There are a few mistakes you can make with your Medicare

benefits that seem small, but actually carry some big, nasty consequences.

I’m talking about the kind of consequences that can cost you

thousands of dollars. That’s a lot of money that you could have on the line —

and the confusing Medicare system doesn’t make it any easier to avoid big

mistakes.

Medicare is full of confusing language, plans that seem awfully similar,

a lot of different deadlines, and more than a few hidden costs that can take

you (and your budget) by surprise.

I’ve seen more than a few people make these specific Medicare mistakes, and I want to help you avoid becoming just another one of many. Here’s what I see most often — and how you can avoid making these same errors.

Are you an educator or public servant who currently works — and will eventually be subject to Social Security’s Windfall Elimination Provision or the Government Pension Offset? Tired of waiting on your elected officials to keep their promises and repeal the WEP and GPO that punish workers like you?

If so, I have some good news: you have the power to get these rules changed. You just need to know what actions to take, and that’s what I want to share with you in this article.

It’s no secret that Social Security is not the easiest system to understand. A

maze of complex and complicated rules make it very hard to understand what is

and isn’t allowed, and there are a number of hoops everyone has to jump through

to ensure they get their benefits in the right amount.

Another not-so-secret fact about the system?

It’s plagued with problems, the biggest of which may be the fact that the

Social Security Administration’s trust funds will run out of money around 2035

unless someone finds a fix — and quick.

Considering this, it’s little wonder that people

are quick to take issue with anything about Social Security that seems to

indicate that someone is getting more benefits than they should. After all,

anyone receiving income from Social Security is pulling from a very finite pool

of resources.

The more money that goes to people who shouldn’t be receiving it means less for

people who truly need it.

So when it comes to people with felony

convictions who receive Social Security checks, it’s little wonder people get

very fired up about this topic. But there’s also a lot of misinformation

floating around about this topic, so let’s set the record straight about

whether felons have a right to Social Security or not.

A Felony Conviction Does Not

Automatically Disqualify Someone for Social Security

Not long ago, someone commented that the Social

Security system wouldn’t be in such trouble if we didn’t have prisons full of

people collecting disability and retirement benefits.

While I have a lot of content, in the form of

both blog posts and videos on my YouTube channel, dedicated to breaking down

and explaining the complex rules around Social Security, that comment made me

realize that I’ve never gone into detail on whether or not someone with a

felony conviction can receive benefits.

Here’s how this works: a felony conviction alone does not turn off your Social

Security benefits. But an individual cannot receive benefits while imprisoned

for more than 30 days for that conviction.

That detail is important! It means that if someone is arrested for a crime, and spends 90 days in county jail waiting on their trial, their benefits will continue. In order for the benefits to be suspended, they must be convicted and imprisoned for more than 30 days.

The Rules Around Medicare and

Other Benefits for Imprisoned Individuals

While we’re clearing up the misinformation

around whether or not convicted felons serving their sentences for their crimes

are eligible for benefits, let’s look at a few other important points that most

people don’t have the facts on.

If someone is on Medicare when they go to

prison, their Social Security benefits will stop. The automated payments to

Medicare Part B stop, as well — but those premiums are still due and payable.

If an individual does not pay their Part B

premiums, then their Medicare Part B coverage will discontinue. That person

would then have to reapply for benefits during an open enrollment period. The

result for that person would most likely be a much higher Part B premium.

The other interesting note is with regards to

spousal and childrens’ benefits. The rules are fairly clear that if a spouse or

child is receiving benefits from the work of an individual who is incarcerated,

that benefit will continue.

Keep in mind that before a spouse or child can

receive a benefit from another work record, the individual who owns that record

has to file first. If someone is in prison when they first become eligible to

file, then they can’t actually take that action — and if they can’t file, then

their spouses and children can’t receive their benefit.

What’s Your Take on This

Topic?

It’s easy to hear rumors like the one that a bunch of felons are sitting around collecting Social Security, and feel worried or concerned over whether that’s completely true. After all, Social Security is in some degree of trouble because funds will run out unless new rules or regulations go into effect soon.

But I ask that you really think this one

through. Some people believe that if an individual is being provided housing

and food by the government at taxpayer expense, they shouldn’t be able to get

any kind of Social Security benefit on top of that.

But you can consider this from another perspective, too. Some people say that if a prisoner worked for their entire life and contributed to the system, the government shouldn’t be able to seize any portion of that earned benefit.

Questions? If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too. Also…if you haven’t already, you should join the 100,000+ subscribers on my YouTube channel!

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

Worries and rumors and complaints about a broken system on

the verge of collapsing have been the norm when it comes to talking about

Social Security since as far back as the 1980s — and that shows no signs of

slowing down today.

With current projections showing the Administration’s trust funds run out in 2035,

it makes sense that people are still concerned and clamoring for a solution.

Wouldn’t it be nice if we could just fix Social Security once and for all?

It sure would be — and it might be easier than most people currently think. In fact, I believe there is a solution to fix Social Security. Not only would it repair a broken system, but it wouldn’t even require extensive legislation and the infrastructure is already in place to start administering this today.

Sound too good to be true? Keep reading and I’ll give you

all the details on the most obvious fix for Social Security’s current woes.

We CAN Avoiding Cutting Social Security

Benefits

It’s no secret that Social Security is facing financial

challenges ahead. Again, we know that within the next 15 or so years, there

will not be enough money coming in to pay out benefits.

Something has to change, and fast, or we can expect benefits

to be cut by around 25% across the board. Maybe that’s not a big deal for some

people… but for many others, losing a full quarter of your benefit payment

could be devastating.

This would be a good place to pause before I share my

solution, and give a quick warning to politicians who would like to stay in

office:

There are nearly 50 million individuals in the United States

over the age of 65. 25 million households get half of their family income from Social Security. More than 12

million get 90% of their income from Social Security.

That’s a lot of people — and this many people can easily swing election outcomes one way

or another. Since 1900, the average popular vote difference between the winner

and loser of a presidential election has been 5.8 million votes.

Clearly, there are more than enough voters here — voters

who have the majority of their income at stake — to easily swing an election

to the side of someone who can fix this system before benefit cuts happen.

My idea would not be difficult for politicians or the

government to implement, because the systems are already in place to put this

plan into action. So what is this great fix?

It’s very simple: it’s an extension of the Social Security

earnings limit to all ages.

Here’s how it would work.

Extending the Social Security Earnings Limit to

All Ages Could Fix the System

Under the current rules, if you’re younger than the full

retirement age then you can only make a certain amount of income before your

benefits are withheld. If you make over a certain amount in income, you don’t

get benefits at all.

But once you reach full retirement age, there is no limit on

the amount of earnings you can have outside of your Social Security benefit.

My fix would simply extend this current rule around the

earnings limit to apply that limit to all

ages. If your earnings exceed a certain amount — which would mean you don’t

actually need Social Security in

order to get by or afford your lifestyle — you would not be eligible to

receive benefits.

This would actually realign the system with the original

guidelines. It would also free up funds to go to those who truly rely on their

Social Security benefits to survive in retirement and have little or no other

sources of income to use.

Shouldn’t Social Security Go to Those Who Need

It Most?

When Social Security first began, the earnings limit applied

to all ages. In 1950, the earnings limit was eliminated at age 75.

In 1954, this was changed to age 72. Another change happened

in 1983 when the age was dropped to 70. Finally, in 2000, the rules changed for

a final time to make the earnings limit drop off at your full retirement age.

I’m certainly not the first to suggest this specific fix to

Social Security — although my simplified method of extending the earnings

limit may be new.

On the campaign trail in 2015, now-President Donald Trump

said, “I would be willing to say I will not get Social Security. But the fact

is that there are people that truly don’t need it, and there are many people

that do need it very, very badly.”

