Trying to plan for your retirement — but can’t understand the complicated rules for calculating Social Security benefits when you have your own benefit and a spousal benefit?

You’re not alone! Most people find this really perplexing…

…and when you add in a spouse that’s affected by the Government Pension Offset (GPO) and Windfall Elimination Provision (WEP) to the mix, the rules become even more tangled.

If you have a scenario where both spouses are subject to these rules, it can really seem like the convoluted rules are setting you up to fail! In a case like this, it can mean that one spouse could be forced to have their Social Security benefit calculated with the dual penalties from both the WEP and GPO (at the same time!)

This application of both of these rules is not necessarily a “double penalty,” but rather a separate type of penalty on each of the separate benefits.

Don’t worry if it all seems hopelessly confusing. I’ll explain all of this below.

All of these issues occur when one spouse is “dually entitled” to benefits. This simply means that the lower-earning spouse’s total benefit will be made up partially from their own benefit plus an additional amount as a spousal payment.

This happens when someone has their own benefit, but it’s less than half of the higher earner’s Social Security benefit.

This creates a dual entitlement because the Social Security Administration would pay the worker their own benefit first, and then finish it out with a spousal payment. This would be treated as two separate benefit payments for the purpose of age-based reductions and increases, and special rule applications.

Before we move on into how the GPO and WEP affects dually entitled spouses, lets cover a quick refresher on the concept of dual entitlement for spousal benefits. Then, we’ll dig into the nuance of how the GPO and WEP change things and look at a few examples of how this works in cases where only one spouse is affected and where both spouses fall under these rules.

Social Security Spousal Benefits and Dual Entitlement

The spousal benefit rules guarantee that if the lower-earning spouse files for Social Security at full retirement age, they will not receive less than half of the higher-earning spouse’s full retirement age benefit.

Here’s an example to show how this works: Let’s assume we have a couple where the husband paid into Social Security over his career as a self-employed electrician. The wife managed the books of the business, but was never technically an employee and did not pay into Social Security.

At full retirement age, the husband has a monthly Social Security benefit of $2,000. Because the wife did not work in a role that allowed her to earn the required 40 credits for Social Security benefits, she won’t have a benefit of her own.

However, as an eligible spouse, she’d be eligible for a benefit valued at half her husband’s benefit, or $1,000 per month. That’s through the qualified spousal payment at her full retirement age. (If she filed for that benefit early, the number would be reduced based on her age.)

If we change this scenario slightly, we can see where the dual entitlement provisions come in.

Let’s now assume the wife did have a small benefit of her own from a prior job. The husband still has a full retirement age benefit of $2,000 per month — but now the wife has her own benefit of $800 per month, too.

Remember, at full retirement age, the lower-earning spouse can get the greater of their benefit or half of the higher-earning spouses’ benefit. In this case, the wife can still have a total benefit of $1,000 — but, she’ll receive her own benefit of $800 first and then a “spousal payment” of $200 to get her to the full $1,000 she is eligible for.

This is the perfect example of a dually entitled spouse: the wife in this scenario is entitled to a benefit she earned through her own work, plus a second payment through spousal benefits to catch her up to the total Social Security benefit she is entitled to receive.

The important thing to understand with dual entitlement is that these are really two separate benefits all rolled into benefit payment. The easy way to understand how this may apply is a simple formula:

Half of Higher-Earning Spouse FRA Benefit

– Lower-Earning Spouse FRA Benefit

= Spousal Payment

Using this formula, if we go back to the husband and wife in our example, we know that half of the higher earner’s benefit amount is $1,000. We can then subtract the lower earner’s benefit amount of $800 to see what the spousal payment would be: $200

To complete this calculation and determine a final benefit payment, all that’s left is to reduce or increase the benefit payments based on your filing age. (For a full conversation on the actual age-based calculations, see my article Calculating Spousal Benefits with Dual Entitlement).

Dual Entitlement When Facing the Government Pension Offset or Windfall Elimination Provision

When you add the GPO & WEP rules to the dual entitlement calculations, things change a little. But once you get past a few differences, it isn’t radically different than someone who would file without the GPO or WEP.

The WEP rules are often confused with the GPO, so it’s important to understand the differences.

