It’s one of the most popular questions asked about claiming benefits for your retirement: What’s the right age to collect Social Security? Should you file early — or late?

This is not an easy decision to make, or one to take lightly. No matter what your financial situation, you’ve likely wondered about the best strategy for you.

So today, take a look at the 10 factors you need to consider when you’re thinking about filing for your benefits.

Who’s Right: People Who Wait, or People Who File for Benefits ASAP?

Many people who work in finance take a hard stance on the best age to retire and collect Social Security. More often than not, they say it’s best to delay taking Social Security for as long as possible.

But plenty of other people persist in saying you need to get your benefits as soon as you can. So who is right?

The truth is that neither of these are always correct. The decision about when to take Social Security is highly personal, and the right choice for you needs to take multiple individual factors into account.

Don’t let the simplicity of the Social Security statement fool you — if you care about your retirement, this decision must be made with careful thought and analysis. My goal here is not to tell you that a certain age is best and another age doesn’t work.

Instead, I want to provide you with the right information so you feel empowered to make the best decision for you. But before we jump into the factors to consider in determining the right age to file for Social Security, let’s make sure we understand some of the basic facts we’re working with.

How Reductions and Increases in Social Security Benefits Work

The first thing you need to understand to make a decision for yourself is at what age do you obtain the Social Security Administration’s status for full retirement age. It’s pretty simple to find the answer.

For those born between 1943 and 1954, full retirement age is 66. If you were born between 1955 and 1959, add two months for every year after 1954 to get to your full retirement age. And if you were born in 1960 or later, your full retirement age is 67.

Full retirement age means the point at which you will receive the full amount of your Social Security benefit. For the purposes of the rest of this article, we’ll assume “67” when talking about full retirement age (but know yours might be slightly different if you were born before 1960).

Your benefit will be reduced or increased if you file at an age other 67. If you file after full retirement age, your benefit is increased up to 124% (which is 8% per year), up until age 70. If you file early it will be reduced by an average of 6% for every year before 67 that you filed.

We can use an example with dollar amounts to make this more clear. Say your full benefit at 67 is $2,000. That benefit will increase up to $2,480 if you wait until age 70. If you file before your full retirement age, however, your benefit could be reduced down to as little as $1,400.

Not including cost of living adjustments, that’s a $1,000 difference per month. That’s a big deal!

It’s easy to see why the financial community likes to make blanket statements suggesting that everyone should delay as long as possible. But despite the overwhelming software tools and online content suggesting that most should wait, that’s not what people are doing.

A Break-Even Analysis Might Not Be the Best Way to Evaluate the Right Age to File for Social Security

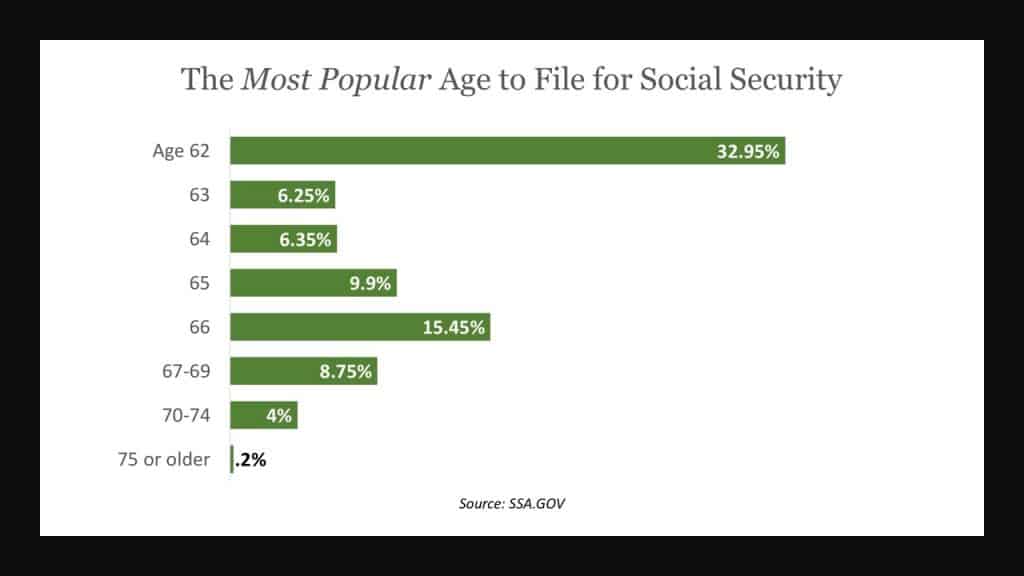

The filing age data put out by the Social Security Administration shows that one-third of people simply file at the earliest age possible.

