Whenever I’m asked about how Social Security survivor benefits work, I have a simple answer:

At death of the first spouse, surviving spouses receive the higher of:

Their own monthly benefit, or

The monthly benefit of the deceased.

That’s the clean and straightforward answer, but it’s not quite that simple. Although Social Security survivor benefits really are pretty simple, every family is different. Unique situations and variables can introduce some complexity.

Have you ever tried to use a power of attorney for Social Security purposes? If you haven’t, save yourself the trouble. The Social Security Administration will not accept it.

After multiple clients experienced frustration at the Social Security office, I reached out to John Ross, an elder law attorney and co-host of our podcast (Big Picture Retirement) for an explanation and guidance on why powers of attorney (or POAs) don’t fly with the Administration.

Here’s what he told me.

There’s No Such Thing as a Social Security Power of Attorney

John Ross explained that there is no “Social Security Power of Attorney.” Powers of attorney are creations of state law and vary wildly from state to state, Ross added.

“Since the federal agencies like the SSA do not want to have to separately review POAs based on both the facts and circumstances of their creation and the various state laws that may be applicable, these agencies have taken the position that they will not accept a POA under any circumstances,” said Ross.

He explained that the Social Security Administration developed federal regulations related to incapacitated beneficiaries of federal programs and established criteria under who the agency will deal with. “Since federal law trumps state law,” he added, “there is nothing an agent under a power of attorney can do to alter this structure.”

How to Help Someone with Their Social Security When POAs Don’t Work

That’s reason for concern if you’re a friend or family member of someone who struggles to manage their Social Security 100% on their own. How do you help someone with their Social Security issues if the SSA won’t accept a POA?

Essentially, anyone who wants to assist someone receiving Social Security benefits who needs help will have two options:

Obtain a court appointment as the Social Security beneficiary’s guardian.

Apply to the SSA to become the representative payee for the Social Security benefits.

Let’s look at each option in more detail:

Option #1: Obtain a Court Appointment as Guardian

Warning: This is not your best option.

One way to approach the Social Security Administration is with a court-appointed guardianship. This is an expensive, time-consuming process — but agencies such as the SSA are required to deal with a beneficiary’s court appointed guardian.

First, you’ll have to hire an attorney to file a petition for a guardianship hearing. Depending on your state, this process could take a long time.

The court will have to examine expert findings, such as doctor’s statements, declare that the individual is incompetent, and appoint a guardian. The court then transfers the responsibility for managing all living arrangements, and medical decisions to the guardian.

Then, in many cases, the court will require the guardian to provide regular, detailed financial accounting reports to the court. In most cases, becoming a court-appointed guardian is a complicated, expensive solution.

There’s a much easier way to help someone who may need it:

Option #2: Become a Representative Payee

The second option is applying to become a representative payee. This program is specific to the Social Security Administration, and it allows an individual to manage the Social Security payments of a beneficiary who is incapable of managing his or her own Social Security.

Thankfully, this option is nowhere near as burdensome as applying for guardianship. This is the best solution! It is faster, free, and doesn’t come with all of the encumbrances of a court appointment.

The steps to becoming a representative payee is as follows:

Fill out (or least review) SSA 11 Request to be Selected as Payee form.

Here are the instructions that the Social Security gives to their technicians in deciding who the payee will be:

“Each payee application must be reviewed and evaluated individually to determine the best payee. All applicants must be carefully screened and considered before a selection is made to ensure that the beneficiary’s best interest is served. In determining the best payee choice, consider all factors, including the applicant’s relationship to the beneficiary, the applicant’s interest in the beneficiary’s well being and whether or not the applicant has custody of the beneficiary.”

In the past, a representative payee could not be appointed until the point of need. But now, an individual can designate up to three people who could serve as a representative payee if the need ever arises.

This designation can be updated or withdrawn at any time and the SSA will send a notice each year listing the advance designees for review.

The good news is that it’s really easy to get this done. On the mySSA account, simply navigate to the link

Understanding Your Responsibility as a Representative Payee Report

The SSA requires that a representative payee file an annual accounting called the Representative Payee Report. This report details what you, as the representative payee, have done with the beneficiary’s funds during the previous year.

If you have kept accurate records of the beneficiary’s funds over the course of the year, the report will be very easy to fill out. Commingling funds, or not keeping accurate records of expenditures, can lead to an incredible headache when it comes time to file the report. And not filing the report at all could lead to your removal as representative payee.

So who can become a representative payee? The Administration maintains a list of preferred individuals. This list is in their preferred order of representative selection.

Payee Preference List For Adults

When you determine that the beneficiary needs a representative payee, select the best payee available from this list of preferred applicants:

A spouse, parent or other relative with custody or who shows strong concern;

A legal guardian/conservator with custody or who shows strong concern;

A friend with custody;

A public or nonprofit agency or institution;

A Federal or State institution;

A statutory guardian

A voluntary conservator

A private, for-profit institution with custody and is licensed under State law;

A friend without custody, but who shows strong concern for the beneficiary’s well-being, including persons with power of attorney;

Anyone not listed above who is qualified and able to act as payee, and who is willing to do so;

An organization that charges a fee for its service.