In the same campaign season, then-Governor Chris Christie

said, “We need to save this program for people who have paid into the system

and need it. This government doesn’t need more money to make Social Security

solvent. We need to be not paying benefits to people who don’t really need it.”

A Word on Fixing Social Security with Means

Testing

Although a means test has been suggested before, I haven’t

seen the research on the impact of such a change. One of my big questions about this is, where

would the earnings limit be set under this solution?

Ultimately, there is an earnings amount where cutting

benefits to individuals above the line would completely fix the system. Is that

number $15,000 in income? $25,000? Who knows?

To my knowledge this topic hasn’t been researched enough to

have a complete answer, which is where the means test seems most problematic to

me. It’s a big puzzle piece that’s missing and really needs to be known before

this proposal can get serious.

I know some people will say that even

my proposed solution of making the earnings limit something that applies to

everyone regardless of age is a form of means testing — and that it unfairly

punishes success.

As much as I agree with that,

the entire Social Security system is already

built on means testing. My fix doesn’t present a huge change due to the

progressive Social Security benefits formula.

Under that formula,

lower-earning individuals receive a benefit that is a higher replacement of

pre-retirement earnings than higher earning individuals. And once benefits

begin to be paid, lower earning individuals usually don’t have to pay any taxes

while those with higher incomes have to give some of it back through taxes.

Adding a “means test” like the

earnings limit applying to all ages wouldn’t really represent a monumental

policy shift.

The fact is, any solution we can use now will likely impact

anyone under 50 with a higher than average income. Even I don’t love my solution, as it impacts me, too!

This is probably something we need to get used to — and I

think a solution like the earnings limit applying to everyone is preferable to

a convoluted fix that only fixes part of the problem through half measures and

complex law. Let’s keep it simple so we can rip the bandaid off and get it over

with!

As this and other policies develop, I’ll be here to give you the details.

Questions? If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too. Also…if you haven’t already, you should join the 100,000+ subscribers on my YouTube channel!

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

The concept of paying taxes on Social Security benefits doesn’t sit well with many individuals. After all, the contributions you make in hopes of receiving a future Social Security benefit are after-tax dollars that were involuntarily taken out of your paycheck.

Now the benefit you receive from the system you funded for your working career could be taxed again?!?

I can see why many people feel this puts them on the hook for paying taxes twice on the same dollars. After all, isn’t there something in our complex tax code that stops double taxation? Let’s take a closer look at the issue to get clear on what’s going on.

Is There Double Taxation on Social Security Benefits?

Through the years I’ve read a lot about this issue, but I’ve never seen anything that adequately explained it. Most articles never go deeper than the surface level, which only adds to the confusion.

Most articles I’ve seen try to explain away the double taxation on Social Security benefits issue in a different number of ways. Let me know if any of these sound familiar:

It’s not double taxation because the funds you collect don’t come directly from your taxes. Your taxes are paying for today’s beneficiaries, so the benefits you receive will be from someone else’s payroll taxes.

You have to think about your payroll taxes as a premium into a retirement account. Just like distributions from retirement accounts, Social Security benefits are also taxable income.

Not all of the benefits you will receive will come from the tax you paid to help fund the system. Some of the benefit comes from interest on the trust funds, some comes from taxes collected, and the rest comes from payroll taxes.

It’s a “contribution,” not a tax. This allows the IRS to tax you on the money you put into Social Security and the money you receive out as a benefit — because on the way out, it’s technically not a tax. (I don’t care what you call it, it’s a tax! The original Federal Insurance Contributions Act (FICA), the Social Security Administration, and the IRS all explicitly refer to this as a tax.)

All the “reasons” to wave away the double taxation idea that you can easily find online sound like double speak to me. That also piqued my curiosity, so I dove into the research to figure out once and for all whether this is truly a case of double taxation.

Understanding the History of Taxes on Social Security

To understand the whole issue, we have to put some context around this. Let’s back up and look at the history of taxation, how it works and finally answer the question once and for all (although for the purposes of this article, we’ll only look at taxes on the federal level)

Social Security benefits were not taxable from January of 1937, when the first Social Security benefit was paid, until the beginning of 1984. The original thinking was that since FICA taxes are paid with after-tax dollars, the benefit from them should be tax-free.

This all changed as a result of the Greenspan Commission.

(Officially, this was known as the National Commission on Social Security Reform — but it’s commonly called the Greenspan Commission after its chairman, Alan Greenspan.)

Congress and President Reagan appointed this group in 1981 to figure out how to “fix” Social Security. Much like we hear all about today, the Social Security trust fund was also very close to running out of money in the early 1980s.

They had to do something — and fast!

The Introduction of Taxes on Benefits

The Greenspan commission saw taxing Social Security benefits as the low-hanging fruit to solve the problem, despite the fact that there were three separate Treasury rulings in the early days that explicitly excluded Social Security benefits as taxable income.

The rationalization for taxing Social Security benefits was based on how the program was funded. Employees paid in half of the payroll tax from after-tax dollars and employers paid in the other half (but could deduct that as a business expense).

This meant only 50% of payroll taxes were already taxed (the employee portion) and thus up to 50% should be taxable after it was paid.

The Greenspan commission believed this would align the Social Security rules with the ones that already existed for some pensions, annuities, and other retirement savings plans. The way this works is that if you contributed after-tax dollars to your pension or annuity, your pension payments are only partially taxable. You don’t have to pay tax on the portion of the payments that represent a return of the after-tax amount you paid.

The Greenspan commission argued that the portion of the payroll tax that the employer paid was deducted, and thus no taxes were paid on it… which created the loophole to make that portion taxable, but with the recipient of the benefit footing the bill even though the employer initially paid that portion into the system.

In late 1983, a law was passed which made up to 50% of an individual’s benefit count as taxable income.

Once this tax was widely accepted, it didn’t take long for the federal government to realize that they had been missing billions of dollars in potential revenue. The next step was to increase these taxes again.

Where the Increase in Taxable Benefits Came From

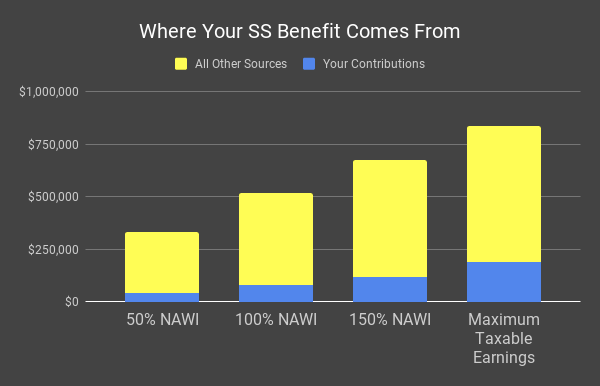

In 1993, a second “level” was added, making up to 85% of a Social Security benefit taxable. The rationalization they used to justify this was different than what the Greenspan commission used just 10 years earlier.

The members of the legislative committees decided that the average worker who lived to an average life expectancy will only contribute 15% of their expected total lifetime benefit in their part of the payroll taxes. Therefore, the other 85% must come from other sources and should be taxed.

For example, say someone earned an average wage and lived until an average life expectancy. They would likely receive a lifetime social security benefit of around $400,000.

But the employee only paid about $60,000 into Social Security. According to their logic, since that’s the only part that’s already been taxed, up to the remainder should be taxable.

Checking the Government’s Math: Unfortunately, They Have a Point

Although I didn’t want to admit it at first, the math here is mostly correct. A worker with average earnings who lives to an average age contributed payroll taxes that equal about 15% of their total expected lifetime benefit amount.

However, this doesn’t hold true if the worker’s income was in excess of the national average wage.

With the same life expectancy, an individual who earned 150% of the national average wage would have contributed approximately 18% of their total benefit. An individual who paid in the maximum Social Security taxes would have contributed around 23% of their lifetime Social Security benefit.

