If you are a minister, you have several key tax issues that makes you uniquely different from other taxpayers. These differences include the housing allowance, self-employed treatment for W-2 wage earners and the big one…the ability to opt out of Social Security.

All of these tax differences can create a great deal of complexity, and should only be handled with a team of competent tax and financial advisers. However, the ability to irrevocably opt out of Social Security is probably the most complex financial planning issue for new ministers as it carries a high degree of long-term consequence if the wrong decision is made.

If you are a new minister, I know this decision can be complicated. It’s more than just a financial decision. If you opt out, you must agree to the following language:

I certify that I am conscientiously opposed to, or because of my religious principles I am opposed to, the acceptance of any public insurance that makes payments in the event of death, disability, old age, or retirement; or that makes payments toward the cost of, or provides services for, medical care.

That’s weighty for sure, but my focus for this article is not to debate the ethical and moral issues of opting out, the good Lord knows there’s already been plenty written about that. My goal is to examine the economic aspects of opting out. Specifically, I want to help quantify what it would take to replace the benefits that you’re walking away from.

I help a lot of people with Social Security. One thing they all have in common is that they’ve called their local Social Security office at least once. Most of these calls have ended in frustration. It doesn’t have to be that way. If you know who to ask for, you’ll get the help you need.

A decent part of my living comes from consulting with individuals throughout the nation with Social Security issues. For some, it’s simply determining how their filing strategy fits in with their overall retirement plan and making sure they haven’t missed anything. For others, I help solve complex Social Security problems. Many of these people that I help would never call me if they would have received a satisfactory answer and solid advice when they called their local Social Security office. So I may be hurting myself slightly, but I can’t stand to see any more bad (and sometimes non-reversible) decisions made as a result of incorrect guidance from the Social Security Administration. I’m going to tell you who to ask for the next time you call.

In 2012 there were 2.7 million grandparents who had primary responsibility for a grandchild under the age of 18, according to a recent US Census Bureau report. Many of these grandparents don’t know that Social Security retirement benefits for dependent grandchildren is a real possibility.

Retirement doesn’t always go as expected. It hasn’t for the Causey’s. Instead of the frequent traveling they had always planned for their retirement, they are raising their young grandchildren. There’s no sense of burden though, they strongly believe it’s a privilege to have the mental, financial, and physical health that affords them the chance to offer security to their grandchildren. I admire their attitude! I hope that I would feel the same if I were placed in their situation.

Although the Causey’s had a well thought out retirement income plan, they’ve quickly discovered that the extra expense of raising kids will require them to increase their monthly cash flow.

They were surprised when I advised them to file for Social Security benefits immediately. They had always planned to wait until full retirement age to file for benefits, but that all changed when they found out that by filing for their own benefits, they would turn on Social Security benefits to their dependent grandchildren as well.

It’s not one of the more well-known benefits, but under the right conditions grandchildren (or step-grandchildren) can receive a benefit based on the work history of a grandparent.

After a life spent in the States, maybe you’d prefer the cultural heritage of Latin America, the sand of the Caribbean or the ancient beauty of Europe. Before you pack your bags, make sure your selected destination is one of the countries where you can still receive your Social Security benefit.

The rules are incredibly complex for those who are eligible for Social Security benefits, but are outside of the United States. These rules apply not only to those who plan to move, but could apply to someone who was on a missions trip or extended vacation.

For the purposes of this article, we’ll limit our discussion to US citizens who have lived and worked in the United States and decided to retire overseas (or extensively travel) during their retirement years.

The Social Security Administration makes it clear. If you are a US citizen, you can receive your Social Security benefits if you are outside of the United States. As you may suspect, there are some stipulations.

Just how much you owe in tax on Social Security benefits can be a huge shock if you’re unprepared.

I vividly remember the fact that the amount of tax on Social Security benefits was one of my Dad’s biggest retirement surprises.

He didn’t expect to pay so much in taxes, so in his first year of retirement (and first year claiming his benefits) it came as a nasty surprise when he found out that up to 85% of his Social Security benefit could be counted as taxable income!

My dad wasn’t alone. A lot of retirees have no idea of the big tax bill that could be waiting for them in their first spring after retirement.

What to Expect from Taxes on Social Security Income

Ultimately, in my dad’s situation, we were able to mitigate some of his tax burden. But for a good part of it, he was stuck.

As you can imagine, he didn’t like this one bit. And you might not either if you find yourself in the same position.

Every year individuals retire and are faced with sticker shock when they find out how much they’ll have to pay in taxes on Social Security income.

To some, it doesn’t seem fair. You’ve worked for years and paid your Social Security tax as the admission ticket to a Social Security benefit.

