The Social Security age of retirement used to be straightforward and the same for everyone. Not anymore.

From the first Social Security Act back in 1935 through 1983, the full Social Security age of retirement was 65. Then things got a little confusing. Due to the 1983 Amendments to the Social Security Act, the full retirement age began to gradually increase from age 65 to 67. However, it took 22-years to adjust! It slowly increased from 65 to 66, stayed at 66 for 11 years, and then began to move slowly to 67.

Whew! No wonder everyone is confused about their Social Security age of retirement.

Thankfully, these changes have mostly worked themselves through the system and now the full retirement age is based on your year of birth.

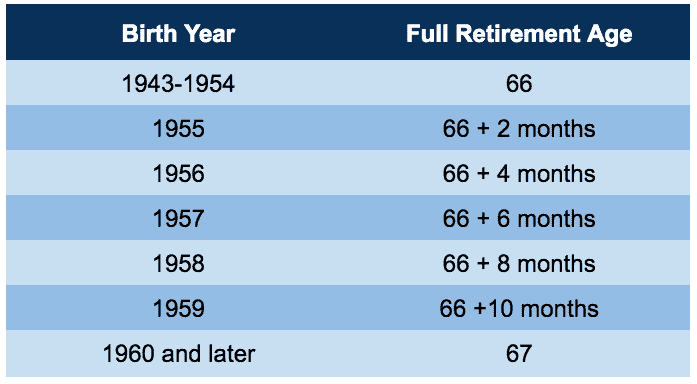

Here’s how it works by birth year:

- Full retirement age 1943 – 1954: 66

- Full retirement age 1955: 66 and 2 months

- Full retirement age 1956: 66 and 4 months

- Full retirement age 1957: 66 and 6 months

- Full retirement age 1958: 66 and 8 months

- Full retirement age 1959: 66 and 10 months

- Full retirement age 1960: 67

The one exception to these dates is if you were born on the first day of the year. In that case, the SSA deems you to have been born in the year prior. For example, if your date of birth is Jan 1, 1960, the SSA will count your year of birth as 1959. This means that an individual would be able to receive his full benefit 2 months earlier than anticipated.

Although it’s only a small segment of the population who is affected, this “day before” rule can change a retirement strategy.

Why Your Social Security Age of Retirement Really Matters

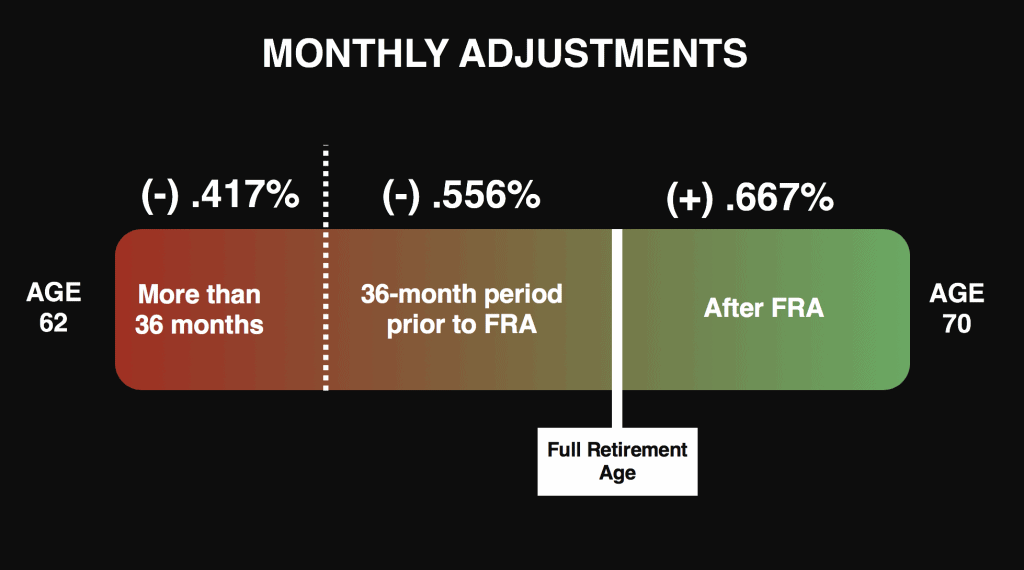

Understanding at which age you attain full retirement age is important because this is when you qualify for 100% of your Social Security benefit. If you file before this age your benefit will be reduced. If you file after this date, your benefit may be increased.