So…does the taxation of Social Security benefits constitute double taxation? Not unless you earned an income higher than the national average and have enough other income in retirement to have 85% of your benefit taxed.

But if you did…there will be some double taxation on Social Security benefits.

For example, if you worked from 1972 to 2019 and earned maximum wages, your part of the FICA tax to fund Social Security would have been around $190,000. If you file at your full retirement age and live to 85 (and get an average 2% cost of living adjustment), you’ll receive benefits totaling around $834,000.

If 85% of your benefits are taxable, you paid tax on the original FICA contributions plus $708,900 in benefit payments($834,000 x 85%). This means that in the end, you pay tax on $899,000 (85% of benefits + your part of FICA) despite having only received a total benefit of $834,000. Effectively, you get hit with double taxation on $65,000 worth of your benefits.

The Future of Social Security Taxation

If you’re breathing a sigh of relief that you won’t be impacted by double taxation on your benefits, you might not want to rest easy yet.

When Social Security benefits first became taxable, the change only affected the top 10% of retirees in terms of income earners. Now, that number is nearly 60%.

This number will likely continue to increase since the brackets that determine an individual’s income level at which point benefits become taxable has not changed since the law took effect.

In other words, the brackets are still set at 1983 and 1993 levels.

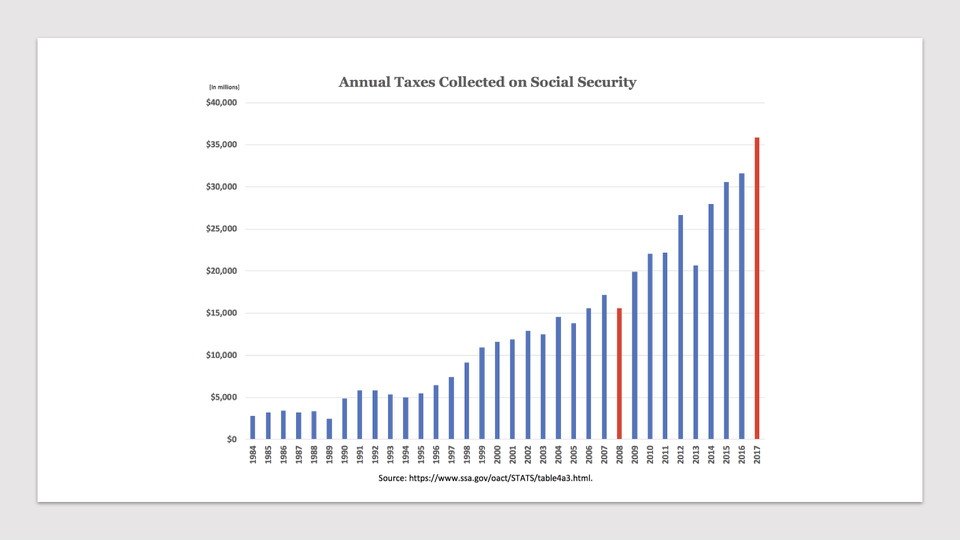

Needless to say, wages have increased between then and now. This becomes even more apparent when you look at the revenue the Social Security Administration is collecting from taxes on benefits; the tax revenue from Social Security has doubled in the last 10 years alone!

There have been a few proposals to eliminate the taxation of Social Security benefits, but with an estimated $13.2 trillion cash shortfall between 2034 and 2092, I can’t envision any proposal succeeding that would reduce revenues for the SSA. Taxes on Social Security benefits are probably here to stay.

But just because taxes may be inevitable for some, you can still plan to lessen the impact. The most obvious strategy would be to simply lower your income — but that’s not appealing or realistic for most of us.

The best option may be to build a strategic plan before you retire. For example, distributions from a Roth IRA or 401(k) are not counted against you in determining whether your Social Security benefits are taxable. You could have an unlimited level of income from these sources and still not pay tax on Social Security.

If you start now, your traditional IRA and 401(k) balances may be able to be converted to Roth accounts.

Could this be an option for you? It may be depending on a number of factors that your financial planner and tax professional can help you unravel. You’ll certainly need to keep the big picture in mind when planning.

If I can help you with your financial planning or investment issues, please don’t hesitate to contact me here.

Questions?

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too. Also…if you haven’t already, you should join the nearly 400,000 subscribers on my YouTube channel!

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

The

government really is watching you. Or

at least, the Social Security Administration is watching your social media

accounts.

It

might sound like the plot of a movie, or the latest conspiracy theory about Big

Brother out to get you. But it’s true: the Social Security Administration (SSA)

wants to increase its monitoring of social media accounts.

This isn’t a future

threat. It’s happening now. The SSA already monitors social media posts from

individuals who are on disability. The purpose is to help identify and

investigate fraudulent disability claims, but what may change is when they

begin monitoring.

Why the Social Security Administration May Increase Its Social Media

Surveillance

The SSA wants to

start using social media activity not just to catch or track potential cases of

fraud. They want to use social media content as part of the evaluation of a disability application.

If you file for

disability, the Social Security Administration could start checking out your

Facebook, Instagram, and other social networking profiles to make sure you

aren’t behaving in a manner inconsistent with your disability.

For example, if you

file a disability claim for degenerative disc disease, the SSA could

potentially check out your social media

posts to verify that you aren’t participating in activities that would be

inconsistent for someone with chronic back pain.

Here’s what you need to

know about this potential ability of the SSA to keep an eye on you online.

With Financial

Challenges Ahead for Social Security, Expect Crackdowns

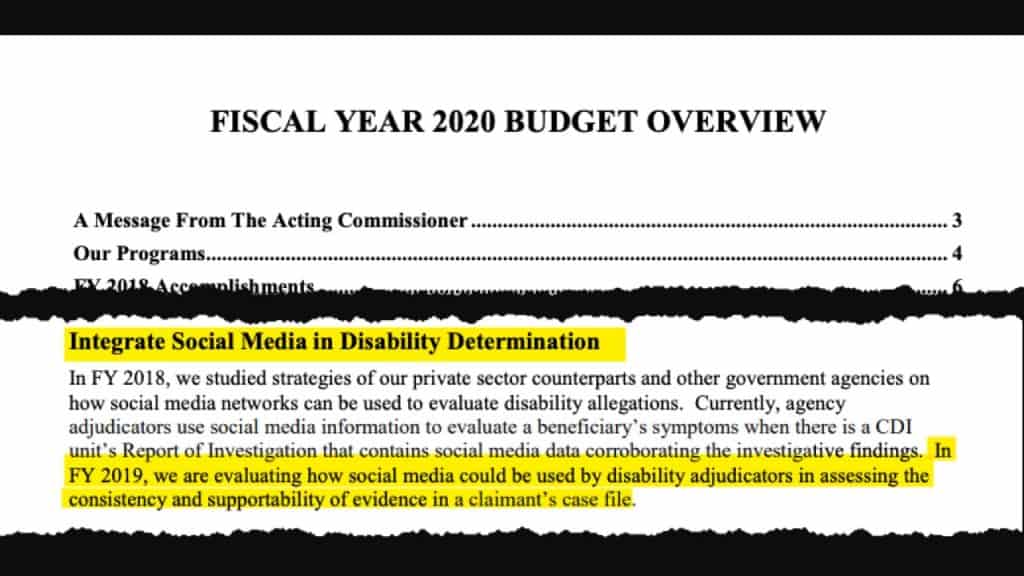

The SSA’s Fiscal Year 2020

Budget Overview addresses the potential for increased social

media surveillance. The document includes this line explaining what the

administration may roll out in the near future:

“We are evaluating how social media could be

used by disability adjudicators in assessing the consistency and supportability

of evidence in a claimant’s case file.“

It’s no surprise that the Social Security

Administration has turned to this. Since 1970, there has been a 460% increase of individuals on disability.