Now that you’re collecting that benefit, you have to pay taxes? Again?

Taxes on Social Security Income Are a Relatively New Thing

At first, Social Security benefits were not taxable. That all changed with the passage of 1983 Amendments to the Social Security Act.

Under this new rule, up to 50% of Social Security benefits became taxable for certain individuals. 10 years later, the Deficit Reduction Act of 1993 expanded the taxation of Social Security benefits.

Under this Act, an additional bracket was added where up to 85% of Social Security benefits could be taxable above certain thresholds.

The combination of these laws left us with the current tax structure on Social Security benefits. Today, somewhere between 0% and 85% of your Social Security payment will be included as taxable income.

Since those brackets have been added, they’ve never been changed! As far as I know, there are no plans to change them in the future. This means that as the general income levels rise, more individuals will be subject to taxation on their social security benefits.

For proof of this, look at what’s already happened. Since taxes on SS benefits were introduced, the revenue coming in from these taxes have skyrocketed. Here’s an example: In 2008, taxes were slightly above 15 billion dollars. In 2017, this amount was 130% higher!

How to Know How Much of Your Benefit Is Subject to Taxes

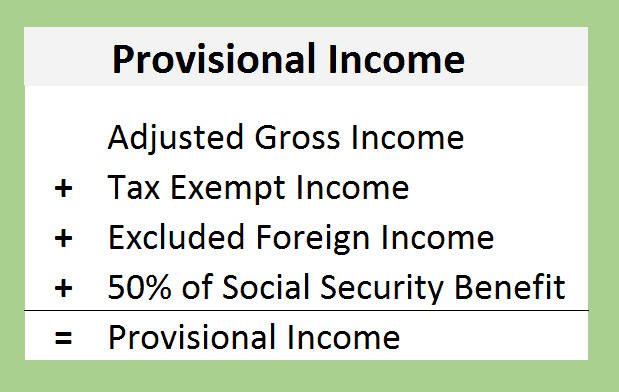

In order to determine how much of your Social Security benefits will be taxable, you first have to calculate “combined income.”

I’m not a tax professional, but to my knowledge, the only place this term is found is when it relates to Social Security benefits. It’s a formula by which the IRS determines how much of those benefits you receive should be included as ordinary income on your tax return.

Combined income can be roughly calculated as your total income from taxable sources, plusany tax-exempt interest (such as interest from tax free bonds), plus any excluded foreign income, plus50% of your Social Security benefits.

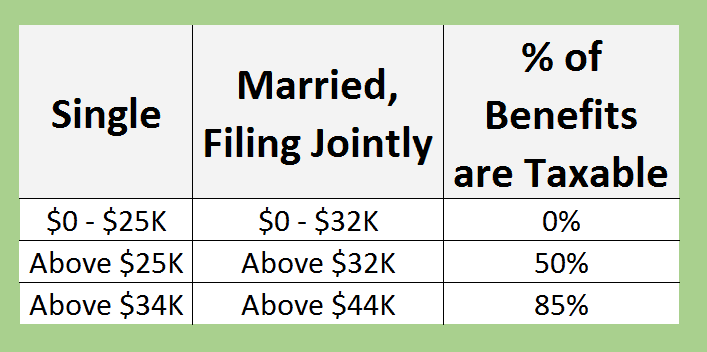

Once you’ve calculated your “combined income” you can apply it to the threshold tables to determine what percentage of your Social Security will be included as taxable income.

If your total “combined income” is less than $32,000 (or $25,000 if you’re single), none of your Social Security benefits will be taxable.

However, if you are married and your total combined income exceeds $32,000 (and $25,000 for singles), then 50% of the excess is the amount of Social Security benefits that must be included in taxable income.

If your combined income exceeds $44,000 (or $34,000 for singles), then 85% of the excess amount is included in income.

An Example of How Combined Income Calculations Work

That can seem really confusing when we’re just talking about things in theory. Let’s look at a more tangible example so you can better understand how taxes on Social Security benefits are calculated.