Does that mean about 33% of us are making bad financial moves? To be honest with you, I do feel people often make the decision to file without doing a lot of thoughtful analysis first…

…but broadly saying, “filing early is wrong” is shortsighted. One thing I know for sure is that there is a lack of resources to help individuals make this important decision. This leaves individuals to make the most intuitive choice in front of them, and that’s generally centered around the concept of a break-even analysis.

These type of analysis tells you how long you’d have to live to for benefit payments to catch up to other filing ages. Let me give you an example of this.

Assuming your full retirement age benefit is $2,000, you could claim your benefits at age 62 and start receiving $1,400. If we go with the life expectancy assumptions from the Social Security Administration and say you’ll live to an average 85 years old, then filing at 62 gives you a total cumulative benefit of around $515,000 when you include cost of living adjustments.

That also means if you wait to file until age 67 and receive your full $2,000, your total benefit payout could be nearly 100,000 dollars higher! But you have to live until at least 76 before you break even and get the same amount as you would if you filed at 62.

When Some folks look at the life expectancy of their family members or coworkers and decide there’s no way they’ll ever hit that break even age of 76 and so…they file early. I think this is a mistake!

The question the breakeven analysis answers is, “What if I die early?” But this question is such a small part of the filing decision. It only considers your benefit amount and completely ignores the optimization of spousal and survivor benefits and the role your benefit amount may play in their lifetime.

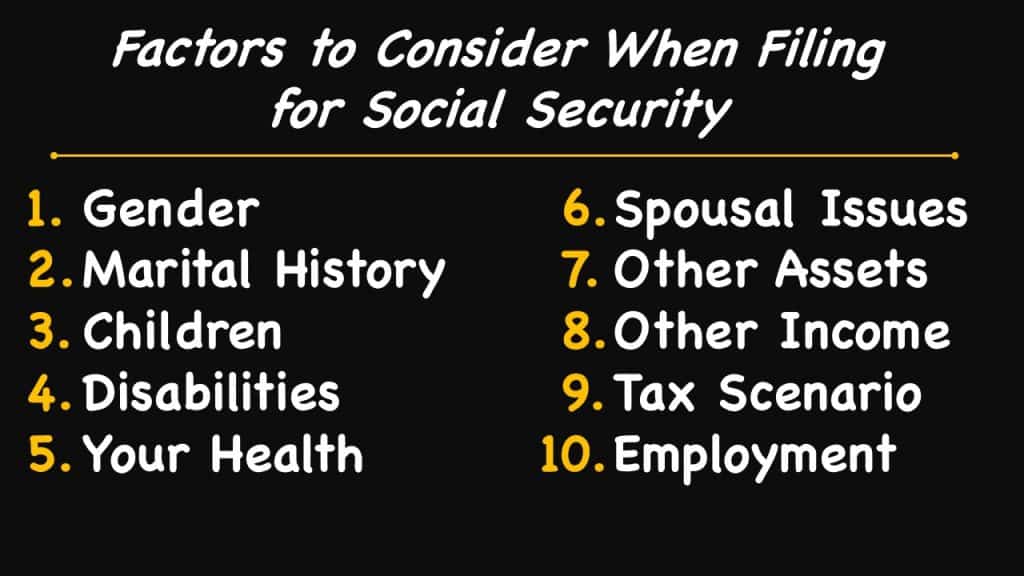

The 10 Factors to Consider to Determine When You Should File for Social Security Benefits

When you’re making the decision about when to file (or helping someone else make this choice), there are at least 10 factors that you need to consider to get to the right answer. All of these factors are very important to account for — but there can be disastrous consequences for ignoring the last two in particular.

Factor 1: What’s Your Gender?

Your decision about when to collect Social Security begins with your gender. The decision to delay or not is more important for women than it is for men. There are two reasons for this:

- Women live longer than men.

- On average, Social Security makes up a greater percentage of a woman’s retirement income (47%).

The decision to file later and get a higher benefit is possibly more important for a woman to consider. According to data from the Social Security Administration, men usually have a higher benefit amount than the women they’re married to.

If that’s your case, you need to exercise caution filing based on the impact your benefit will have to your wife (since she will likely outlive you and need the income even more than when you were living).