The Windfall Elimination Provision: Only applies to individuals who are entitled to a Social Security benefit based on their own work history AND have a pension from work where they did not pay Social Security tax.

The Government Pension Offset: Only applies to individuals who are entitled to a Social Security benefit as a survivor or spouse AND have a pension from a federal, state or local government employer where they did not pay Social Security tax.

Before we move on, there are a few basic terms you should know:

- Windfall Elimination Provision (WEP): This rule reduces a worker’s own Social Security benefit amount from work that they have performed.

- Government Pension Offset (GPO): This rule reduces Social Security benefits to which the individual is entitled based on the work record of another individual such as spousal or survivor benefits.

- Non-Covered Pension: A pension from a job where the worker did not pay Social Security taxes.

- Primary Insurance Amount (PIA): This is the result of the Social Security benefits calculation. For retirement benefits is the same amount of your full retirement age benefit.

- WEP PIA: This is the PIA after it is calculated with the alternative WEP Social Security formula, which results in the WEP reduction.

- High-Earning Spouse (HES): For the purposes of this article, the high earner is the one who contributed the most to the Social Security system.

- Low-Earning Spouse (LES): – For the purposes of this article, the low earner is the one who contributed the least to the Social Security system.

To make all of this easier to understand, let’s break this down into two sets of easy-to-understand examples.

First, we’ll examine a scenario where one spouse is subject to these rules and look at how this affects the spousal benefit, then the same scenario except we’ll examine how this would affect a survivor benefit.

In the next set of examples we’ll examine a scenario where both spouses are subject to the WEP and GPO, and also break this down into the calculation of spousal benefits and then the calculation of survivor benefits.

And before we jump into those examples, please note that for the sake of clarity, we’re using the terms “husband” and “wife” rather than “spouse.” These are complex rules and we believe using different words to differentiate each individual and their potential Social Security benefit (rather than simply saying “spouse” for each person) will make it easier for readers to follow the narrative that illustrates these examples.

When ONE Spouse Has a Non-Covered Pension

For the first example let’s assume that the husband is not subject to the WEP or GPO, and has a monthly Social Security benefit of $2,000. The wife has a non-covered pension of $1,700 and Social Security benefits with a WEP reduced PIA of $400.

For the wife with the non-covered pension, absent any exceptions to the rules, the WEP and GPO will apply to any benefits she will receive from Social Security.

To calculate the total monthly benefit an individual would receive with a non-covered pension, you can follow these three simple steps:

Step 1: Calculate the spousal payment amount

This is only the spousal portion that will be added to the spouse’s benefit who is covered by the WEP & GPO. To find the spousal payment, you simply take 50% of the higher-earning spouse’s full retirement age benefit (PIA) and subtract the lower-earning spouse’s full retirement age benefit after it has been adjusted for the WEP.

½ Higher Earner PIA

– Lower Earner WEP PIA

= Spousal Payment

Step 2: Reduce the spousal payment portion for the GPO

With the spousal payment result from step one, you simply need to subtract an amount equal to ⅔ of the non-covered pension. For example, if the non-covered pension is $3,000, you’d subtract $2,000 from any spousal payment. This step may result in the complete elimination of the spousal payment.

Spousal Payment

-⅔ of lower-earning spouses non-covered pension

= GPO adjusted spouse payment

IMPORTANT NOTE: The GPO provision only applies if you are receiving a “government” pension as defined by the SSA. They also have a list of pensions that are NOT government pensions.

Step 3: Reduce or increase the payments based on filing ages

Now that you have the spousal payment adjusted for the GPO, you simply need to adjust both the lower earner’s benefit and the spousal payment for the age-based reductions or increases. Each of these benefit types should be reduced separately, based on the reduction factors specific to that benefit type.