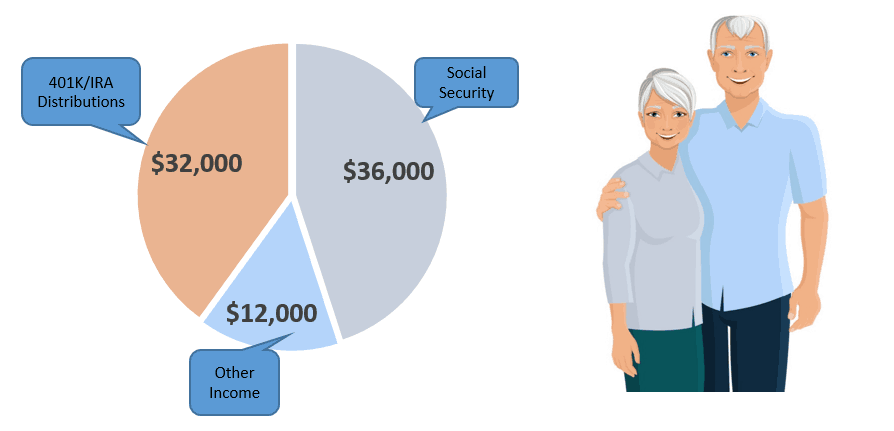

Imagine that Tim and Donna have recently retired. They have some rental property that generally averages $12,000 in net annual income.

Their combined Social Security benefit will be $3,000 per month, which equals $36,000 per year. In addition to this income, they will take an annual distribution from their IRA in the amount of $32,000.

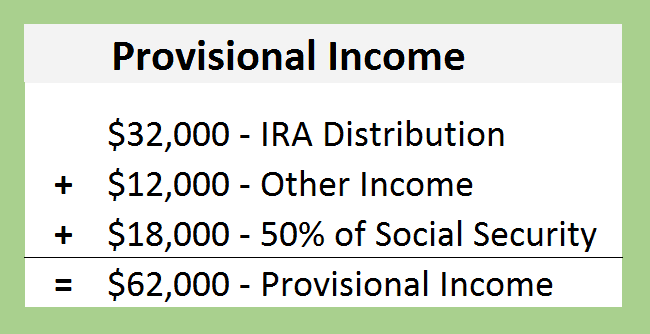

Using the income from those sources, here’s how the combined income would be calculated — and remember that only half of the Social Security income is counted in the calculation:

From this, we can see that Tim and Donna have $62,000 worth of combined income. From here, we can see how much of their Social Security benefit is taxable.

How Your Combined Income Impacts the Tax You Pay on Social Security Benefits

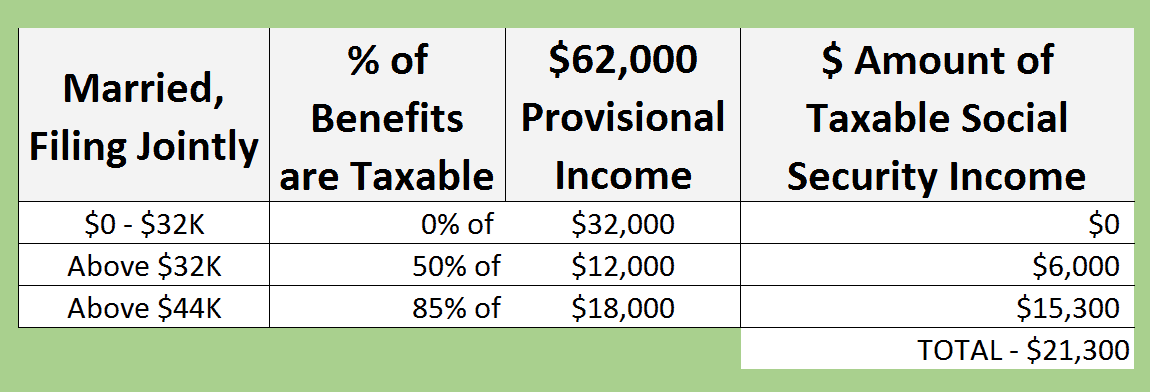

Based on a married couple with a combined income of $62,000, we can return to the thresholds to determine how much in tax on Social Security benefits they might fact.

The first $32,000 of combined income has no impact on whether or not a Social Security benefit is taxable. 50% of the amounts between $32,000 and $44,000 will be added and then 85% of the amount in excess of $44,000 will be added.

As a rough calculation, a married couple with a combined income of $62,000 would have about $21,300 of taxable Social Security income:

Since you can only spend the dollars you keep, you need to be familiar with the rules about when and how much you may pay in taxes on Social Security benefits.

You don’t have to be a tax expert; I know I’m not. But I do understand enough to know how to roughly calculate the amount of tax on Social Security benefits — and you should too.

If you need to dig deeper and get specific advice on your situation, please consult your tax advisor or CPA.

Need More Information on Social Security?

If you still have questions, you could leave a comment below, but what may be an even greater help is to join myFREE Facebook members group.

It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the 326,000+ subscribers on myYouTube channel! For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing that you don’t want to miss: Be sure to get your FREE copy of mySocial Security Cheat Sheet. This handy guide takes all of the most important rules from the massive Social Security website and condenses it all down to just one page.