Factor 2: What Does Your Marital History Look Like?

Next, consider your marital history. If you had prior marriages, figure out if you are eligible for benefits from any of those past marriages that could boost your own benefit.

For example, if you have an eligible deceased spouse or ex-spouse, it could make sense to file for a survivors’ benefit as early as age 60 and switch to your own benefit later.

If you have an ex-spouse who is still living you need to figure out if you are entitled to a higher benefit from the spousal provisions

Factor 3: Do You Have Minor or Disabled Children?

If so, they could eligible for benefits once you file. Grandchildren could be eligible, as well, if both biological parents are deceased or disabled or if you have adopted them.

This is one of the cases where it generally makes perfect sense to file as early as possible. This is because a rule that states that before benefits can be paid to anyone off of your work history, you have to be receiving benefits.

When combined with your benefit, the benefits to children and your eligible spouse can be up to 180% of your full retirement age benefit. So if you have children at home that meet the criteria, there’s an obvious reason to consider filing early.

Factor 4: Are you Disabled?

If you are disabled, or think you may meet the criteria, filing for Social Security disability at age 62 could make a lot more sense than filing for retirement benefits. This is because your disability payment is the same as your full retirement age benefit.

Filing for disability will also enable your eligible beneficiaries to receive a benefit. If you file for disability first and then file for retirement benefits, just remember that the Social Security Administration will make up the difference if you are awarded disability benefits.

I’ve seen more than one individual who clearly met the criteria for disability benefits, but waited until full retirement age to file for retirement benefits so they could get their full amount. What a mistake!

Factor 5: How’s Your Health?

If you have a condition that could lead to a shortened life expectancy, that should be part of the decision process about the right age to file for Social Security.

If you’re single, it may mean that you file for benefits as early as possible in order to get all the payments you can. This is one time when the break-even chart really makes sense. This was part of the reason that I recommended to my own mom that she should file early.

On the other hand, if you’re married, you’ll have to balance the impact of leaving your spouse a smaller benefit (if you file early) or a larger benefit (if you file later).

Factor 6: How About the Health of Your Spouse?

In a broad sense, the age, health and individual benefit of your spouse should probably be considered separately, but they are so interwoven that I’ll cover them at one time.

First, let’s assume your spouse is the lower earner. If they’re also younger than you, they’ll probably outlive you. Your retirement benefit will likely become their survivors’ benefit when you die.

For this reason it’s important to consider how your filing timeline will affect the eventual survivors’ benefits your spouse could receive. Delaying your benefit would increase the survivors’ benefit they’d receive for those extra years after you’re gone.

But if your spouse is in poor health and is unlikely to outlive you, delaying your benefit strictly for the purpose of increasing their survivors’ benefit doesn’t make sense.

Again, assuming that your spouse is the lower earner, their benefit may not get to the maximum potential benefit until the spousal benefit portion kicks in. So If your spouse’s benefit is less than one half of yours, it could make sense to file just to open up your work record to pay a spousal benefit.

For example, if your benefit is $2,000 and your spouse’s benefit from their work is $400, they’ll be entitled to the $400 first, and then up to a $600 spousal benefit for a total of $1,000 at full retirement age.

The catch is, you have to file for your benefit first for the extra $600 to be paid. Furthermore, you have to remember that a spousal benefit does not increase beyond full retirement age. If your lower-earning spouse is older than you, waiting to file may be increasing your own benefit — but not necessarily your lower-earning spouse’s benefit.

Factor 7: Don’t Forget Your Spouse’s Earnings in Relation to Yours

If you have a spouse with very little to no earnings, it could make sense to file early for the sole purpose of opening up the spousal benefit. A strategy like this is highly dependent on multiple factors, but when you compare the total amount of benefits you both could receive, this strategy could make more sense than you delaying your own.

Remember that since the spousal benefit portion can’t be paid until you file, delaying your benefit also delays your spouse’s benefit.

Here’s another example: if your benefit at full retirement age is 67, your spouse would also be entitled to a benefit at their full retirement age of $1,000. So if your spouse is 3 years older than you, and you wait until you’re 67 to file, you’d be waiting five years to get an extra $600 on your check but meanwhile you’re leaving behind a $1,000 spousal benefit for every month you delay filing.

Yes, your benefit would be higher once you file, but your spouse’s benefit would not be. The total benefit paid with you filing at 62 versus 67 would eventually catch up, but you’d be 84 before getting to the break-even point.