Unfortunately, there’s no doubt that at least some of these cases are

fraudulent.

The SSA wants to increase their efforts to

identify and prosecute these claimants — especially considering the

administration faces huge financial challenges to continue funding the program.

With an uncertain future for Social Security in general, this increasing burden

on the system only makes things worse.

Frankly, I’m not shocked that the SSA might

increasingly mine social media platforms and profiles for proof of fraud — I’m

only shocked that it took them this long to consider this approach.

Social Media’s Popularity Means There’s an Abundance of Data

for the SSA to See

There are more people using social media

accounts than ever before. According to the Pew Research Center, 69% of all adults have at

least one social media account. (Just for reference, this was 5% in 2005.)

50% of those who don’t have a social media

account live with someone who does and in the same research report it shows

that a good percentage of these individuals use the account of the other person

to see posts.

And all those people on social networks?

They’re sharing content — and personal information and data — like crazy. On

average, people upload 350 million photos to Facebook every day. The

platform experiences 100 million daily video views and 4 million likes every

minute.

The desire to share the details of your daily

experience with your interconnected network helped to drive this kind of growth

and mass adoption of the platforms. This treasure trove of data is too tempting

and valuable for the SSA to continue ignoring as part of their evaluation.

How Will the

Social Security Administration Truly Leverage Social Media for Monitoring and

Surveillance of Potential Claimants?

Again, I’m not

surprised to see the SSA want to take advantage of the ability to look in on

the real lives of people requesting benefits from the program to confirm their

claims are legitimate. But the problems come in with the application of the

policy.

How would this work? As

users of social media, we understand that each photo or video has to be taken

in context (and with a grain of salt). We all know that social media serves as

a highlight reel of our lives and doesn’t always portray reality very

accurately.

In other words, we’ve

all posted content meant to paint us in a good light or to make our lives look

just grand all the time (even though 5 minutes before you posted a happy

picture of you and your spouse you had a screaming match in the living room).

We all do this, and on

some level, we all know other people do it too. As users of social media, we

understand that what we see on the platforms isn’t 100% representative of our

24/7 daily lives.

But what happens when

that personal connection is lost? What happens when there’s no context to the

photos and your content is taken at face value with no other information taken

into account? Will the SSA understand the context around a photo enough to make

a decision about whether you are really

disabled?

For example, the leading cause of disability

payments are made due to “musculoskeletal and connective tissue” disorders.

That seems easy enough to evaluate through images and videos.

After all, if an

individual files a claim for disability on the basis of chronic Fibromyalgia but posts a current video of them winning their age group

in a marathon, that seems like a no-brainer. Maybe they shouldn’t be on disability.

But again, given the

tendency to present our best self to our network on social media, we tend to

only post the photos showing us happy and healthy.

Imagine you live with

daily chronic back pain, but have a rare day of low pain. Do you think you

might be more likely to post photos of yourself and your activities from that particular

day than the next few days where confinement to a bed is a real possibility?

You might share those

rare, fleeting moments not only because you’re likely happier on that one day

you experienced unusually low pain, but also because you may have enjoyed doing

something you’re rarely in any physical condition to do, like hike a favorite

trail.

At around 26%, the

second leading reason for disability payments are from “all other mental

disorders.” How will the SSA use a social media account to evaluate those claims? Does a picture really show

what’s going on inside the mind?

I think the

investigation of potential fraud is important, but it needs to be done

correctly. The Social Security Administration should understand that life on

social media is generally not an accurate recording of someone’s real circumstances.

Regardless of what the Social Security

Administration begins doing with social media monitoring, all of us should use

this as a reminder that what we say and post online matters and could have

consequences.

As this and other policies develop, I’ll be here to give you the details.

Questions?

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too. Also…if you haven’t already, you should join the 100,000+ subscribers on my YouTube channel!

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

Not long ago, a viewer on my YouTube channel asked me to give her a good reason why we have the Social Security earnings limit. The comments that followed showed how many viewers shared the belief that the earnings limit is unfair and should be eliminated.

In my response, I explained that the rationale behind the entire program of Social Security was a safety net. The original intent of the Social security program was not to supplement retirement income, but to keep the elderly (most of whom lost any potential long-term wealth in the Great Depression) out of poverty.

I also added that today’s earnings limit is relatively generous compared to where the Social Security earnings limit began. Let’s take a walk through history and see how the earnings limit has evolved.

Understanding the Origins of the Social Security Earnings Limit

The original Economic Security Bill which is what the Social Security Act was originally called) President Roosevelt sent to Congress featured a very restrictive earnings limit.

It said, “No person shall receive such old-age annuity unless . . . He is not employed by another in a gainful occupation.”

Whoa! This means that if you had even a single dollar in wages from a job, you could not collect a Social Security benefit at all.

The Bill reached Congress and then made its way into the House Ways and Means Committee. After holding hearings, committee members suggested dropping the retirement earnings test — but the Senate Finance Committee ultimately decided that the earnings limit should remain.

Eventually, the House version without the earnings limit passed by a vote of 372 to 33. The Senate version with the earnings limit passed by a vote of 77 to 6. After a couple more months of wrangling over details, the government signed the final version of the Bill featuring the earnings limit into law.

The final version of the Social Security Act of 1935 contained this language on the subject:

“Whenever the Board finds that any qualified individual has received wages with respect to regular employment after he attained the age of sixty-five, the old-age benefit payable to such individual shall be reduced, for each calendar month in any part of which such regular employment occurred, by an amount equal to one month’s benefit.”

(Keep in mind that age 65 was the earliest age of eligibility during the first few decades of Social Security.)

Over the next few years, lawmakers realized they needed to make the term “regular employment” more clear and better defined. In the 1939 amendments to the Social Security Act, they defined “regular employment” as having earnings of less than $15 in one month.

How the Earnings Limit Evolved Over Time

By the late 1940s, post-WWII wages rose and the $15 earnings limit became outdated. In the 1950, lawmakers passed more amendments that eliminated the retirement test for applicants at age 75. They also increased the earnings limit from $15 to $50.

The 1950s also saw the vast expansion ofSocial Security, and an additional 10 million people, including many self-employed individuals, gained Social Security coverage.

The earnings test for the self-employed was set at $600 per year initially, but in 1952 that jumped to $900 per year. Meanwhile, the earnings test amount also increased for employees, from $50 to $75.

The 1954 amendments reduced the age where the earnings test no longer applied from 75 to 72. The differences between wage earners and self employed were also made uniform with an annual earnings test.

Up until this point, wage earners faced a monthly test but self-employed individuals had an annual limit of $900. With the new law, the earnings test would only apply if earnings exceeded $1,200. Then, for every $80 increment, one month’s benefit would be withheld.

Further Changes to the Earnings Test through the 1960s and 1970s

The 1960 amendments introduced the phase-in earnings limit where an individual could still exceed the limit without a total loss of benefits.

For earnings between $1,200 and $1,500, the reduction was $1 for every $2 of earnings. For earnings over $1,500 the reduction amount would be dollar for dollar.

From this point forward, the earnings limit used this phase-in approach. The 1961 amendments increased the upper limit to $1,700 from $1,500 while the 1965 amendments changed this range again.

Recipients could then earn up to $1,500 a year and still get all their benefits. If, however, earnings exceeded $1,500, $1 in benefits would be withheld for each $2 of annual earnings up to $2,700 and for each $1 of earnings thereafter. The 1967 amendments modified this range from $1,680 to $2,880.

The 1972 amendments modernized the method used to determine the earnings limit. Previously, only an act of Congress could mandate an increase in the earnings limit amounts. The 1972 law put the increases “on automatic” by tying them to increases in the average wage index. This became effective in 1975.