Not too long ago, I saw a participant in the Texas ORP make a massive mistake.

Texas ORP is the Texas Optional Retirement Program. It’s something that, when initially hired, teachers can choose to opt into. Alternatively, teachers may be able to choose the Teacher’s Retirement System (TRS) instead.

This is a big decision if you have the choice, because you only get once chance to make it.

Most teachers are automatically enrolled in TRS. However, certain employees of public colleges are eligible to choose the Texas ORP instead of the TRS pension plan.

Although both of these accounts are meant to be for retirement savings and income, they each approach this goal using two distinctly different paths.

I’ll tell you more about the teacher who made a simple little move — on the recommendation of her financial advisor! — within Texas ORP that cost her thousands of dollars. She’s not the only one I’ve seen make this mistake, either.

But first, let me explain a little bit more about both programs and how they work.

“The Optional Retirement Program (ORP) is available as an alternative to the Teacher Retirement System (TRS) for full-time faculty, librarians, and certain administrators and professionals employed by Texas public institutions of higher education.”

Essentially, certain higher-education employees can opt out of the Teachers Retirement System in favor of a plan that allows them to make their own contributions and get a match from their employer.

The dollars in the Texas ORP can be invested in a variety of ways. On the surface it works much like a 401(k) or some other employer sponsored retirement plan. This intent of creating this plan was to give these employees a choice of how they saved for their retirement needs.

The Difference Between Texas ORP and TRS

TRS is a defined benefit program, whereas the ORP is a defined contribution program:

A defined benefit plan, like TRS, specifies the benefit that will be payable to you on a monthly basis when you retire. This amount is based on a formula that includes factors such as years of service and average salary.

A defined contribution plan, like the ORP, specifies what percentage or dollar amount of your paycheck is withheld and saved in an investment account. In addition to your salary deferrals, your employer will often match your salary up to certain limits. The amount you have in this plan at retirement is not set. It is usually determined by factors such as investment performance and how much you saved in the plan. The ORP falls under this category.

The TRS plan is set up to provide you a specified income stream in retirement. The ORP, on the other hand, is set up to provide you an unspecified lump sum at retirement.

How Do You Decide Between the ORP and TRS If You Have the Choice?

The obvious follow-up question here is, which program is better for you if you have the ability to choose between them?

The Texas Higher Education Coordinating Board, like most states, takes a hands-off approach to recommending one plan over the other. In their handout “An Overview of TRS and ORP,” they suggest you talk to your employee benefits office or your authorized ORP company representative.

But you need to beware. Your employee benefits office is not going to give you specific advice on choosing a plan. This leaves you with one suggestion for help on this decision: your authorized ORP representative.

And that’s a problem, because this “ORP representative” is usually an investment or insurance salesperson. They get paid only if you choose to enroll in ORP instead of TRS. Do not expect unbiased advice.

Many of these ORP providers are from insurance companies who use products with heavy fees and heavier advertising language. Consider this language from one of the larger authorized ORP providers in Texas:

“The Texas ORP gives you the significant advantages of portability, tax deferral for contributions, interest and earnings and flexible investment options.”

That statement is problematic for me. Why? First, none of those “significant advantages” are all that significant. Second, most financial services companies like this have gotten really good at changing the retirement equation.

Over time, they’ve used some great marketing to convince individuals that retirement planning should be about accumulating a lump sum amount. The idea is that this lump sum amount will be able to generate an income for retirement.

The problem is, it takes a large lump sum to generate the same income you could receive from a pension like TRS. For this reason I usually recommend TRS over ORP. For retirement income purposes, I simply can’t make the numbers work in favor of the ORP.

How the Math Works When You Compare TRS and ORP

Here’s an example of how the math works out. For this story, we’ll talk about a fictional set of teachers named Mich and Katie, and we’ll use the contribution rates currently used in Texas.

Mitch and Katie began teaching at a Texas university on the same day in 2016. They each started with a salary of $45,000 per year.

With funding shortfalls, they figured they could only expect an average cost of living increase of 1% per year throughout their career. Both of them planned to work for the next 30 years until they would be age 65.

After weighing their options, they each came to a different conclusion about which plan would best fit their retirement needs. Mitch chose the Optional Retirement Plan. Katie’s choice was to participate in the Texas Teacher’s Retirement System.