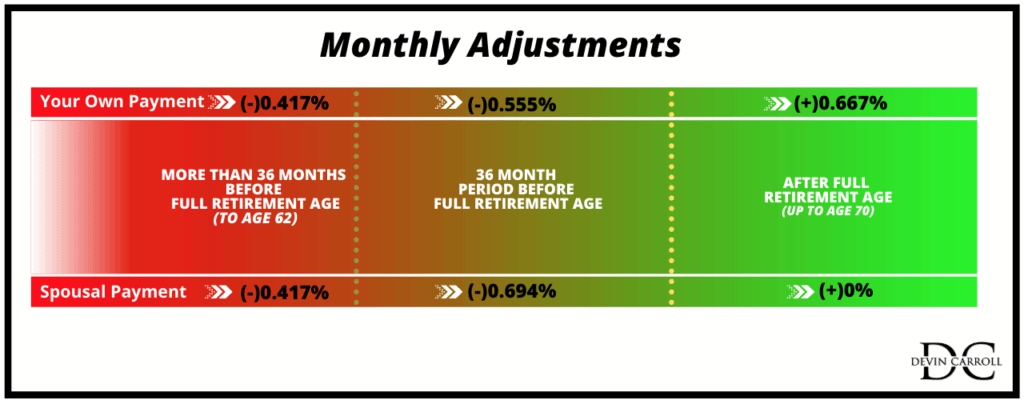

There are three separate bands that you have to know about to figure out the benefit amount in this situation:

- The band that applies if you are 37+ months from full retirement age

- The band that applies if you are 1 to 36 months from full retirement age

- The band that applies if you are already past you full retirement age

If you are more than 37 months away from FRA, the spousal payment and your own benefits are reduced the same: 5/12 of 1% (or .417%) per month.

If you are 1 to 36 months out from your full retirement age, spousal benefits are reduced by 25/36 of 1% (or .694%) percent and your own benefits are reduced by 5/9 of 1% (.555%).

After you reach full retirement age, your spousal benefits are not increased at all but your own benefits are increased by 2/3 of 1% (.667%).

With these monthly adjustment amounts, it’s now time to calculate the total monthly benefit that will be payable. To get this final amount, you need to apply separate reductions to the spousal payment and your own benefit.

Once you have each benefit reduced appropriately, you simply add them together for the total monthly benefit payable.

Spousal Payment Age Adjustment

GPO-Adjusted Spouse Payment from Step 2

– Filing Age Adjustments

= Spouse Payment Adjusted for GPO and Filing Age

Your Own Benefit Age Adjustment

Lower Earner’s WEP PIA

+/- Filing Age Adjustments

= WEP PIA Adjusted for Filing Ages

Total Benefit Payable

Spouse Payment Adjusted for GPO and Filing Age

+ WEP PIA Adjusted for Filing Ages

= Total Monthly Benefit Payable

When BOTH Spouses Are Subject to the WEP and GPO

When both spouses are subject to the WEP and GPO, the main difference in how benefits end up is in how the WEP ends when one spouse dies.

Imagine there is a husband and wife who each have their own Social Security benefit as well as a non-covered pension.

The wife spent the first 10 years of her career working at a job where she paid into Social Security. She left that job in her early 30s and started teaching at a school district where they did not pay into Social Security. At retirement, this left her with a Social Security benefit of $1,000 and, from her time as an educator, a pension benefit of $3,000.

The husband worked as a firefighter and his department did not participate in Social Security. On his days off he ran a construction business where his earnings were subject to Social Security taxes. This left him with retirement income of $3,500 from his non-covered firefighter’s pension, as well as and a Social Security benefit of $2,250 from the job in which he paid into the Social Security program and earned credits for future benefits.

To summarize, their situation looks like this:

Wife’s monthly benefits:

- $1,000 from Social Security benefits (before applying the WEP rules)

- $3,000 from a non-covered teacher’s pension

Husband’s monthly benefits:

- $2,250 from Social Security benefits (before the WEP)

- $3,500 from a non-covered firefighter’s pension

Since the husband has the higher earner’s Social Security benefit, we don’t need to consider any spousal benefits for him. He would simply receive the firefighter’s pension plus the WEP-reduced Social Security benefit.

His benefits at his full retirement age would be as follows:

$2,250 Social Security Benefit Before WEP

-$480 WEP Reduction (Based on 2020 numbers)

= $1,770 in Social Security benefits after applying the WEP rules

The wife, on the other hand, is dealing with a slightly different scenario.

Her Social Security benefit after the WEP reduction is applied would be $520. Since this is less than 50% of her husband’s Social Security benefit, she would ordinarily be entitled to a spousal payment of $365. We know this because we simply subtract the wife’s benefit from 50% of the husband’s benefit.