Payee Preference Lists For Minor Children

When the beneficiary is a minor child, select the best payee available from this list of preferred applicants:

A natural or adoptive parent with custody;

A legal guardian;

A natural or adoptive parent without custody, but who shows strong concern;

A relative or stepparent with custody;

A close friend with custody and provides for the child’s needs;

A relative or close friend without custody, but who shows strong concern;

An authorized social agency or custodial institution; or

Anyone not listed above who shows strong concern for the child, is qualified, and able to act as payee, and who is willing to do so.

When you’re dealing with a relative or friend who can no longer manage their own financial matters, everyday activities are complicated. It would be really nice if the Social Security Administration would just accept a power of attorney. But since they won’t, being designated a Social Security Representative Payee is the simplest way to help with Social Security issues

That being said, if you’re dealing with Social Security benefits as a representative payee and feel overwhelmed, I know how difficult and isolated it can make you feel.

It can seem that no one understands your predicament and can’t give you the answer you need. What may help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the nearly 400,000+ subscribers on my YouTube channel. For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing that you don’t want to miss: Be sure to get your FREE copy of mySocial Security Cheat Sheet. This handy guide takes all of the most important rules from the massive Social Security website and condenses it all down to just one page.

Social Security benefits for children are a big deal. In October of 2022, there were more than 3.8 million children receiving Social Security benefits because one or both of their parents are disabled, retired, or deceased. These benefit payments to children total more than $2.6 billion every month.

Sadly, many children don’t get the benefits for which they are eligible. Most people don’t know about the qualifications and rules for this special benefit, so they don’t know to apply for the children in their lives.

A few years ago I saw a startling headline. It read, “Obama Administration Finalizes Social Security Gun Ban.” The sub-headline read, “On Monday the Obama administration finalized a Social Security gun ban that could prevent ‘tens of thousands’ of law-abiding elderly citizens from purchasing guns for self-defense.”

It didn’t take much browsing to find more headlines that were equally disturbing:

Obama’s Secret Plan To Block Seniors On Social Security From Owning Guns on Breitbart

SPREAD THIS: Obama Makes Huge Move to BAN Social Security Recipients From Owning Guns on Conservative Tribune

Obama to Ban Thousands of Senior Citizens from Owning Firearms on GunOwners.org

Since then I’ve seen headlines like these pop back up anytime there is a mass shooting.

With provocative headlines like these, it’s no wonder that I get lots of comments from worried retirees. Will seniors really be forced to surrender their firearms before they can receive Social Security payments?

As with many sensational headlines, this headline contains enough truth to keep it from being a flat out lie. However, that’s not the same as being accurate. Not even close.

Note: The Social Security earnings limit changes each year. The most current version of this article uses numbers for 2023.

At one of my first speaking engagements, I heard a great story from one of the attendees. Her experience provides us with one of the best examples I’ve ever heard of how much the Social Security income limit can catch you by surprise.

A few years earlier, she’d been at her bridge club when the topic turned to Social Security. As she and the other card players chatted about the best way to leverage Social Security Benefits, the consensus around the table seemed to be that filing at 62 was the smartest thing to do.

This lady, trusting the advice of some of her closest friends, did just that: She filed for benefits as soon as she turned 62.

She then told me she’d always wanted to buy a brand-new Toyota Camry. She figured that, once she started receiving Social Security income, it would be the perfect time to buy the car. She was still working, which meant her Social Security check would be extra income.

As she told the story to me, she bought the car and took out a car loan to do it. She planned to repay the loan using some of the income she expected to receive from her Social Security benefits since she filed for them.

Imagine her surprise, then, when a nasty letter from Social Security Administration showed up in her mailbox. The letter claimed she had been paid benefits that she was not eligible for!

The Social Security Administration not only asked her to pay the benefits back, but also informed her that future benefits would be suspended due to her income.

Now she had a new car and a car loan, without the Social Security benefits she planned to use to handle that monthly payment. What happened here?

Something that surprises more than just the poor Camry owner who approached me that day: the Social Security income limit.

What Is the Social Security Income Limit?

The earnings limit is also known as the income limit, or the earnings test. The official term is “earnings test,” but income limit and earnings limit are the terms that you’ll hear most often.

For our purposes, know that all these terms mean the same thing — and there are four quick facts about the Social Security income limit that you should know before we jump all the way into explaining the test or limit:

Be aware that we are talking about Social Security income limits for retirement benefits, not disability or SSI.

The earnings limit does not apply if you file for benefits at your full retirement age or beyond. These limits only apply to those who begin taking Social Security benefits before reaching full retirement age.

Not long ago, a viewer on my YouTube channel asked me to give her a good reason why we have the Social Security earnings limit. The comments that followed showed how many viewers shared the belief that the earnings limit is unfair and should be eliminated.

In my response, I explained that the rationale behind the entire program of Social Security was to create a safety net. The original intent of the Social security program was not to supplement retirement income, but to keep the elderly (most of whom lost any potential long-term wealth in the Great Depression) out of poverty.

