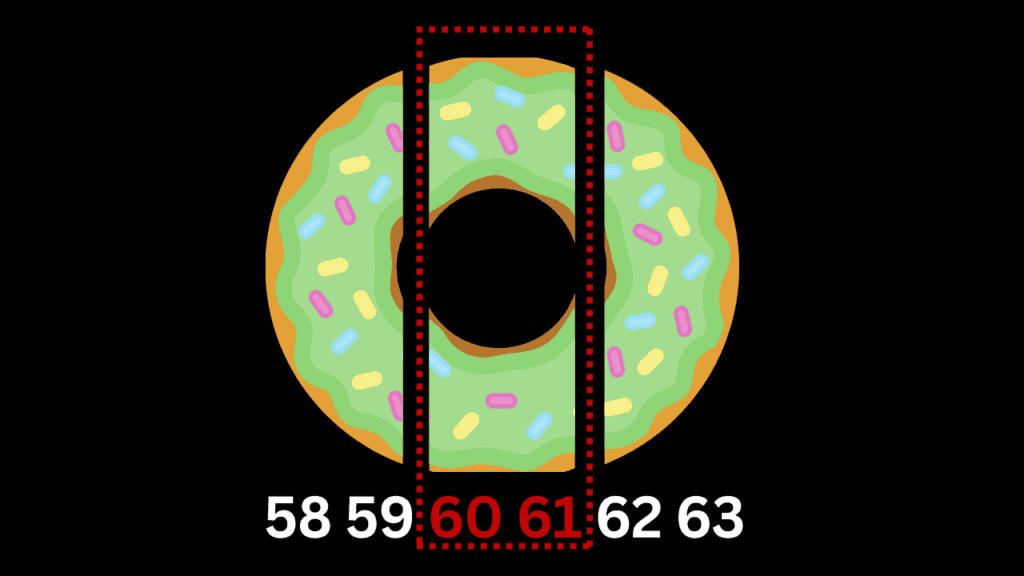

Is there a ‘donut hole’ for Social Security inflation adjustments for individuals 60 and 61 years of age?

I’ve been receiving lots of questions about benefits increases since the latest Social Security COLA was announced. The alleged donut hole for inflation adjustments to Social Security for individuals aged 60 and 61 is one of the questions frequently raised. During this period of high inflation, some members of this age cohort are upset that they may be missing out on significant benefits increases.

This thinking is based on the observation that if all wages are indexed through age 59, and the cost of living adjustments don’t start until 62, there are two years of no inflation.

It’s common to hear that Social Security will run out of money within a few years or otherwise be bankrupt by the time future generations are ready to start claiming benefits. While there may be problems for the program in the future if changes aren’t made, it’s essential to understand how Social Security is funded and how the program works in general so that you can better understand where problems might arise. Putting the many rumors about Social Security’s impending demise into context can help you better plan for your retirement and claim your benefits with less fear that the program may not be there when you’re ready.

Let’s look at how Social Security is funded, its expenses, and some of the problems it inherently faces.

Social Security’s 8.7% cost of living adjustment is old news by now. There are a lot of sites that have covered it, and most of them have covered it more than once.

Considering how hot this topic has been for a while, it’s not surprising. According to the modern method of calculating increases, this was the fourth largest cost of living increase in the history of Social Security.

This cost of living increase will be good news for the moment, but it will have a high cost and accelerate the problems with Social Security.

Several thousand people have been underpaid by Social Security, according to a government watchdog report.

We’re not talking about small dollars here either.

According to estimates, the previous underpayments have been at least $131 million, and every year an additional $9.8 million will be added.

This comes from a 2018 report from the Office of the Inspector General. This is the agency that’s in charge of overseeing several of the big government programs like Social Security. Although this isn’t a new report, there has been an update that should anger those affected.

Social Security is a complicated topic, especially when determining tax implications and how best to incorporate your benefits into your retirement plan. Many financial planners rely on data plugged into Social Security software to help their clients choose the best time to file for benefits, but depending only on a software program can mean that a lot of the details get missed and could cost you thousands in taxes during retirement.

Let’s look at how filing for Social Security benefits at age 65 versus 70 can affect your tax bill in retirement and how Social Security software is a one-size-fits-all solution to a highly individual decision.

Now that we have the official announcement of all the Social Security changes for 2023, it’s time to highlight those which will be most impactful to retirees.

These changes include:

The 2023 cost of living adjustment

The 2023 Earnings Limit

The amount needed to earn one credit

The Windfall Elimination Provision (WEP) penalty

The maximum taxable wage base

The Substantial Gainful Activity (SGA) thresholds

For clarity, let’s examine each of these individually.

The Social Security cost of living adjustment has been a hot topic in the news lately.

If you do a quick internet search for the term “Social Security” you’ll find that more than half of the articles are covering the forecasts of the upcoming benefits increase.

It’s no wonder: The upcoming cost of living adjustment will likely be the fourth largest in the history of Social Security.

As interest in this topic has grown, individuals are learning more about how these increases are calculated. And not everyone is happy about it.

Many of the comments I’ve been seeing claim that the numbers are rigged and that the increase in the cost of living won’t even be close to inflation because the numbers will be adjusted explicitly for the purpose of lowering the annual increase.

Some of this skepticism comes from the time period used in how the cost of living adjustment is calculated. While we have the inflation numbers that come out every month, it’s ONLY the months of July, August, and September that are counted for the annual increase to Social Security.

According to some, inflation goes down during those three months, then goes back up again. They suggest that if we used the entire 12-month period of data, we would get a more accurate cost of living adjustment and a larger increase.

So today, I want to tackle this head-on and look at the historical data to answer this question once and for all.

If you’re like most people, you’ll need Social Security retirement benefits to help you make ends meet in your golden years. That’s why it’s so important to understand the rules for these benefits.

Unfortunately, if you don’t know how the retirement income program works, you actually could find yourself inadvertently losing some of the money you were expecting.

To make sure this doesn’t happen to you, there are four situations you need to know about that could lead to a temporary or permanent reduction in your retirement income from the Social Security Administration.

Many Americans look forward to the time when they’ll be able to claim Social Security benefits. After all, receiving a guaranteed income for life from the government may seem like an ideal way to fund an enjoyable retirement.

The reality, however, is that Social Security benefits may not be as generous as you think. And you could end up in dire straits if you over-rely on them as a retirement income source.

To make sure you don’t end up suffering financial insecurity in your later years due to a misunderstanding about the role that Social Security will play in funding your future, you need to know these four harsh truths about the benefits you’ll get in your golden years.

Social Security is one of the most important government programs ever created as it has single-handedly kept millions of seniors out of poverty. Unfortunately, it’s also a complicated program that many people don’t know the intricacies of.

Not only are many Americans in the dark about some major Social Security realities, but millions have also bought into falsehoods about this benefits program that could end up costing them.

You don’t want to make decisions based on inaccurate assumptions, only to learn the truth too late, so read on to make sure you haven’t fallen for any of the following four common myths and misconceptions

Social Security is one of the most important government programs ever created as it has single-handedly kept millions of seniors out of poverty. Unfortunately, it’s also a complicated program that many people don’t know the intricacies of.

Social Security is one of the most important government programs ever created as it has single-handedly kept millions of seniors out of poverty. Unfortunately, it’s also a complicated program that many people don’t know the intricacies of.