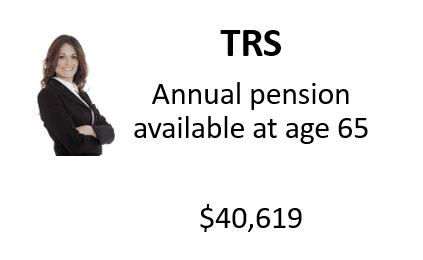

Katie wanted to work and enjoy life. The thought of managing investments did not appeal to her. After running her numbers she calculated that her pension amount would be approximately $40,619 per year.

Since she was conservative, she didn’t see how she would ever beat that with an investment portfolio on her own.

But Mitch was different. He loved the idea of a little risk and controlling his investment options. His thought was that he should be able to substantially increase his retirement income by managing his own portfolio.

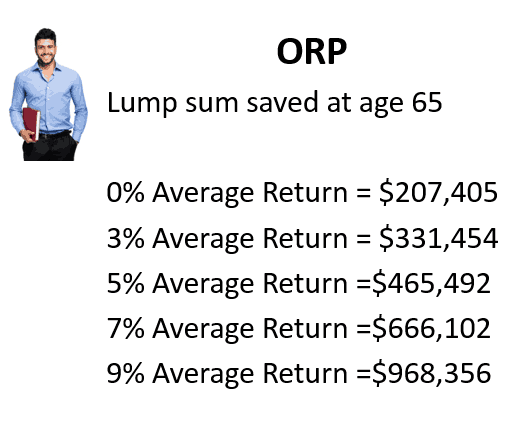

He ran a hypothetical future value calculator that showed he could grow his account to nearly a million dollars if he could achieve an average annual return of 9%!

It’s hard to argue with nearly a million dollars, but here’s the important question:

How much retirement income could he expect if he would have actually averaged a 9% rate of return?

It’s not as much as you think.

A Quick Side Note on the 4 Percent Rule

Many financial planners follow what’s called the “4% rule.” This rule says that if you withdraw 4% of your retirement savings each year, and adjust for inflation, your money should safely last 30 years.

Using the 4% rule rule, Mitch could expect $38,734 in his first year of retirement. The first thing to notice is that he is not even getting the amount of income that Katie is receiving. It’s also assumingthat everything goes right for him!

The fact is, Mitch probably wouldn’t even get that amount of income. The big flaw in the calculation is the same flaw that your ORP company representative will probably repeat.

Here it is: You’re not going to get a 9% return! Sure, the total stock market has averaged that over the past 30 years… but you’re not the market. You’re an investor like me.

We have emotions and occasionally make irrational decisions about our investments, usually at the worst possible time. If you don’t believe me, look at this study by Dalbar.

They found that the 20-year return for the average mutual fund investor was 5.19% (over the same period the stock market averaged 9.85% annually).

Even if you’re more disciplined than the average investor, you still have to consider the performance drag from investment and management fees. If you are using annuity products, which are really popular in these plans, these fees can get really high! I’ve seen them as much as 3% per year.

So what can you expect as an annual rate of return if you choose the ORP? Personally, I wouldn’t project much more than a 5% average annual return.

While that would still leave you with a substantial $465,492 at retirement, it simply could not safely produce the same amount of income as the teacher’s retirement pension. In fact, your income would be cut in half!

Using the same “4% rule,” you could only generate approximately $18,619 in annual income. That’s a long way from the $40,619 that Katie will receive.

If you’re in the middle of choosing between ORP and TRS, you may want to consider going with TRS.

But what if you’ve already made your choice, and you’re stuck with ORP? Don’t despair! Your retirement may not be in jeopardy… but you need to avoid making the big mistake the teacher at the beginning of this article that I was telling you about made with hers.

Watch Out for Social Security Reductions…

Many employees of Texas colleges do not pay Social Security taxes. If they have never paid this tax at a prior job, they are not eligible for a Social Security benefit.

But many of these employees have worked in other jobs where they have paid these taxes and earned the required 40 quarters for Social Security benefit eligibility.

In a situation where there are both covered (Social Security taxes paid) and non-covered (no Social Security taxes paid) earnings, the Social Security Administration has some funny rules about how they reduce benefits.

I won’t use the space this article provides to go into a full discussion of the Social Security rules, but you should learn more about the Windfall Elimination Provision (WEP).

The Basics of the WEP is that your benefit can be reduced by up to $413 (for 2015) every month if you held a job where you did not pay Social Security tax.

…And Avoid That BIG Mistake

Now, on to that big mistake that I’ve seen so many teachers make. It’s not due to how the funds are invested, but in what happens when the funds begin to be distributed.

For those workers who are also eligible for Social Security, there is often a blanket assumption that those benefits will automatically be subject to the reduction from the Windfall Elimination Provision.

That’s just simply not true.