I also added that today’s earnings limit is relatively generous compared to where the Social Security earnings limit began. The original Economic Security Bill (which is what the Social Security Act was originally called) President Roosevelt sent to Congress featured a very restrictive earnings limit.

That bill stated, “No person shall receive such old-age annuity unless . . . He is not employed by another in a gainful occupation.”

Whoa! This means that if you had even a single dollar in wages from a job, you could not collect a Social Security benefit at all.

Thankfully, the system we have in place today allows for individuals to have some earnings from work while they are receiving a Social Security benefit.

However, it’s very important to stay informed on the dollar amount of this limit because it changes every year.

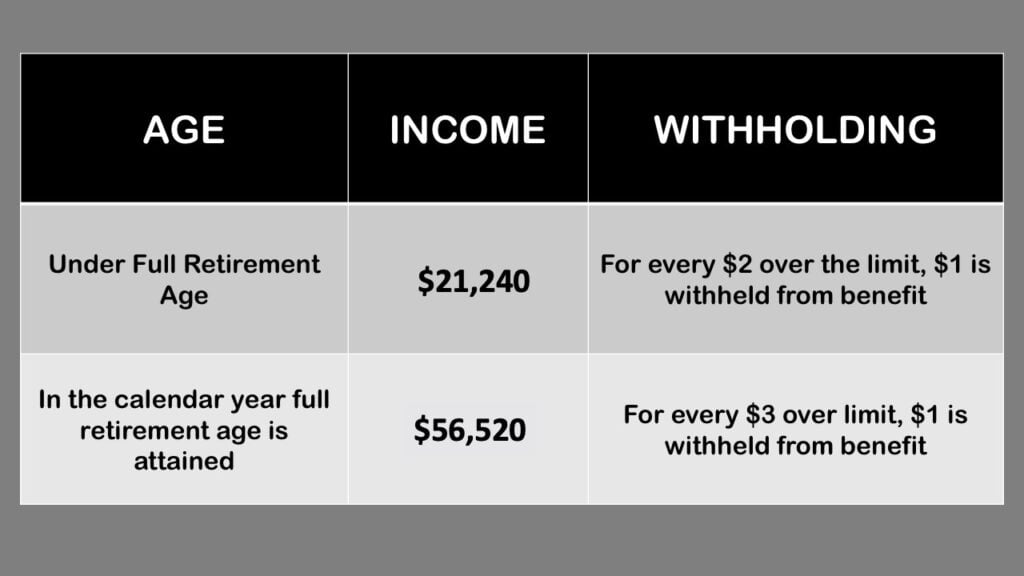

For 2023, the Social Security earnings limit is $21,240. For every $2 you exceed that limit, $1 will be withheld in benefits.

The exception to this dollar limit is in the calendar year that you will reach full retirement age. For the period between January 1 and the month you attain full retirement age, the income limit increases to $56,520 (for 2023) without a reduction in benefits. For every $3 you exceed that limit, $1 will be withheld in benefits.

This means that if you have a birthday in July, you’ll have a 6 month period with an increased income limit before it’s dropped completely at your full retirement age. This increased limit and decreased withholding amount allow many individuals to retire at the beginning of the calendar year in which they attain full retirement age, rather than waiting until their actual birthdays.

Again, once you reach full retirement age, there is no reduction in benefits regardless of your income level.

A Real-Life Example of the Social Security Income Limit in Action

To put these numbers into context, let’s look at an example of how this might work in a real-life scenario:

Rosie is 64 years old. She started taking Social Security benefits as soon as she turned 62. Based on her birth year, her full retirement age is 66.

Right now, Rosie is eligible for $20,000 in Social Security benefits per year. She also worked during the year and made $31,240 in wages.

The question we want to understand is, how much was Rosie’s benefit reduced by working while on Social Security? To answer that, we first need to calculate how much Rosie was over the Social Security earnings limit for her age.

In 2022, Rosie filed for Social Security; she received her first check in January of 2023. Throughout the year she received $1,667 in benefits every month. Without knowing the rules, she also worked and earned $31,240 in wages.

With a Social Security earnings limit of $21,240, she was over by $10,000:

$31,240 Total Wages – the Social Security Income Limit of $21,240 = $10,000 Income in excess Of limit

Because this is a full calendar year during which Rosie is receiving benefits but is not yet full retirement age, the benefits reduction amount is $1 reduction for every $2 in excess wages. Since she was over the limit by $10,000, her benefits will be reduced by $5,000.

The benefit reduction calculation would appear as follows:

$10,000 Income in Excess of Limit x 50% ($1 reduction for every $2 over limit) equals a $5,000 Benefit Reduction

With a $5,000 benefits reduction for exceeding the income limits, Rosie’s $20,000 yearly Social Security benefit will be reduced to a $15,000 benefit for the year. In the following year, she would attain her full retirement age and after her birthday, the limit would no longer apply.