From 1977 to Now: The Modern Way the Earnings Limit Evolves

The 1977 amendments earnings limit changes focused on allowing older Americans to access much-needed Social Security benefits to supplement their retirement incomes.

The House passed a bill eliminating the earnings limit at age full retirement age. The Senate passed a similar bill, but it didn’t eliminate the earnings limit until age 70. Ultimately, the conference committee accepted the Senate position and the final legislation ended the earnings limit at age 70 (but it didn’t officially come into effect until 1983).

The 1977 amendments also separated those who were under full retirement age and those who were over full retirement age. They granted a more generous earnings limit of $6,000 annually for those who were are or above full retirement age.

In the 1983 amendments, lawmakers expanded this by not only giving those above full retirement age a higher earnings limit, but also decreasing the amount of withholding by reducing the withholding to $1 for every $3 over the limit. Even though this change was legislated in 1983, it went into effect in 1990.

The next major change introduced the earnings limit as we know it today. The Senior Citizens Freedom To Work Act of 2000 permanently ended the earnings limit at full retirement age and increased the amount an individual can earn in the calendar year they attain full retirement age.

Since 2000, except for the annual increases, the earnings limit has been unchanged. As you can see from the timeline above, this is the longest period the earnings limit has ever gone without substantial changes.

Part of that is due to the automation of the increases by tying in with the annual changes in average wages, but there has been some talk about the earnings limit being one of the fixes for the pending shortfall in the Social Security trust fund.

The argument is that the earnings limit could be reinstituted for any ages if their income exceeded certain thresholds. This would be the “means testing” that would exclude high income individuals from drawing a Social Security benefit. That may never happen, but the framework certainly seems to be in place for those with high income — even if they’re above full retirement age.

Whatever changes come, I’ll be sure to keep you informed! You can keep up with me on my YouTube channel the other projects I’m involved with.

Also, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

If you want to read more on this subject, check out these resources below.

The gradual phase-in of taxes on Social Security benefits can deliver some unexpected and unpleasant results if you fail to recognize the “danger zone” to avoid. The calculation the IRS uses to determine how to tax Social Security income creates a category where taxes on benefits are amplified.

Fall into this danger zone, and you could pay a much higher tax rate on some of your retirement income. Here’s what you need to know about the taxes on Social Security benefits and how you can avoid the pitfall of paying way too much in taxes on that income.

Know Which Category You’re in for Taxation

Individuals fall into three basic categories for taxation on Social Security:

None of your benefit is taxable income

Between 0% and 85% of your benefit is taxable income (this is the danger zone!)

85% of your benefit is taxable

In the first category, you have no real need to fear slipping into the danger zone unless you have other income that could push you into the second category.

If you’re in the third category, you have few options to exercise to pay less in taxes.The only real choice you have is to somehow lower your reported income so that you qualify for the first or second category.

This is probably unrealistic, as people who find themselves in the third category are there thanks to large incomes from pensions, required minimum distributions, or some other source. You may need to accept that 85% of your benefit is taxable.

But if you find yourself in the second category, you may have more control over how much of your benefit is taxed.

Understanding the Danger Zone

I call that second category the danger zone because this is where taxes can nearly double on income.

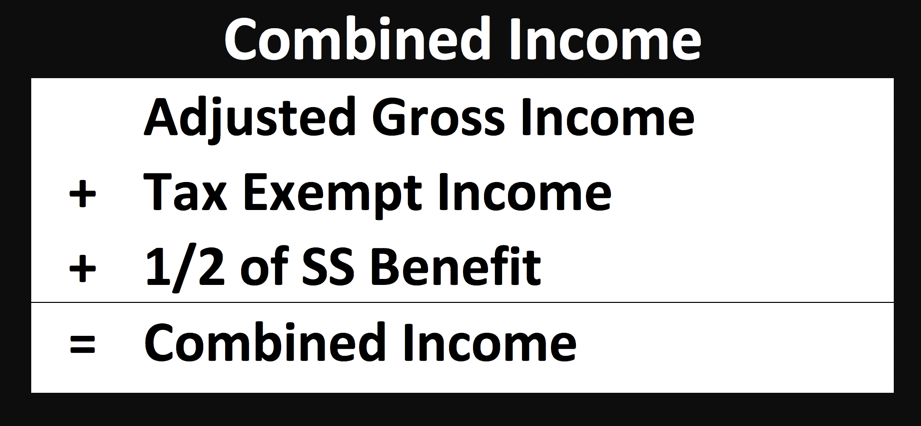

For some, this “danger zone” of magnified taxes can easily be avoided with a strategic, well-thought retirement income plan. The first thing you need to be able to do is to calculate your combined income.

This is the number the Social Security Administration uses to determines how much of your benefit is taxable. It’s also referred to as “provisional income,” but we’ll use the specific term combined income since the Social Security Administration uses that term.

Combined income can be roughly calculated as your adjusted gross income, plus any tax exempt interest (such as interest from tax free bonds), plus 50% of your Social Security benefits.

Once you’ve calculated your combined income you can apply it to the threshold tables to determine what percentage, if any, of your Social Security benefit will be included as taxable income.

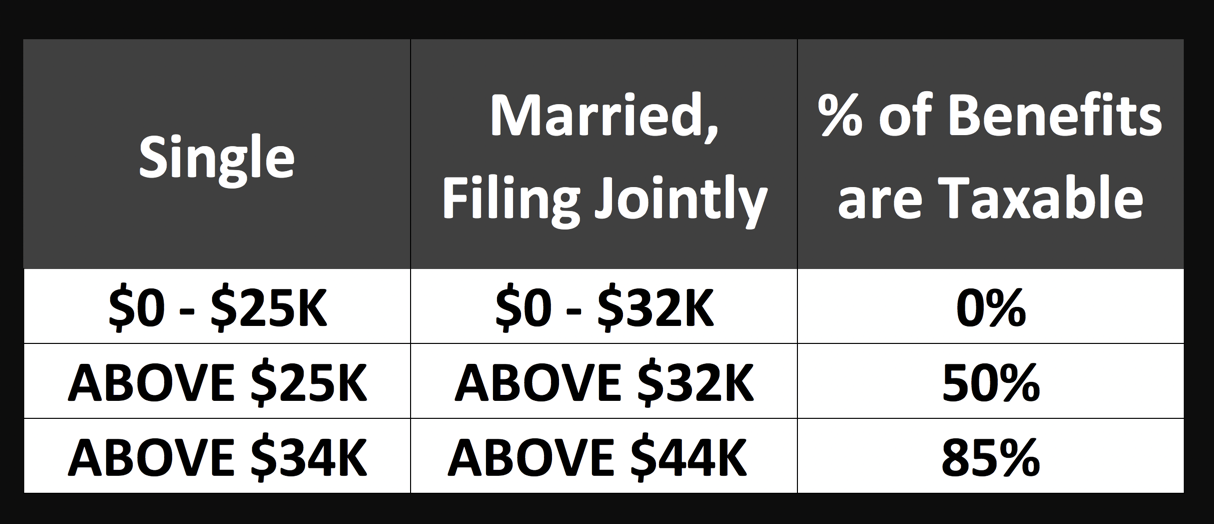

Thresholds for Social Security Taxes If You File Single

If your total combined income is less than the base amount of $25,000, none of your Social Security benefits will be taxed. But if your combined income is between $25,000 and $34,000, up to 50% of your benefit may be taxed.

If your combined income is more than $34,000, up to 85% of your benefits may be taxed.

Thresholds for Social Security Taxes If You’re Married Filing Jointly

If you file a joint return and you and your spouse have a combined income that is less than the base amount of $32,000, none of your benefits will be taxable.

If your total combined income is between $32,000 and $44,000, up to 50% of your benefit is taxable.