You can get a Social Security benefit that is not reduced by the Windfall Elimination Provision into your early 70s if you avoid the triggering events.

The Social Security Administration has a great piece on Texas ORP and Social Security on their website. The rules found there on how the Texas ORP triggers the WEP can be boiled down to these points:

The trigger for the WEP reduction does not occur until you become entitled to benefits from your Texas ORP.

Entitlement does not occur until you take a distribution

For purposes of the WEP trigger, a distribution is

A rollover of any type

A lump sum distribution

Periodic Payments

Distributions are required no later than April 1 of the year following the year you attain age 70 1/2.

So, as long as you don’t meet the triggers, you are not “entitled” to your Texas ORP and thus are not subject to the Windfall Elimination Provision.

This could mean several years of a Social Security benefit with no reduction.

Here’s how those rules apply in real life.

$46,000 More?

Depending on when your birthday falls, on average, you have 113 months between your age 62 and April 1st of the year following the year you attain age 70 1/2.

The current maximum WEP reduction is $413 per month. You could file for Social Security benefits at age 62 and have all those months with no deduction as long as you don’t become “entitled” to your Texas ORP.

That could mean an additional $46,000 in Social Security benefits ($413 per month x 113 months). I should point out that those figures do not include increases from the cost of living adjustment.

For some, this may not be an option. It’s possible that you will rely on the income created by these savings to provide your retirement income.

However, some strategic retirement income planning may allow you pull income from other sources and eliminate the need for touching those Texas ORP dollars until you are required to take a distribution.

Remember that your Texas ORP account can stay where it is when you retire. If your financial advisor tells you that you need to do a rollover (or anything else) with your Texas ORP, be very inquisitive. There could be $46,000 at stake.

Have More Questions?

If you still have questions, you could leave a comment below, but what may be an even greater help is to join myFREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the 100,000+ subscribers on myYouTube channel! For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing that you don’t want to miss: Be sure to get your FREE copy of mySocial Security Cheat Sheet. This handy guide takes all of the most important rules from the massive Social Security website and condenses it all down to just one page.

Social Security Overpayment letters are becoming more common.

For those who depend on Social Security payments, receiving a Notice of Overpayment is no fun. These notification letters will often show up after a change in income or family status and generally allege that the Social Security Administration has paid you too much money. In this letter they offer you a 30 day window to repay the benefits.

This leaves many shaken who count on this income to buy their groceries or some other necessity. Fortunately, the Administration is often incorrect in their calculations.

However, there is still a process to follow if you receive one of these letters. Unless otherwise stated, you have three options.

The definition of marriage has always been a hot topic. In the past several years, we’ve seen more and more court cases and news debating this, and as a result, more people from this community have been wondering:

What about the impact of common-law marriages and Social Security benefits? How do these types of relationships get classified in the eyes of the Social Security Administration?

Let’s take a look at the topic today so you can fully understand how Social Security benefits and common-law marriages go together.

The Social Security Administration’s Rules on Common-Law Marriages

The Social Security Administration is not known for their simple, plain language in most cases. So you might be surprised to learn that when it comes to common-law marriages and Social Security benefits…

The rules are actually quite straightforward! According to the SSA, a common-law marriage is a valid marriage. And as such, a common-law couple will be able to claim the same benefits as a couple who followed the “traditional” marriage route.

Common-Law Marriages Are Entitled to the Same Benefits As “Traditional” Marriages

The Social Security benefits you receive as a common-law marriage couple include spousal benefits, survivor benefits and even benefits from an ex-common law spouse.

While that part of the rule is straightforward, there is a bit of a catch: meeting the requirements of a common-law marriage.

These requirements are not as easy as some may think to achieve. Many people incorrectly assume that a common-law marriage is sealed after a certain time period of living together, but it’s not always so simple.

What Qualifies as a Common-Law Marriage?

To make sure I fully understood the rules before sharing them with you, I reached out to my friend Lisa Shoalmire.

Lisa is well-versed in the rules around common-law marriages and how the SSA sees these relationships. Here’s what she told me:

“Generally, the Social Security Administration will recognize a common-law marriage as valid if the following requirements are met:

First, the common law marriage must be contracted in a state where common-law marriages are recognized. Less than half of the fifty states recognize [these relationships as legally binding].

In states that do recognize common-law marriage, usually the parties must live together and hold themselves out to the public as husband and wife. The cohabitation does not have to be in the State where the marriage agreement was made.

Second, there must be an agreement to marry. This agreement must:

Propose a permanent union that is exclusive

Be in the present tense

Propose a marital status that cannot be terminated at will but can be terminated only in the same manner as a “traditional” marriage, i.e., death, divorce or annulment

Third, the marriage must be entered into by mutual consent of the couple to become husband and wife from that time forward.