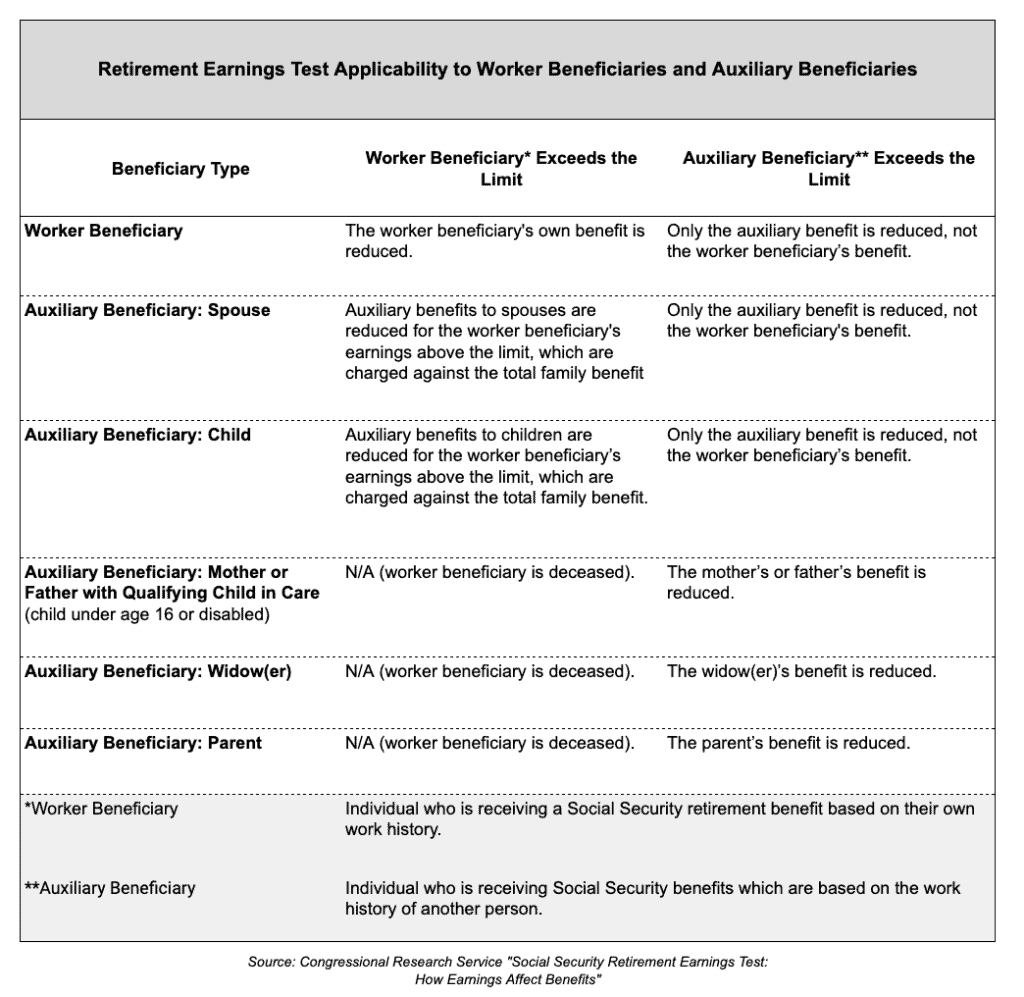

How Does The Income Limit Affect Spousal, Survivor, or Children’s Benefits?

There are millions of individuals who receive benefits as an “auxiliary” of a retired or disabled worker. These auxiliary beneficiaries are also subject to the same earnings test.

See the chart below for more detail on how the limits are applied to each type of benefit.

Special Monthly Income Limit Rule for the First Year (or, Your Grace Year)

Many people who retire mid-year have already earned more income than the limit allows. This is why there is a special rule where the earnings limit switches from an annual limit to a monthly limit. (These monthly limits are 1/12 of the annual limit.)

This rule allows you to receive a check for any month you are considered “retired” by the SSA even if you have already exceeded the annual earnings limit.

That sounds straightforward enough — but the interpretation of “retired” as defined by the SSA can cause some confusion. Here’s what they mean by this term:

You are retired if your monthly earnings are 1/12 of the annual limit ($1,770 for 2023) or less and you did not perform substantial services in self-employment.

Essentially, you are considered retired unless you make more than the income limit. The rule for the year you reach full retirement age also applies when working with the monthly limit. In this calendar year for 2023, the limit is $4,710 (1/12 of $56,520).

It’s very important to remember that in the year following this first year, the monthly limit is no longer used and the earnings limit is based solely on your annual earnings limit.

How the Earnings Limit Is Applied

The most confusing part of the benefit reduction due to income is how it’s reflected in your monthly benefits deposits. Instead of taking out a little bit every month, the SSA will withhold several months of benefits at a time.

If you predict in advance that you will have excess earnings and report this to the Social Security Administration, they may take a few months of benefits before you actually earn the anticipated excess earnings.

For example, if your Social Security payment is $1,667 per month, and you expect to receive $31,240 in wages from your job, the Administration would calculate that you’ll be over your earnings limit by $10,000 and thus $5,000 in benefits should be withheld. So, they would withhold your benefit payment from January to March. In April, your checks would resume.

If you don’t report excess income before you earn it, then you have to report this information after the fact. You can do this when you file your income tax return, but the preferred method is to be proactive and call your local Social Security Administration office.