If your combined income is more than $44,000 up to 85% of your benefit may be taxable.

This system is a gradual phase-in of tax on Social Security benefits where, as income rises, more of your Social Security benefits are subject to taxation, until eventually a maximum of 85% of all benefits are subject to taxation.

For a more in-depth reading check out my article on the taxation of Social Security benefits.

What Happens to Social Security Taxes in the Danger Zone

Because of the way Social Security income phases into taxation through this formula, there is a “danger zone” when every dollar of increase in combined income pulls more Social Security into taxation.

In this zone, the effective tax rate on this other income skyrockets. For example, if an individual is in the upper end of the danger zone and takes $1.00 from his IRA account, they’ll not only have to pay tax on that $1 but also on $.85 of their Social Security benefit.

Effectively, because they took out $1 they had $1.85 added to their taxable income. This has the effect of increasing the marginal tax rate well beyond what your tax bracket might suggest you are paying.

If your tax bracket is 25% you would ordinarily pay $0.25 on the dollar you took out of your IRA. However, since that $1 increased your taxable income by $1.85, you will have to pay $0.46 in taxes. Since that $0.46 in taxes is solely due to your $1 distribution, you’re paying a 46% tax rate on that dollar!

This whole effect has been referred to as the tax torpedo — but for purposes of this article we’ll refer to it as the “danger zone” since my goal is to help you identify a specific range of provisional income where one should be hyper-vigilant about the effect of taking IRA distributions.

The danger zone ends when the results of your combined income calculation reaches 85% of your social security benefits. At this point, 85% of your benefit will be taxable, so increased combined income will not have the magnified effect.

For example, if you take $1 in IRA distributions it will not expose an additional $0.85 of Social Security benefits to taxable income since your benefit is already taxable.

Also, since all Social Security benefit amounts are not the same, the point where the danger zone ends will be different for everyone. Below we’ll break down the different ranges for those married filing jointly and those filing single.

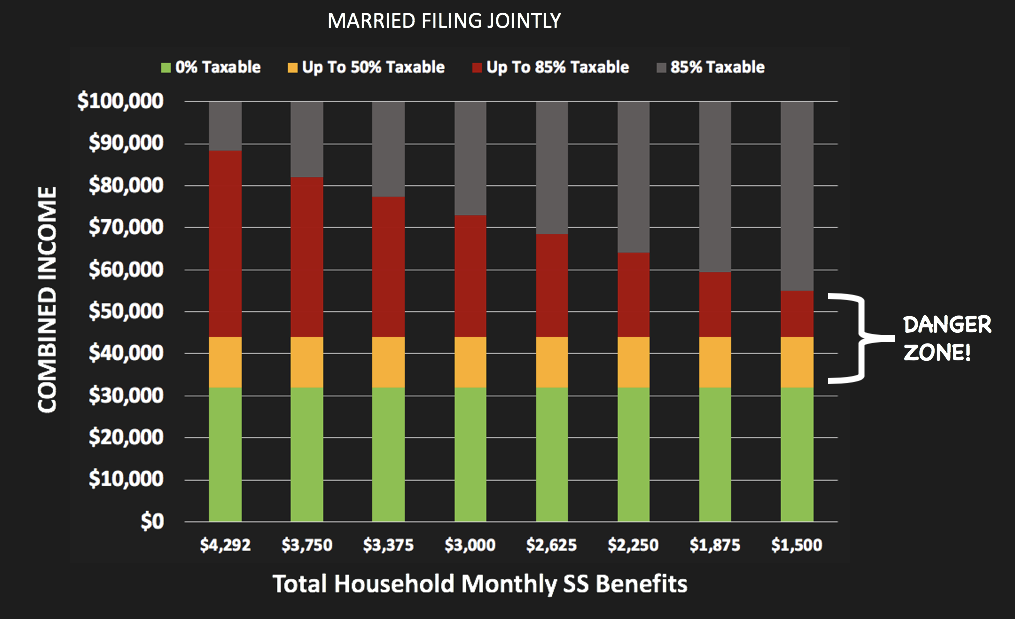

Where the Danger Zone Ends If You’re Married Filing Jointly

For those who are married filing jointly, exercise caution when combined income income rises over $32,000. At this point, your Social Security benefit will be added to your taxable income at the rate of $.50 for every additional dollar in combined income (signified by yellow on the chart below).

At $44,001 of combined income, your Social Security benefit will begin to be included in taxable income at the rate of $0.85 for every additional dollar in combined income (see the red areas of the bars in the chart below).

You’ll notice that the point at which someone can exit the danger zone varies based on the benefit amount. This is because the exit point is the point where the full 85% of your benefit becomes taxable.

The danger zone ends for those who are married filing jointly at around $88,000 for those who have a maximum benefit in 2019 and half of their benefit is being paid as a spousal benefit.

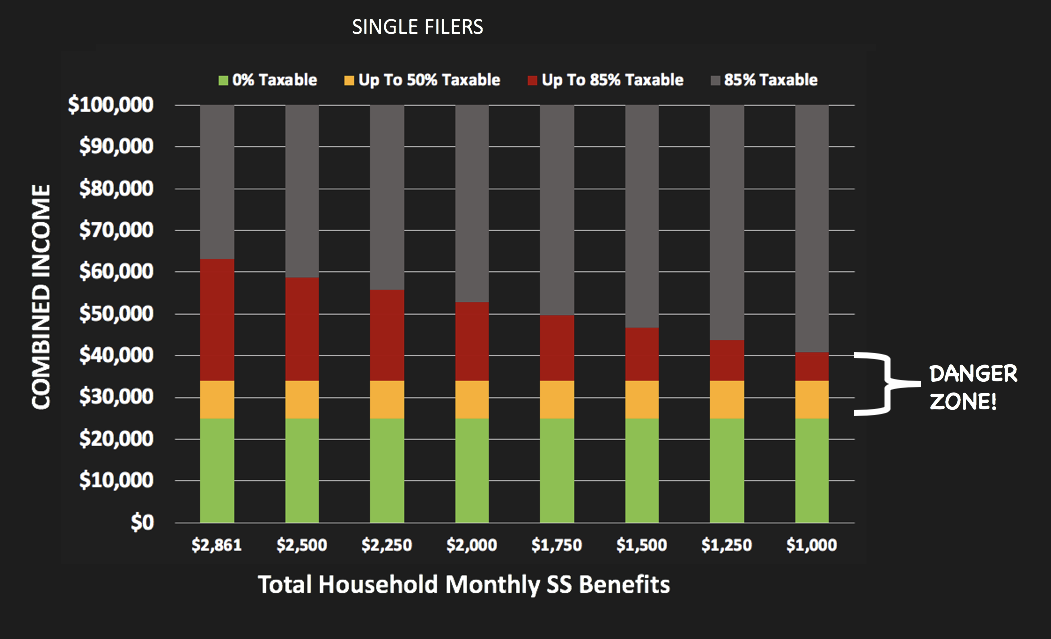

Getting Out of the Social Security Taxes Danger Zone for Single Filers

You need to start paying attention when your income rises above $25,000. At this point, your Social Security benefit will be added to your taxable income at the rate of $.50 for every additional dollar in combined income (signified by yellow on the chart below).

At $34,001 of combined income, your Social Security benefit will begin to be included in taxable income at the rate of $0.85 for every additional dollar in combined income (see the red areas of the bars in the chart below).

The danger zone ends for single filers around $63,000 in combined income for those with a maximum benefit (2019). For individuals with lower benefit amounts, you’re in the clear sooner.

The Opportunity Zone

In some cases, there is nothing to be done that will help lower the amount of taxes on Social Security. It could be due to required minimum distributions, pensions or a variety of other income sources.