If your spouse is the higher earner, then their benefit will be higher than yours. There’s nothing you can do in your filing strategy to increase their current benefit or future survivors’ benefit.

Instead of evaluating their health or life expectancy in this case, consider your own along with the last few factors we’ll discuss. (One exception may be if your spouse is the higher earner and in poor health, especially with a condition that has a high likelihood of ending in premature death; consider filing early because once they die, your own benefit will stop and you’ll start to collect your deceased spouse’s benefit).

Factor 8: What to Keep in Mind If You Already Have a Lot of Assets

If you have ample assets and other income sources, the relative importance of a filing decision is not the same as it is for someone with no other assets or income who will rely solely on Social Security.

Social Security benefits make up 38% of the average American’s retirement income. That’s a pretty high percentage. But this number includes those who have so much income they don’t even notice these deposits and people who depend on Social Security for 100% of their retirement income.

You’ll have more options to be flexible with your filing decision if you have ample retirement savings and other sources of income. So if this describes you, then you need to think about the next factor to determine the best age to file.

Factor 9: Your Tax Scenario

Somewhere between 0% and 85% of your Social Security benefits will be added to your taxable income. It could make sense to delay filing to reduce these taxes in retirement.

This won’t work for everyone, but it could make a big difference for those in the right income bracket.

In order to determine how much of your benefit will be taxable, you first have to calculate “combined income.” This is a measurement of income used specifically for this purpose.

Combined income can be roughly calculated as your total income from taxable sources, plus any tax-exempt interest (such as interest from tax-free bonds), plus any excluded foreign income, plus 50% of your Social Security benefits.

Assume that you need $4,000 per month in income. Your Social Security benefit at your full retirement age is $2,000. This means that you’ll need $2,000 from other sources such as retirement accounts.

What if you took the entire $4,000 you needed from your retirement accounts until you reach age 70? Then, you could switch on your Social Security benefit which would be $2,480. Now you only need $1,620 in monthly distributions from your retirement accounts.

Since only half of your Social Security is counted in the provisional income calculation, the overall provisional income should be reduced. That results in less of your benefit being taxed.

All this being said, your tax advisor is the best resource for recommendations on a tax plan for retirement and Social Security, so be sure to touch base with them and talk through the specifics of your situation before making a final decision based on tax benefits.

Factor 10: Your Employment Status

Finally, we have to consider your employment status. The lure of eligibility at 62 is strong. But if you plan to continue working, you need to be aware of the Social Security income limit.

I’ve seen more than one individual who filed for benefits without being aware of this income limit — and later got caught with an overpayment notice and a suspension of benefits.

The Social Security income limit is the amount of money you can earn before your earnings impact if you’ll receive Social Security benefit. If your income exceeds the Social Security income limit your Social Security benefits will be stopped.

This limit increases every year. In 2019, the limit is $17,640. It’s important to note that the earnings limit does not apply if you file for benefits at your full retirement age or beyond. These limits only apply to those who begin taking Social Security benefits before reaching full retirement age.

In this complex conversation on Social Security and the best age to file for benefits, one thing stands out very clearly: there’s no one-size-fits-all answer or rule of thumb for Social Security filing.

Not even this article covered all the factors you need to know in order to make a great decision — but I hope it did give you some great food for thought. Keep digging in and continue learning how your filing strategy will impact you in retirement.

You’re making the right moves by reading articles like these, but don’t stop here! Continue to do your research and talk to your own advisors. Most importantly, continue to educate yourself.

Questions?

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

Also…if you haven’t already, you should join the 100,000+ subscribers on my YouTube channel!

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

[…] the filing decision. But it’s just one step in the process, as this is a complex situation with more data points to consider. Break even age is an important consideration, but that information alone cannot be the deciding […]

I’m 69 , I have reached my full benefits age. I hear you say I can make as much income as I wish without reducing my benefits. Am I correct?

What about starting at 62, but investing that money vs. just spending it. Now it seems that has the potential to push back the “break-even age” by a little or even a lot. Then factor in the fact that the Soc Sec Chest has been tapped and exploited and now in potential of causing drastic cuts in SS or even SS going away. It may be smarter to get what you can, as soon as you can.

Very informative article. Determining the correct age to collect social security benefits is important to maximise your benefits. Social Security benefits provides approx 37% of the average retirement income. Getting this information can help you increase your monthly instalments.