If you wait for the Social Security Administration to learn of your excess earnings via your tax return, there could be a significant gap between the time you earn the excess income and the time that they withhold your benefits. In most cases, it’s better to report the excess earnings quickly so the benefits reduction occurs closer to the time you actually earn that extra income.

Regardless of whether your benefits are withheld in advance or in arrears, benefits withholding can make budgeting and planning difficult, especially if you don’t understand the system. You may need to create a separate savings account to set some of those earnings aside to compensate for benefits withholding that will occur in the future.

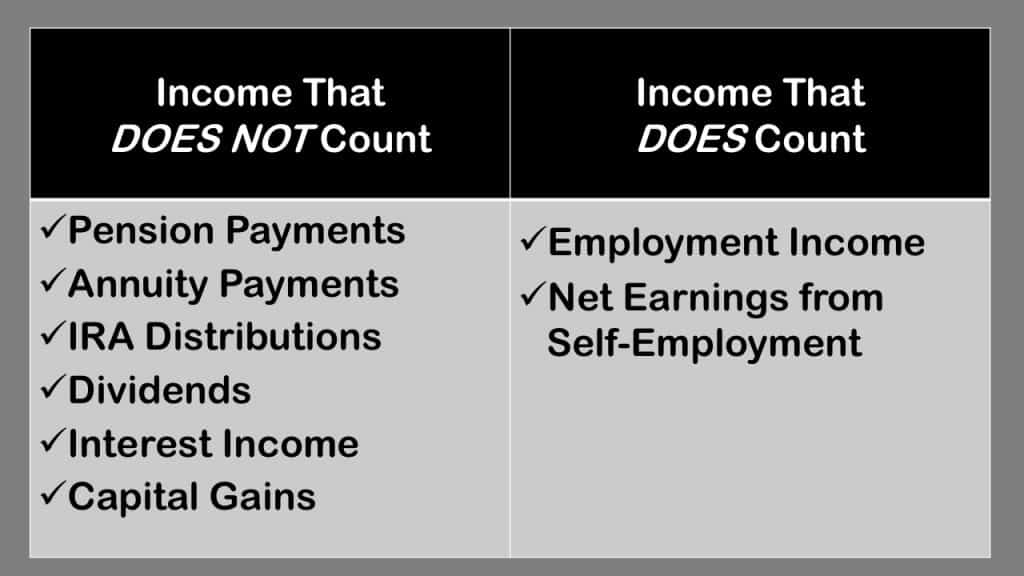

What Kind of Income Counts as Earnings?

The Social Security income limit applies only to gross wages and net earnings from self-employment. All other income is exempt, including pensions, interest, annuities, IRA distributions, and capital gains.

The term “wages” refers to your gross wages. This is the money that you earn before any deductions, including taxes, retirement contributions, or other deductions.

What to Do If Your Benefits Are Already Being Withheld

If you’re subject to the Social Security earnings limit, don’t wait for the SSA to start reducing the benefit you receive. Instead, I’d recommend voluntarily suspending benefits.

If you wait for the Social Security Administration to discover that you’ve earned too much working while receiving benefits, your risk of an overpayment notice is higher.

Either way, you aren’t missing payments that you’ll never get back. Your benefit amount will be recalculated at your full retirement age (or when you stop working) to reflect the months that benefits were withheld.

The best way to avoid the earnings limitation is to wait until full retirement age to file for benefits. If you can’t wait, make sure you have a clear understanding of how working impacts your Social Security benefits.

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the nearly 400,000 subscribers on my YouTube channel! For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing that you don’t want to miss: Be sure to get your FREE copy of my Social Security Cheat Sheet. This handy guide takes all of the most important rules from the massive Social Security website and condenses it all down to just one page.

Social Security credits are the building blocks that the Social Security Administration relies on to determine whether or not you qualify for one of its programs. In 2021, you receive one credit for each $1,470 of earnings, up to the maximum of four credits per year. The amount of earnings needed to earn a credit increases annually as average wage levels increase.

One stipulation is that your earnings must be subject to Social Security tax to count for a credit. In exchange for this tax, you are eligible for the following important benefits:

Social Security Retirement Benefits

Social Security Disability Benefits

Social Security Survivor Benefits

Medicare

Each of these programs have different requirements for the number of credits to gain eligibility. Here’s a quick look at the eligibility for each.

Louisiana state public employees face special challenges when it comes to figuring out their retirement benefits. Most Louisiana state public employees, who may be covered by LASERS, LSERS, TRSL, or other public employee retirement plans, don’t pay into the Social Security system. This means their ability to receive Social Security benefits is different from typical employment where the employee pays Social Security taxes. The situation gets more confusing when an eligible employee has some Social Security covered employment and some non-Social Security covered employment. Even worse, many people don’t learn about the rules until they reach retirement age, and they may have made decisions based on faulty information. Thankfully, the rules aren’t too complicated, and I’m here to help you decipher them. There are two rules that apply here: the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO). These links give more detailed information about each rule, but here are summaries:

How confident are you that your Social Security earnings record is accurate?

Unless you’ve checked it recently, you shouldn’t be too sure.