Finally, both individuals must be legally capable of entering into a valid marriage such as having the mental capacity to marry or not otherwise be legally married to someone else at the time of entering into the common-law marriage.”

Lisa went on to tell me that many have assumed they were in a common-law marriage, but often find out otherwise when the relationship ends or a death occurs.

If you have questions about the validity of your marriage, you need to see an attorney who can help with this. To find one near you, visit LegalMatch.

What You’ll Need for Social Security Benefits in a Common-Law Marriage: Proof of Marriage

Let’s say you believe you meet all of the requirements for a common-law marriage. What do you need to have in order to apply for Social Security benefits?

The Social Security Administration mandates that you must provide evidence of your marriage. Evidence to prove a common-law marriage in the States that recognize such marriages must include:

A statement from each spouse and a statement from a blood relative of each, if both spouses are living, OR

If either spouse is deceased, you will need a statement from the surviving widow or widower and statements from two blood relatives of the decedent, OR

A statement from a blood relative of each spouse if each individual has passed away.

For more information, see the language on proving eligibility for a common-law marriage in the Social Security Handbook here.

Note that the Social Security Administration will also ask you to attach evidence that confirms that you had a common-law marriage, such as mortgage/rent receipts, bank records, insurance policies, and so on.

Don’t Forget: The Rules May Vary, Depending on Your State

It’s important to note that the rules in each state vary greatly on what is required to have a recognized common law marriage.

Since the Social Security Administration takes its lead from individual state law when determining benefits eligibility, it’s important to understand where the individual states differ.

If you still have questions, you could leave a comment below, but what may be an even greater help is to join myFREE Facebook members group. It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the 100,000+ subscribers on myYouTube channel! For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing that you don’t want to miss: Be sure to get your FREE copy of mySocial Security Cheat Sheet. This handy guide takes all of the most important rules from the massive Social Security website and condenses it all down to just one page.

If you are planning for retirement, and have prior marriages, it’s critically important to fully understand the rules around Social Security divorced spouse benefits.

Divorce is difficult. Though I’ve never personally been through it, I’ve watched as dozens of my clients and friends have gone through the process.

From my side of the desk, I’ve yet to see a single divorce where either spouse emerged with a higher net worth after the split. Everything changes.

The change brought on by divorce requires major adjustments to your financial plans for the future. One of the most important things you’ll need to do is adjust your plans for retirement. Now you may not have the income to continue saving at your prior level, but you probably won’t need as much to fund your lifestyle in retirement. All of this is up to your individual wishes, goals, and dreams. But one thing is for sure…if you are over 50 you need to plan on part of that retirement being funded by Social Security.

So before you sit down with your financial planner to rethink your retirement income strategy, let me explain more about how Social Security benefits for a divorced spouse actually works and why you need to know.

Are There Social Security Benefits for a Divorced Spouse?

Will Your divorce impact your ability to file for Social Security? There’s some good news to start. What divorce may not impact is your ability to file for Social Security on your ex-spouse’s record.

All you need to do is meet the qualifications. The basic rules are that:

Your marriage must have lasted at least 10 years*

You must be 62 or older (60 if they are deceased)

That’s pretty much it — but if we stop there, we’re only telling part of the story about how Social Security divorced spouse benefits work. Let’s take a closer look.

*Note: While divorced spouse benefits do require a 10 year length of marriage (where the final divorce became final on or after the 10th anniversary of the marriage), the rules say that if that 10 year period was ‘interrupted’ by divorce, the marriage still qualifies provided the remarriage took place no later than the calendar year immediately following the calendar year of the divorce.

For example, Steve married Rebecca on 6/15/2000 and divorced 5/15/2003. On 9/7/2004, they remarried but divorced again on 8/5/2010. This scenario would satisfy the 10-year requirement even though there weren’t married for the entirety of the 10 year period.

The 10 year marriage rule simply looks to see if the total marriage lasted for 10 years and if it was in existence at some point in each year of the 10 year period.

How Social Security Divorced Spouse Benefits Work, Depending on Your Circumstances

The spousal benefit rules for married individuals require the higher earning spouse to file first before a spousal benefit can be paid to a lower earning spouse.

But that’s not how it works with divorce cases. You can collect on your ex-spouse’s record even if he or she hasn’t applied for benefits!

There are some caveats, though. You must have been divorced for at least two years and your ex-spouse must be eligible for benefits, and typically this means that your ex must be at least 62 years old.