Whatever the reason, some people will simply have incomes that are too high to make it possible to lower back into a zone of less than 85% Social Security taxation.

However, there are opportunities for planning around this danger zone. This opportunity not only exists for those who are in the danger zone, but also for those just over or under the line of the danger zone.

For those just over the line, it may be possible to defer capital gains, IRA distributions, or some other type of income if you could reduce the percentage of your taxable Social Security income by a few points.

Fully understanding how much range you have before Social Security benefits become taxable can be a big help in making choices about realizing capital gains, extra income from a job, or even deciding what type of account to use to fund your travel plans.

If you’re inside the danger zone, be aware that any increase in combined income will have an amplified effect on taxation. Instead of waiting until you are in that zone, there are a few steps you can take before it becomes an issue.

For starters, consider using a Roth IRA. This is possibly the most valuable tool for planning around tax on Social Security. Why? Distributions from a Roth are not counted in your combined income!

If you think you may eventually be in this danger zone, consider building a pool of money in your Roth account. You may be able to contribute to a Roth IRA up to $6,000 ($7,000 if over the age of 50).

Check with your retirement plan at work, as well, to see if they offer a Roth option. Using a Roth in 2019 will allow you to put in up to $19,000 per year ($25,000 if over the age of 50).

Finally, you may want to consider converting traditional IRAs to Roth IRAs. There’s certainly a lot to consider when doing so, but since the tax benefits could extend beyond the tax free nature of the Roth, this could be a winning move.

One thing is for sure, planning your retirement income stream is worth the effort! If I can be of assistance, please contact me at https://devincarroll.com/contact/

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

One last thing…I’d like to give a huge thanks to two individuals who helped me with this article. Jim Blankenship, CFP, EA for his expertise on taxation and social security and Brandon Renfro, Ph.D. for his assistance on the research behind these calculations.

Many Americans believe that future Social Security payments are an “earned right” when they retire. As nice as that would be, that’s not the case.

The truth is, you are sadly mistaken if you believe you’re entitled to these benefits down the road — even if you pay FICA taxes!

And if you’re sitting there, nodding your head, saying “that’s right, you’re not entitled to anything!” …you might want to sit down and read the rest of this post, too.

Social Security isn’t a guarantee, and it is in fact an entitlement program.

Scratching your head yet? Let me explain… and more importantly, let me try to reduce some of the inflammatory language around this conversation.

Why Aren’t Social Security Payments Guaranteed?

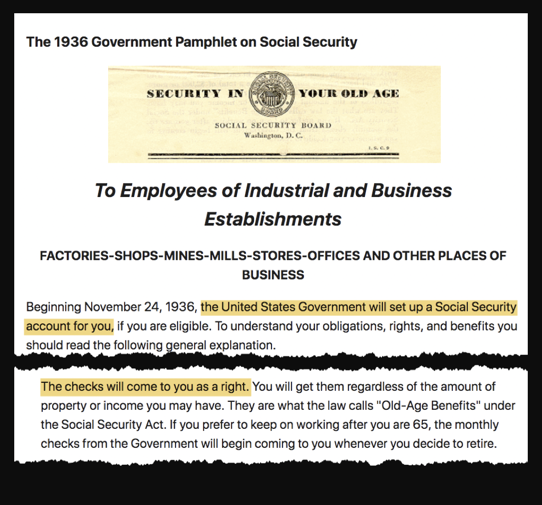

The government almost encourages the belief that Social Security benefits are guaranteed. In fact, in a 1936 pamphlet from the Social Security Administration, it specifically states, “The United States government will set up an account for you … The checks will come to you as a right.”

Whether or not it was intended this way, this pamphlet implied that the new tax would be somehow credit a personal account to which the worker would be lawfully entitled to receive. It didn’t take long for that to get “clarified” by the Supreme Court.

Not long after the Social Security began, a shareholder of the Edison Electric Illuminating Company challenged the tax that funded the program. He wanted to stop the company from making the tax payments and deductions from wages on the grounds that the Social Security Act of 1935 was unconstitutional.

For a period, it appeared that he won. The U.S. First Circuit Court of Appeals held that Title II of the Social Security Act (the heart of the program) was void as it was in direct opposition of the tenth amendment. However, once the case reached the Supreme Court, things changed.

The Ruling That Nixed Future Guarantees on Your Benefits

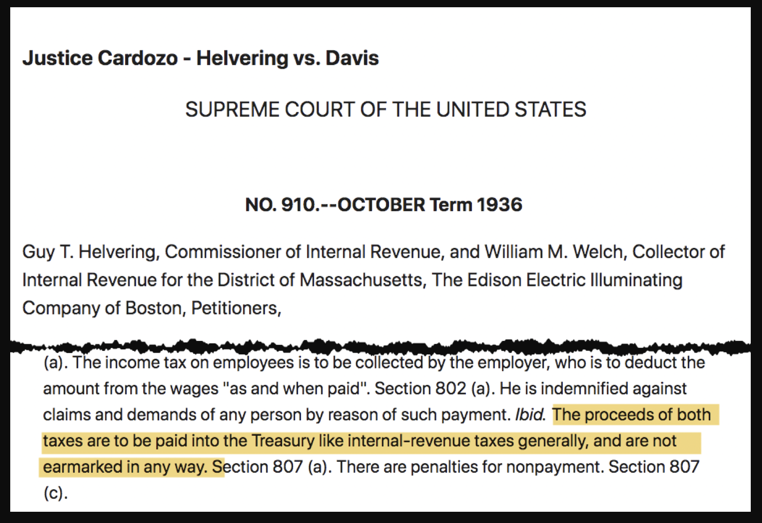

In Helvering v. Davis, the Supreme Court reversed the lower court’s opinion and held that the Social Security Act of 1935 was constitutional.

That in itself was not the interesting part. What was interesting was the language that was used in the written opinion. It said, “The proceeds of both taxes are to be paid into the treasury like internal-revenue taxes generally, and are not earmarked in any way.”

That eliminated the idea of the separate, personal account that the Social Security pamphlet originally implied.

Other Court Cases Made It Clear: Social Security Payments Not Guaranteed

In 1960, another case came up that made it clear how the government felt about the individual’s “right” to Social Security benefits.

Ephram Nestor was a Bulgarian immigrant who paid Social Security taxes from 1936 until his retirement in 1955. In 1956, he was deported for his membership in the Communist Party during the 1930s.

In accordance with a 1954 law Congress had passed a law saying that any person deported from the United States should lose his Social Security benefits, Nestor’s $55.60 per month Social Security checks were stopped.

Nestor sued, claiming that he had a right to Social Security benefits regardless because he paid Social Security taxes.

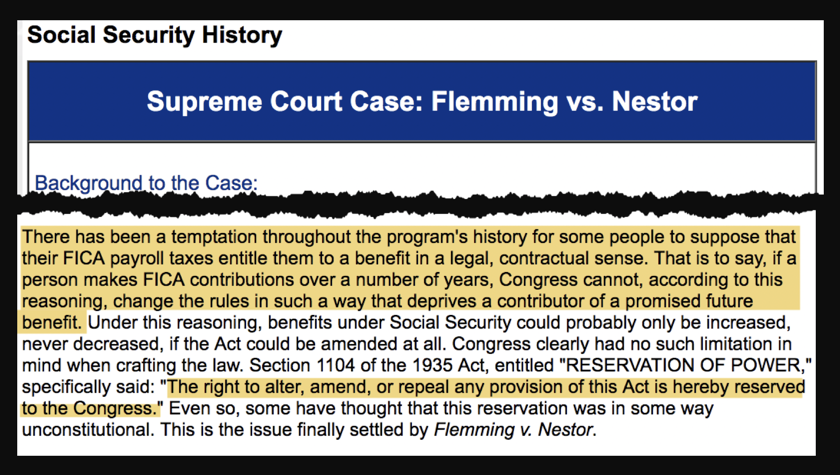

This case made its way to the Supreme Court in Flemming v. Nestor. In the Social Security Administration’s summary of the court’s findings, they state the following:

“There has been a temptation throughout the program’s history for some people to suppose that their FICA payroll taxes entitle them to a benefit in a legal, contractual sense. That is to say, if a person makes FICA contributions over a number of years, Congress cannot, according to this reasoning, change the rules in such a way that deprives a contributor of a promised future benefit. Under this reasoning, benefits under Social Security could probably only be increased, never decreased, if the Act could be amended at all. Congress clearly had no such limitation in mind when crafting the law.”