Mistakes in an individual’s Social Security earnings record are actually much more common than most people think. In tax year 2012 alone, the Social Security Administration reported $71 billion in wages that could not be matched to an individuals earnings record! The good news is that the Social Security Administration has a system for sorting out some of these mistakes and assigning the earnings to the correct record. But nearly half of the mismatches are never corrected. That means that in 2012 there were approximately $35 billion in wages that was never credited to an individual’s Social Security history.

Why A Social Security Earnings Record Mistake Matters

A mistake in your earnings history can make a big difference in how your Social Security benefits are calculated. How? It all goes back to the benefit’s formula. The Social Security Administration uses your highest 35 years of earnings as a cornerstone of the benefit calculation. If any of these 35 years are incorrect or missing altogether, the average is skewed. One year of missing earnings can make a difference of $100 per month (or more!) in your benefit amount. Over your lifetime, that could be nearly $30,000 in missed benefits from one year of missing earnings.

You need to check your Social Security earnings record today. Thankfully, it’s pretty easy to do.

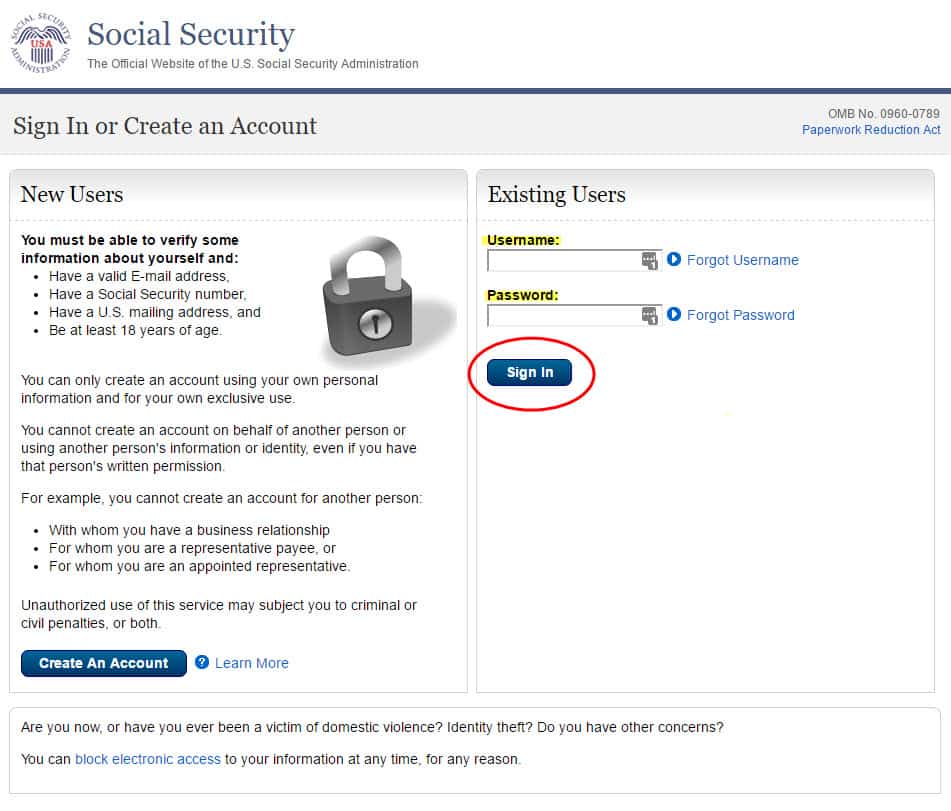

Here’s how to accomplish this in five easy steps.

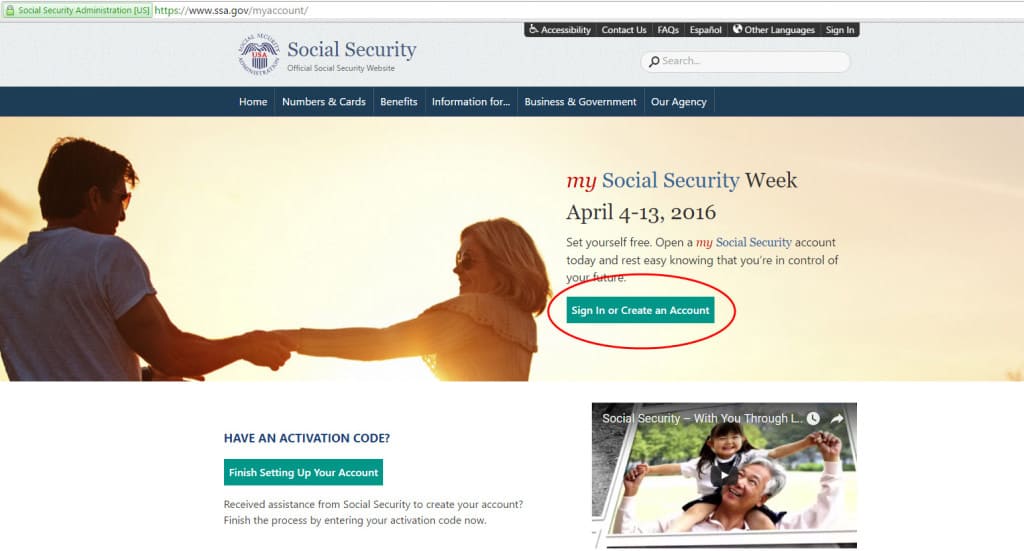

Step 1

Visit www.ssa.gov/myaccount to get started. If you click the link, it will open Social Security’s website in a separate page so you can keep using this guide.