If you’ve met the length of marriage rules, and your ex-spouse is still living, you are eligible for the greater of:

your own benefit, or

up to 1/2 of your ex-spouse’s full retirement age benefit.

Here’s an example:

Your ex-spouse has a full retirement age benefit amount of $2,000. Based on that alone, you could expect to receive $1,000 spousal benefit at your full retirement age.

However, the actual amount you receive may be less, based upon the age that you file for benefits.

Depending on how old you are when you file, the spousal benefit amount will range between 32.5% and 50% of the higher-earning spouse’s full retirement benefit.

So, if a spousal benefit is the highest benefit that you are entitled to, there is usually not a good reason to delay filing beyond your personal full retirement age.

And remember: if you are divorced, and your ex-spouse has not yet filed for benefits, you must have been divorced for at least two years before you can claim benefits based on your ex-spouse’s history.

Filing for Benefits When You’ve Had Multiple Marriages, Or Your Ex-Spouse Is Deceased

Social Security rules say that as long as all marriages have ended, you are not currently married, and you’ve met the length of marriage rules, you can choose the highest benefit from any of your ex-spouses.

If circumstances change — perhaps an ex-spouse passes away — then you could switch from a spousal benefit on one spouse to a survivors benefit on another.

If your deceased ex-spouse was the higher income earner, your benefit would be equal to his or her full benefit, minus any reduction for your age. (You can file for a survivor benefit as early as age 60.)

Before you do this, however, be warned: If you remarry prior to age 60, you lose the right to claim on an ex-spouse’s record, at least until the subsequent marriage(s) end in death or divorce.

If you remarry after age 60, you are eligible to receive benefits based on the highest of your benefit, your current spouse’s benefit, or your deceased spouse’s survivor benefit.

If You Want to File for Benefits on Your Ex-Spouse’s Record, Use This Special Strategy to Yield Higher Benefits

Don’t grab your keys and head off to your local Social Security office just yet. Just because you can file on your ex-spouse’s benefit doesn’t mean that you should.

At the very least, you need to know your options about some filing strategies that could drastically increase the amount of cash flow and lifetime benefits you could receive.

If your ex-spouse is deceased, you have met the length of marriage rules, and don’t exceed the income limitation, you could file a restricted application for a survivor benefit as early as age 60 and switch back to your own benefit at full retirement age or later.

Here’s an example to illustrate how this works:

Let’s say that Karen has her own Social Security benefit available of $2,000 at her full retirement age of 67. Currently she’s 62, and is also eligible for a survivors benefit of $1,300 today.

She could file for only the survivors benefit and let her benefit increase with delayed retirement credits. At age 70, she could switch back to her own benefit which would have grown to $2,480 (not including cost of living adjustments!).

This strategy is only available for those eligible for a survivors benefit — but if you qualify, it can help you reap big rewards in attaining more retirement cash flow.

Don’t Expect the Social Security Administration to Tell You This

The rules for Social Security benefits for former spouses are pretty generous, and the program can provide much-needed income during retirement years. Making sure that you understand the rules is key to receiving the maximum benefit to which you are entitled.

The amount of benefits you, or your survivor, will receive can often hinge on how much you know! But don’t expect the Social Security Administration to look at all of your prior marriages and make a determination about which eligible benefit is best for you.

They make it pretty clear…proving that there are eligible benefits from prior marriages is the responsibility of the claimant.

Unless you know the rules, it’s pretty easy (and common!) to miss benefits from a prior marriage.

Adding to the challenge is that once you are divorced, the Social Security Administration stops sharing information about your ex-spouse’s benefit amount with you.

That’s great for privacy but bad for obtaining information and planning. However, if you ask them specific questions, they will answer.

At least now you know that you need to dig into the rules and figure out your options before you make a filing mistake — but you could still be concerned that you might miss out on benefits.

In that case, if you still have questions you could leave a comment below… but what may be an even greater help is to join my FREE Facebook members group.

It’s very active and has some really smart people who love to answer any questions you may have about Social Security. From time to time I’ll even drop in to add my thoughts, too.

You should also consider joining the 330,000+ subscribers on myYouTube channel! For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing that you don’t want to miss: Be sure to get your FREE copy of mySocial Security Cheat Sheet. This handy guide takes all of the most important rules from the massive Social Security website and condenses it all down to just one page.

Katie wanted to work and enjoy life. The thought of managing investments did not appeal to her. After running her numbers she calculated that her pension amount would be approximately $40,619 per year.

Katie wanted to work and enjoy life. The thought of managing investments did not appeal to her. After running her numbers she calculated that her pension amount would be approximately $40,619 per year.