If there was any doubt left about an individual’s “right” to a Social Security benefit, this case should’ve banished it.

But just in case people forget that benefits can be changed or stopped altogether at any time, the Social Security Administration puts this reminder on every statement they create:

“Your estimated benefits are based on current law. Congress has made changes to the law in the past and can do so at any time.”

Paying FICA Taxes Does Not Make Your Social Security Payments Guaranteed

The big takeaway is that your payment of FICA taxes is not necessarily paying for your future access to Social Security benefits. The criteria for eligibility could change with the whims of politics.

Ultimately, you should heed the advice that’s also printed on each and every Social Security statement:

“Social Security benefits are not intended to be your only source of income when you retire. On average, Social Security will replace about 40 percent of your annual pre-retirement earnings. You will need other savings, investments, pensions, or retirement accounts to live comfortably when you retire.

The Social Security Administration today makes it clear that you have no legal right to Social Security benefits, and there are multiple court cases that set precedent to back this up.

Whether or not you agree does not change the reality that paying FICA taxes does not provide you a guarantee to any future benefit from the program.

While Benefits Aren’t Guaranteed… Social Security Is an Entitlement Program

Given the current level of political division, its no surprise that the dialogue about government entitlement programs has gotten really heated.

Many of our congressmen and senators have discovered how polarizing the use of the word “entitlement” is and that they can associate it with words like welfare, handouts, or charity.

Then they can fire up their supporters by loudly proclaiming SOCIAL SECURITY IS NOT AN ENTITLEMENT!

What’s happened here is that they’ve effectively redefined the word “entitlement” into something that is divisive and dirty. How handy.

Here’s the truth: the federal government has referred to Social Security as an entitlement program for several decades.

On their website, you can see hundreds of uses of the word. In fact, they go so far as to explicitly state “The social security benefit programs are entitlement programs.”

What Does Entitlement Really Mean, Anyway?

If you examine the definition of the word “entitlement,” you’ll see there is no mention of welfare, charity or handouts:

The Merriam Webster dictionary defines it as “a government program providing benefits to members of a specified group.”

The Cambridge dictionary defines it as “something, often a benefit from the government, that you have the right to have.”

The glossary of the United States Senate defines the word as “a federal program or provision of law that requires payments to any person or unit that meets the eligibility criteria.”

The fact is, the phrase “entitlement program” is simply a term for any government program guaranteeing certain benefits to a segment of the population who qualify for them under specific terms and conditions.

That’s exactly what Social Security is. You have to work for at least 10 years with a certain amount of earnings to be entitled to your own benefit. There’s nothing dirty, shameful or beggarly about this word.

But in the highly politicized world that we live in, what words actually mean and the meaning given to words aren’t always the same.

I hope this helps keep you grounded in the reality we’re working with, and not get swept away by anyone else’s political rhetoric.

Have More Questions?

If you still have questions, you could leave a comment below, but what may be an even greater help is to join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the 100,000+ subscribers on my YouTube channel! For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.

Social Security scams cost seniors millions of dollars.

These scammers have recognized a winning formula to steal your money and have doubled their efforts to get you into their trap.

I don’t want you or anyone you care about to get caught up in this. Here’s how you can avoid being victimized by this scam!

Social Security Scams Over Time

There are some scams that have a longer life than others. The most recent Social Security scam has been around since about 2017 and has started to explode. The number of those affected by this increased ten-fold in 2018 and 2019 is already on its way to being even bigger than 2018.

There’s nothing incredibly new or savvy about this scam, but it’s working better than most. That’s probably because it’s being aimed at those who count on Social Security payments to buy food, pay for utilities and other necessities.

The Scam

The phone rings, and the person on the other side tell you your social security number has been suspended, and you need to talk to them to get it straightened out. When you talk to them, they’ll have to “verify your identity” and in the process gather all sorts of personally identifiable information that will allow them to get to your money.

Currently, there are two version of this scam. Here’s how the first sounds.

“YOU HAVE RECEIVED THIS PHONE CALL FROM OUR DEPARTMENT TO INFORM YOU THAT WE HAVE JUST SUSPENDED YOUR SOCIAL SECURITY NUMBER BECAUSE WE HAVE JUST FOUND SOME SUSPICIOUS ACTIVITY. SO IF YOU WANT TO KNOW ABOUT IT…”

This sounds like a pre-recorded bot voice, not an actual person, and the computerized call will continue to tell you how to reach the “department”.

Then there’s the second version that ups the ante with the threat of arrest! The message is much like the first one, but the difference is that the voice says if you do not contact them immediately, they will issue an arrest warrant and arrest you for the suspicious activity.

Keep Yourself Safe

I understand why scams like this work. To an older generation that is not as familiar with technology, it sounds very convincing and scary!

Here are four things to remember:

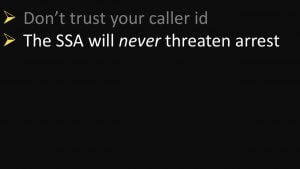

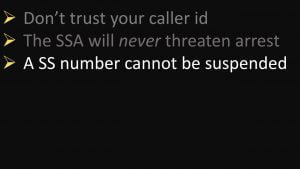

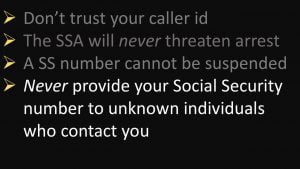

Number 1…don’t trust your caller ID! In many cases these scammers appear to be calling from the Social Security administration’s phone number. There’s spoofing technology to make it appear that way.

Second, the Social Security administration will NEVER threaten arrest.

Third, a social security number can’t be suspended for any reason that I know of. They can suspend benefit payments, but not your social security number.

Lastly, NEVER EVER EVER provide your social security number to any unknown individuals.

If you are contacted by a scammer and want to make sure everything is ok here are three ways to find out:

First, contact the social security fraud hotline to report the contact.

Second, if you just want to make sure everything is fine with your benefit payments, call the main SSA number at 800-772-1213. If you want a shorter hold time you may want to just call your local office. You can find that number at ssa.gov/locator.

You may be in the same situation I’m in where you’re pretty sure that you’d never fall for this type of scam. But you may know someone who could be more vulnerable to this. Please share this article with everyone who needs to be aware.

It’s Good To Be Proactive

You’re making a smart move by learning all you can and reading sites like these. It’s your retirement! If you know more about Social Security, and what retirement will look like for you, you will be in a better position to make sound decisions when it’s time. This is why I talk about Social Security … so you know what’s going on in the world around you.

I’d recommend staying connected with my content so you won’t miss anything. In many cases I’ll publish my newest stuff on YouTube and then share it on my Facebook page. Then my content team does their magic and cleans it up into an article for those who enjoy reading. (Again…the article is shared on my Facebook page.)

If you still have questions, you should join my FREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

Also…if you haven’t already, you should join the 100,000+ subscribers on my YouTube channel!

One last thing, be sure to get your FREE copy of my Social Security Cheat Sheet. This is where I took the most important rules and things to know from the 100,000 page Social Security website and condensed it down to just ONE PAGE! Get your FREE copy here.