Once the page loads, simple click on the button labeled “Sign In or Create an Account.”

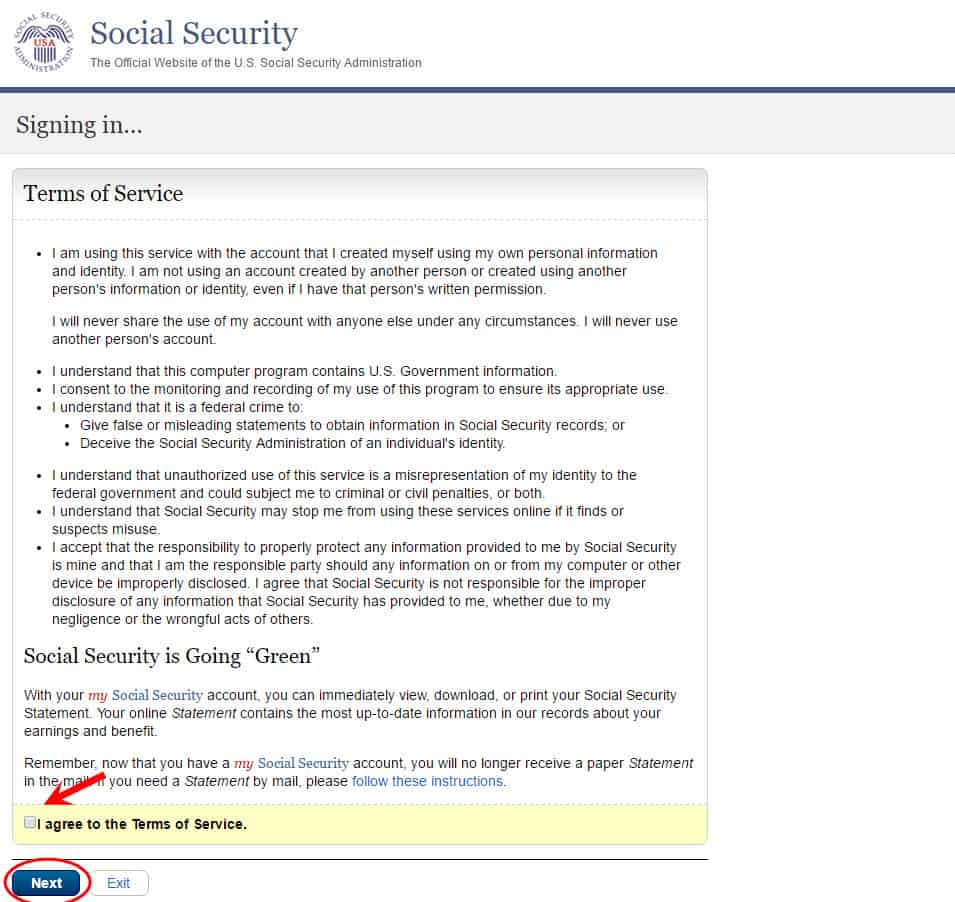

Step #2

Type your username and password and click the button labeled “Sign In.”

Step #3

In the third step, you need to read and agree to the my Social Security Terms of Service. Be sure to carefully read this page before clicking in the “I agree” box and then clicking “Next.”

Although you need to understand this information for yourself, here’s a summary of what you are agreeing to.

-You will never share your information with anyone or use anyone’s account

-Once you open an account, you will no longer receive a paper statement in the mail. Instead, you’ll receive an annual email reminding you to log in and check your information.