The increases and decreases are commonly thought of as occurring on an annual basis, but they are actually calculated on a monthly basis.

Currently, the reductions are calculated as follows:

- .555% Monthly Decrease – During the 36 month period prior to FRA

- .417% Monthly Decrease – Greater than 36 months prior to FRA

If you file after your designated full retirement age, benefits are increased by .667% for each month you delay (until age 70). These increases are referred to as “delayed retirement credits” by the SSA.

It’s important to understand that there are differences between how the increases and reductions are applied.

If you file at any time before your full retirement age, your benefit will be calculated by these reduction amounts and immediately reduced beginning with your first check.

That is not the case for the increases.

In the SSA manual, you can see there are three triggers for adding delayed retirement credits to a retirement benefit:

- The month you attain age 70

- In January of the year following the year you earned the delayed retirement credits

- The month you die (for calculating the survivor’s benefit)

To dive a little deeper into how the delayed retirement credits are added, you should read my article, The Delay of Delayed Retirement Credits.

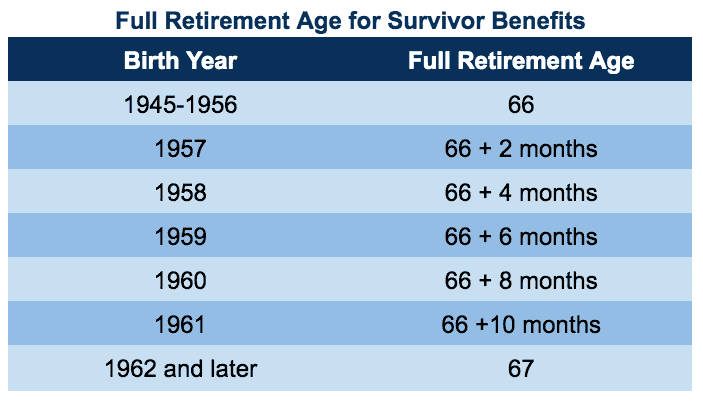

How the Social Security Age of Retirement is Different for Survivor’s Benefits

One commonly overlooked provision in the rules is that the Social Security age of retirement is different for those who are eligible for survivor benefits. When you compare the two, you’ll see that there is a two-year difference in the table of full retirement ages.

How the Social Security Age of Retirement Affects the Future of Social Security

For the past several years, there have been multiple proposals submitted which would increase the full retirement age. Based on the statistics alone, increasing the age for full benefits seems to be a reasonable plan. It hasn’t been adjusted since 1983, but life expectancies continue to increase. This means that the system has to make more payments to each person than in the past and more payments mean the Social Security trust fund becomes depleted even faster.

But, as with any system with this many moving parts, there are some unintended consequences to increasing the full retirement age.

For example, if the full retirement age is increased, the benefit amount for those who file early would be cut. This is simply because reductions are calculated on a monthly basis. If the age is increased, but the early age is still 62, there would be more months between when you file for benefits and your full retirement age. More months equal more reductions.

The fix for this is to change the early Social Security age of retirement. But this scenario could incentivize more people to file for disability benefits instead — because they’re not reduced based on the age at which you file. This would mean that the Social Security system could have an even bigger issue with funding than it’s currently facing!

There are lots of little things to consider when thinking about changing the age of retirement benefit eligibility. For a deeper examination of those considerations, see my article The Unintended Consequences of Increasing the Full Retirement Age for Social Security Benefits.

How To Get Every Dollar In Benefits You’ve Earned

Understanding the Social Security age of retirement is the first step in mastering your retirement. Just keep in mind…this is YOUR retirement we’re talking about here. Continue to learn and educate yourself. It’s the best way to increase your odds of an awesome retirement.

I’ve created a number of resources to help you do that. For starters, you can download my Social Security cheat sheet. It’s completely free and packed with information that I’ve distilled from thousands of government website pages.

Also, if you haven’t already, you should join the nearly 400,000 subscribers on my YouTube channel. I’ll be creating more content around developments in Social Security to keep you informed. If you’re subscribed with notifications turned on, you’ll know as soon as I release a new video. See you there!

[…] your full retirement age is dependent on your year of birth. For anyone born in the years 1943 and 1954, the full retirement age is 66. If you were born […]