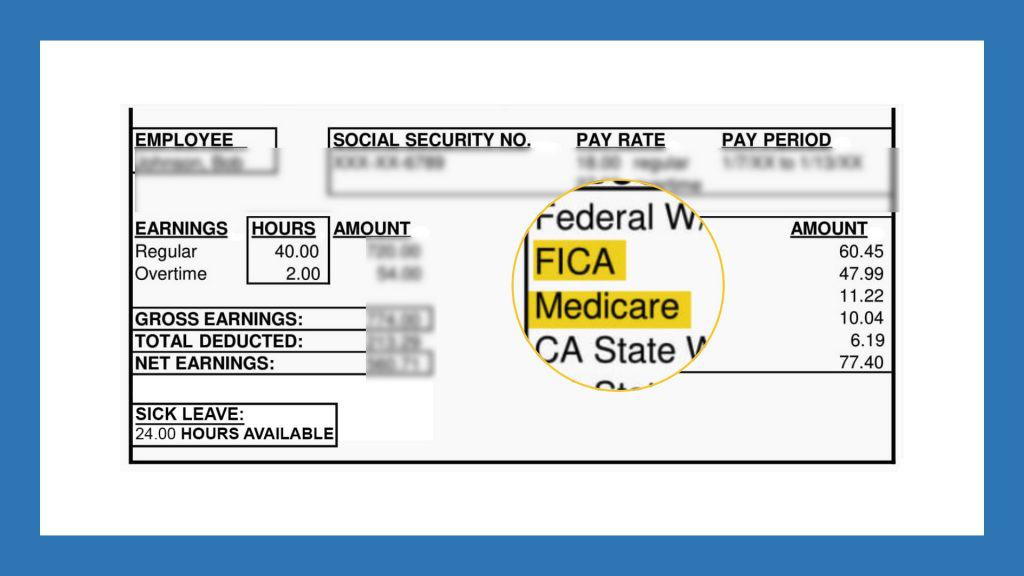

Take a close look at your paystub when you receive it next. You’ll see the deduction from gross pay due to federal withholding, and depending on your state, you may also see state withholding:

If you keep moving down your stub, you’re going to see a line for FICA taxes. Let’s take a closer look.

Understanding the FICA Tax

Again, the FICA tax is what you contribute to the federal government to pay current recipients of Social Security and Medicare benefits. Participation is required for most workers; the FICA tax is a mandatory payroll tax.

The tax collected for both programs could show up on your paystub as two separate line items, one for Social Security and another for Medicare.

Or the Social Security portion could be labeled “OASDI” for the Old Age Survivors Disability Income fund.

There are a few occupations groups that do not pay FICA, but 96% of all workers do pay it — so chances are good that includes you!

How Social Security Is Funded

I want you to understand more about what this tax is (since you’re obligated to pay it!) and how your money goes to fund Social Security and Medicare.

We know there are two components for the two programs. Here’s how the tax breaks down between the two:

The Social Security portion: This is also the largest part of Social Security. The total is 12.4%.

However, the tax rate is only applied to your first $132,900 in wages (for 2019; the limits do change yearly). In other words, you do not pay the 12.4% on your wages once you cross this limit.

Also, you actually only pay for half of the 12.4% you owe. Your employer is responsible for paying the other half.

The exception, of course, is if you’re self-employed. In that case, you’re on the hook for paying the full amount of FICA tax.

The Medicare portion: This is a total of 2.9% in taxes. It’s also split 50/50 between you as the employee and your employer (but again, self-employed folks are responsible for paying the entire amount themselves).

This means that in total, 15.3% of your wages are paid in to the Social Security and Medicare programs in order to fund the benefits going out to current recipients.

I hope that next time you look at your paycheck you’ll have a better understanding of how Social Security is funded.

Need More Info? Here’s Where to Go

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group.

It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the 330,000+ subscribers on my YouTube channel! For us visual learners, this is where I break down the complex rules and help you figure out how to use them to your advantage.

And one last thing that you don’t want to miss: Be sure to get your FREE copy of mySocial Security Cheat Sheet. This handy guide takes all of the most important rules from the massive Social Security website and condenses it all down to just one page.