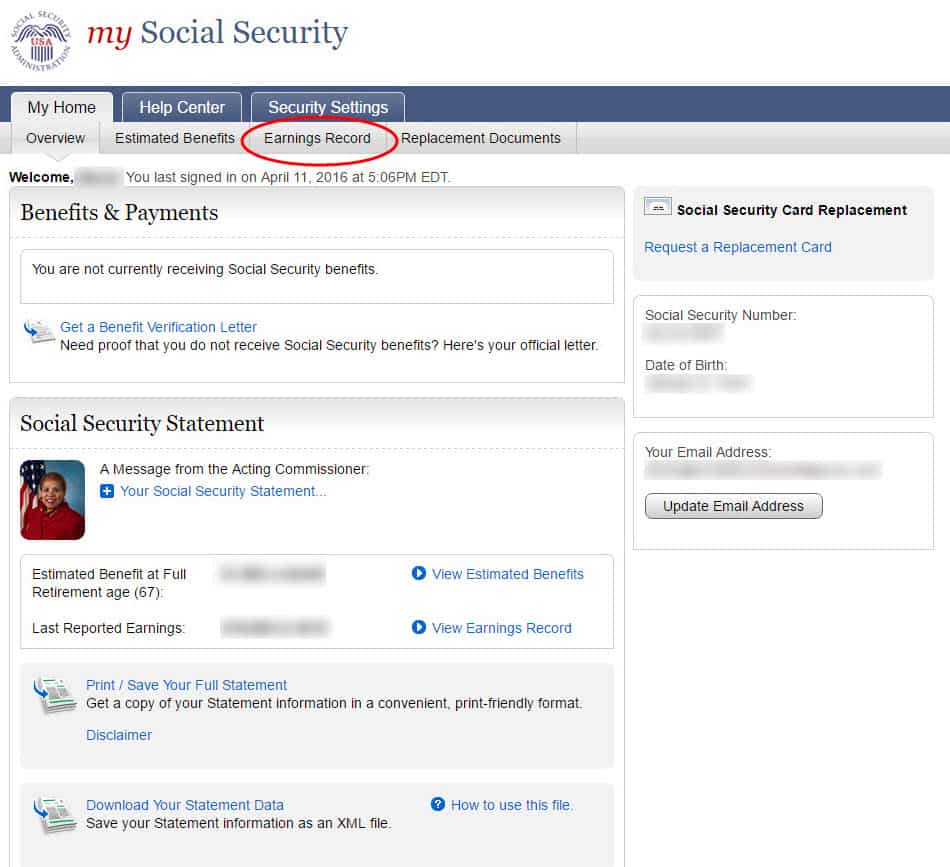

Step #4

Now that you are on the home page, you just need to click on “Earnings Record” tab at the top.

Step #5

On your screen you should see your earnings record. Check it carefully. If there is a mistake, the burden is yours to prove it. You’ll need to locate documents that prove the error such as tax forms, W-2 forms or pay stubs. If you can’t find these, Social Security says to write down the name and address of your employer, the dates you worked there, how much you earned and the name and Social Security number you were using while you were employed, and the agency will use this information to investigate the problem.

For more information from the Social Security Administration on the procedure, you can visit the section of their POMS manual that discusses this.

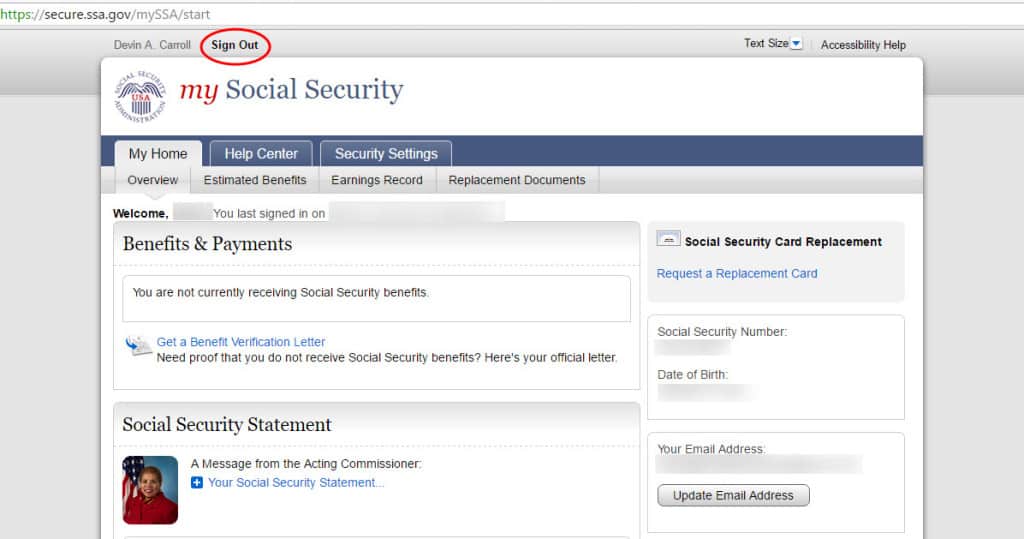

Step #5 1/2

Dont forget to sign out! This system has too much valuable information to leave it open.

If you have questions about any of this, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

“Do stay at home moms get Social Security benefits?”

My wife asked me that question a few weeks ago after the topic came up over lunch with friends. She thought she knew the answer, but after hearing the varied opinions of her friends she was confused.

Here’s how I explained it to her in one sentence.

“Social Security benefits are paid to eligible spouses and children if the working spouse becomes disabled, dies or retires.”

Your Social Security benefits statement has some really important information in it. But where do you find it?

Several years ago the Social Security Administration stopped mailing the annual benefits statement to save cost. Then they started back…but not for everyone. Now, you’ll only receive a statement 3 months before you turn age 25, 30, 35, 40, 45, 50, 55, and 60. After age 60, you should receive a statement every year.

I’m glad they started mailing them again, but for those under age 60 receiving a new Social Security statement every five years in not nearly often enough. Your estimated benefits are most likely changing on an annual basis when your yearly earnings are recorded. If you keep your retirement plan updated annually (and you should), you’ll need these numbers to change your calculations.

So forget waiting on the postal service to deliver this important document. Just use this step-by-step guide and you’ll be looking at your benefits statement in less than two minutes!