However, the spousal payment is subject to the GPO. That subtracts an amount equal to ⅔ of her teacher’s pension. Since the GPO reduction is greater than the potential spousal payment, no spousal payment can be paid.

That means the only benefit the wife can receive is the $520 payment from her own work:

$1,000 Social Security Benefit Before WEP

-$480 WEP Reduction (2020 numbers)

= $520 Social Security Benefit After WEP

$885 (50% of Husband’s WEP-Reduced PIA)

–$520 (100% of Wife’s WEP-Reduced PIA)

= $365 Spousal Payment

$3,000 non covered pension

X two-thirds of the non-covered pension benefit

= $2,000 GPO Offset

Because the $2,000 GPO offset is greater than the $365 spousal payment, the wife would not get the spousal payment at all.

But, if her husband dies, then her situation changes. The rules state that at death, the application of WEP ends.

This means that WEP-reduced payment the husband was receiving would not be what the potential survivor benefit was calculated from. Instead, it would be the original benefit before the WEP penalty was added on.

In this case, it would mean that the wife would simply subtract ⅔ of her pension amount from the full, unreduced PIA of the husband. His PIA, without WEP of $2,250, minus ⅔ of her $2,000 teacher’s pension, leaves a spousal payment of $250.

The wife could then add that amount to her own WEP-reduced benefit of $520, for a total monthly benefit payable of $770. Here’s how the calculations break down:

$3,000 non covered pension

X two-thirds of the non-covered pension benefit

= $2,000 GPO Offset

$2,250 PIA of Deceased Husband

-$2,000 GPO Offset

= $250 Survivor Benefit Payable to Wife

$520 Wife’s Social Security Benefit After WEP

+ $250 survivor benefit

= $770 Total Benefit Payable to Wife

I know these calculations aren’t as straightforward as we’d like for them to be, but hopefully, this guide will simplify the rules so you can finally understand how these benefits are being calculated.

Don’t leave without getting your FREE copy of my latest guide: Top 10 Questions and Answers on the Windfall Elimination Provision. You CAN simplify these rules and get every dime in benefits you deserve! Simply click here http://www.devincarroll.me/top10WEPSSI.

If you still have questions after reading this article, you could leave a comment below… but I’d suggest joining my FREE Facebook members group instead. It’s very active with really smart people who love to answer any questions you may have about Social Security. From time to time I’ll drop in to add my thoughts, too.

You should also consider joining the 275,000+ subscribers on my YouTube channel! For visual learners (as most of us are), this is where I break down the complex rules and help you figure out how to use them to your advantage.

One last thing: There is a tremendous amount of misinformation out there about the WEP and GPO. Help me clear up the confusion by sharing this article on Facebook. Thanks!

Here are some helpful resources for your continued study.

Devin’s book on the WEP and GPO https://amzn.to/2YgivmM

GPO for Dually entitled spouses

https://secure.ssa.gov/apps10/poms.nsf/lnx/0202608401

WEP for spousal payments “All benefits, including the family maximum, are determined using the WEP PIA.” Section 3(c)(a) https://secure.ssa.gov/apps10/poms.nsf/lnx/0300605360

SS Beneficiary Codes

https://www.hud.gov/sites/documents/DOC_10855.PDF

CRS Social Security: The Government Pension Offset (GPO)

https://fas.org/sgp/crs/misc/RL32453.pdf

Social Security: Beneficiaries Affected by Both the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO) https://fas.org/sgp/crs/misc/R45845.pdf

[…] How the Government Pension Offset and Windfall Elimination Provision Affects Dually Entitled Spouses […]

There were certain states that thought their pension plan would be better for their employees than using Social Security. Given the choice to opt out, they chose to not participate.

Why are WEP and GPO only in place for some states and not all ? What is the benefit for the state

that forces this adjustment ?

Great, but what are benefits generated from for a spouse who did not put into social security and did not work, or did work and still receive a portion of the workers benefit that he or she did not pay into social security for, or children for that matter. So many of us that worked and our spouses worked and are bearing the expense of so wealthy spouses, children, parents, adopted children, divorced spouses, children, etc., can live and enjoy life with less stress, while those that should receive benefits earned are having to resort to poverty because money earned… Read more »